The recent news on the COVID-19 crisis has been mostly negative, suggesting that the recovery may be experiencing a major setback (the glass is mostly empty). However, a variety of reports on the economy recently have pointed to unexpected vigor (it’s mostly full). Granted, many of these reports are from June, before the recent COVID wave got legs. Yet the June data are telling us that there is more resiliency in the economy than had been presumed. And prospects going forward, especially once we put the current spread behind us, are highly favorable.

Turning to the June data, retail sales, which surged 18 percent in May, rose another 7.5 percent in June (at a monthly, not annual, rate), placing the level 1 percent above a year earlier. This is pretty remarkable given what we have been through since February! The gains in June were fairly broad-based, including apparel stores (up 105 percent), furniture stores (up 33 percent), electronics and appliance stores (up 37 percent), sporting goods stores (up 27 percent—that bike or bike accessory you purchased last month), and restaurants and drinking places (up 20 percent). Notable among the decliners were grocery stores and nonstore retailers (Amazon), both of which posted big increases while we were locked down. These patterns are indicating that we were making progress in getting back to normal last month.

The increase in industrial production in June also was solid. Production of consumer goods rose 9 percent and business equipment nearly 12 percent. These were larger gains than in May, as the resumption of getting back to work picked up steam. Of note, output of processed foods—which had been seriously disrupted by the pandemic—quickened in June. The ramping up of final goods production is alleviating strains on retail inventories in some sectors.

Consumer prices in June also point to some return to normalcy. The headline CPI rose 0.6 percent, its first monthly advance since February, paced by gasoline and food prices. Excluding food and energy, consumer prices rose 0.2 percent, also the first uptick since February. Food prices were again boosted by meats, suggesting that bottlenecks in food processing are being removed slowly. Elsewhere, there was a bottoming out or upturn in prices of items that had fallen sharply during the lockdown—airfares, hotels, apparel, and car insurance premiums. Nonetheless, prices in these categories were still well below levels before the onset of the pandemic. Perhaps of no surprise, health insurance premiums continued their upward climb, barely dented by the recession. Overall, the data are telling us that aggregate demand and aggregate supply have moved into better balance in the past couple months.

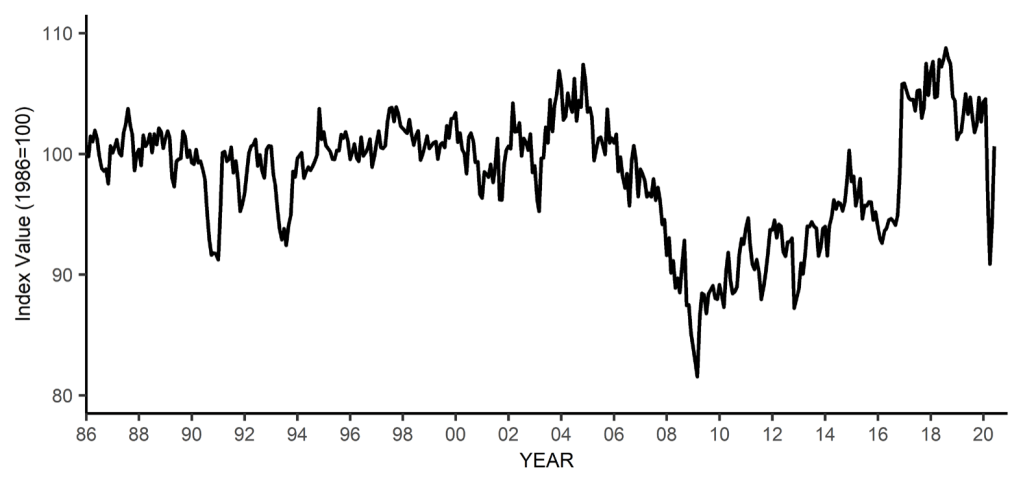

Turning to other sources, the National Federation of Independent Business (NFIB) Optimism Index rebounded further in June, as shown in the chart below. By June, it had recovered nearly three-fourths of its decline since February. Recent monthly increases in this index have surpassed expectations by analysts. Also, several Federal Reserve Banks conduct frequent surveys of the economic outlook in their Districts. Nearly all of these have been very upbeat of late, also exceeding expectations of analysts.

Meanwhile, initial claims for unemployment insurance remain elevated, but continue to drift lower. At the same time, the total number of persons receiving unemployment insurance has edged down, indicating that a huge number of people are returning to their jobs or getting hired into new jobs. The drop in those receiving unemployment benefits is likely to be substantial after the end of this month when augmented benefits ($600 per week) are scheduled to end. The bulk of those currently receiving benefits by not working (five out of six) will be able to receive more money by returning to their jobs.

Putting all of this together, the recent evidence has continued to show that both consumers and businesses are eager to return to something resembling normal. This continues to be evident by a snapback in key economic indicators that steadily surprises the experts. The recent resumption of the spread of COVID-19 may lead to a brief pause in the recovery, but American determination and ingenuity will ensure that the trajectory of the economy is firmly upward—that the glass is mostly full.

Check out Chapter 2 of my new book—Capitalism Versus Socialism: What Does the Bible Have to Say?—for more on the inherent resiliency of market-based economies.