Since mid-March, the M1 measure of the money stock has grown $900 billion—an increase of more than 20 percent over just two-and-a-half months. If it kept this pace, M1 would double in a year. Accompanying this, the Federal Reserve has injected massive amounts of liquidity into our economy by purchasing more than $2-1/2 trillion of assets over this same period. Haven’t we heard over and over that inflation is caused by “too much money chasing too few goods”? In view of this, has inflation begun to roar yet?

Before turning to price data, it is important to note that inflation results when the supply of money grows faster than demand—it is that which constitutes “too much money.” But when they both increase by the same amount, forces are not unleashed that lead to more inflation. Indeed, this is what has happened over recent months. The demand for cash rose sharply as the country was going into lockdown. With so much uncertainty about the prospects for earnings in the weeks and months ahead, both businesses and households sought to get through this shock by storing up cash. They cut back on spending, sold assets, and borrowed against lines of credit to build up precautionary balances, and the Fed accommodated all of this greater demand. And the way the Fed conducts business, it likely will accommodate an unwinding of this buildup once it gets underway. And an inflationary surge will be avoided.

A more helpful way to look at the outlook for inflation is to realize that both expectations of inflation and the aggregate demand-aggregate supply balance determine the rate at which prices change. When inflation expectations increase, businesses will post larger price increases and workers will seek larger increases in wages to compensate for the greater expected inflation. As a result, actual inflation will also increase. Similarly, when aggregate demand expands in relation to aggregate supply, upward pressure on inflation develops. These relationships imply that when demand matches supply, actual inflation will equal expected inflation. And when demand falls short of supply, actual inflation will run below expected inflation.

We know that the COVID-19 pandemic has resulted in reductions in both aggregate demand and aggregate supply. As noted in a previous posting (What Are We Learning About the Economic Decline, May 15), demand has contracted more than supply. The surge in the personal saving rate from its typical level of 8 percent of disposable personal income in February to 33 percent in April underscores the extent to which consumers had cut back on all but necessary spending. Evidence on business outlays points to a sizable cutback in that sector, too.

Just-released consumer and producer prices through May confirm that inflationary pressure has not emerged. The headline CPI declined 0.1 percent in May, bringing the three-month cumulative decline to 1.3 percent. Even the core CPI, which excludes volatile food and energy prices, declined 0.1 percent in May and was down 0.6 percent over the three months. The twelve-month change in the headline CPI was only a plus 0.1 percent and the core CPI 1.2 percent, both well below the Fed’s target of 2 percent.

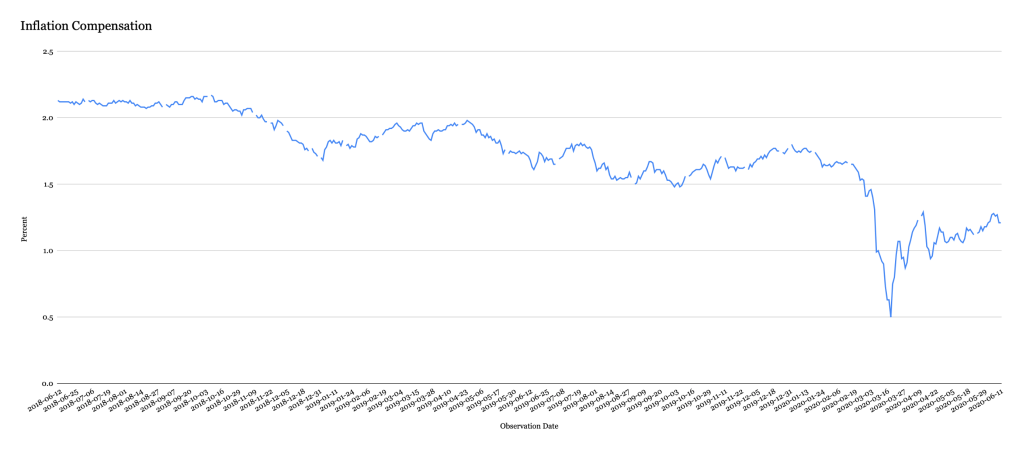

Recent evidence on expectations of inflation suggests that the weak inflation readings of late are not primarily the result of the inflation expectations component. We do not have real-time data on inflation expectations and must make inferences from other sources. One such source, inflation compensation, is shown below.

Inflation compensation—consisting of expected inflation over the next ten years plus an inflation risk premium—is derived from the market for Treasury securities. The expected inflation component is the larger of the two and the inflation risk component tends to be more stable, implying that movements in inflation compensation generally reflect movements in expected inflation. This measure dropped early in the pandemic but has been more stable since then. This tells us that lower inflation expectations may account for some of the slowdown in inflation, but that weak demand has been more responsible—especially in the past two months.

Looking at the components of the price index, there are major cross-currents that should not be surprising. Registering declines of 1 percent or more last month were airline fares (-4.9 percent), motor vehicle insurance premiums (-8.9 percent), hotels (-1.8 percent), and apparel (-2.3 percent). These have come on the heels of declines in previous months, accumulating to double-digit declines over the past three months (except for a cumulative drop of 9 percent in apparel prices). Most notable among the increases was food at home which was up 1 percent in May—paced by beef, up nearly 11 percent—and 4 percent over the past three months. Health insurance premiums rose another 1.1 percent in May, bringing the twelve-month increase to nearly 20 percent. Interestingly, the 3.5 percent increase in health insurance over the past three months represents a moderation from the pace of the previous nine months. Perhaps the weak economy is even showing through to this component.

At the end of the day, it is the change in the average price of the goods and services that we buy that represents inflation, and that is what the CPI attempts to capture. The discussion above suggests that there continued to be deficient demand through last month. The challenge facing the Federal Reserve at this point is stimulating demand sufficiently to get inflation to move higher, at least to match inflation expectations. Despite all the liquidity in the economy, there is not much of a threat of an outbreak in inflation in the months ahead. Beyond that point, keeping us from unwanted inflation will depend on the Fed knowing when to begin removing stimulus. In its view, this is more than two years away. The Fed has the capability to keep inflation under control and has a reputation to preserve.

The role of the financial markets in disciplining a market economy is discussed in chapter 2 of Capitalism Versus Socialism: What Does the Bible Have to Say?