Many have puzzled over the rebound in the stock market during this period of COVID-19 struggles. The blue-chip S&P 500 stock price index is only 6 percent below its mid-February peak, having recovered more than 80 percent of its COVID-related losses. Moreover, the Nasdaq index—a barometer of the tech sector—has soared to new highs. Has someone forgotten to tell investors that we are still dealing with a pandemic or do they know something that has escaped the rest of us?

The stock market is forward-looking. Prospective earnings play a big role. News bearing on prospective earnings—including news on the economy—can have a big impact on stock prices. Additionally, investor appetites for risk affect share prices (see my June 5 post, Has the Market Gotten Ahead of Itself?). When investors become very uncertain and nervous about the outlook, they will insist on higher returns on stocks as compensation for the greater risk. That is achieved by a drop in share prices.

Finally, returns on competing investments affect stock prices. If returns on competing investments increase, share prices will need to fall to attract investors, or else they will shift into those other investments. Conversely, if returns on competing investments fall, investors view stocks to be more attractive and will bid up their prices. The current ultra-low interest rates are an important factor buoying share prices.

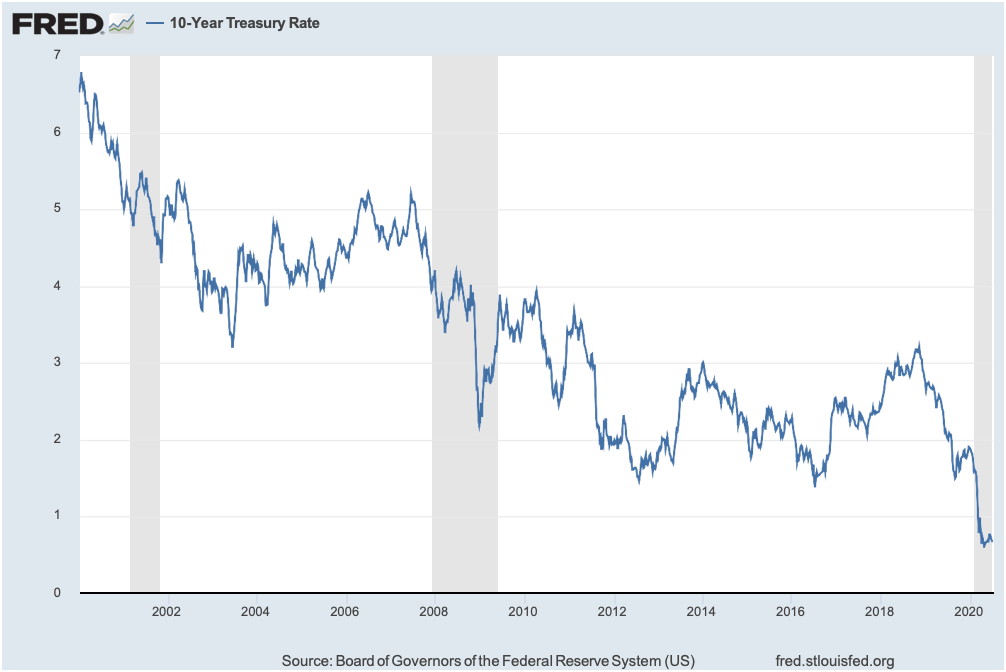

The chart below shows the yield on the benchmark ten-year Treasury note over the past two decades. Even before the onset of the pandemic, yields had dropped to very low levels by historical standards—under 2 percent. But they have plunged lower in recent months, to below 1 percent.

Interest rates have fallen over recent decades because inflation has fallen and expectations are that inflation will remain low going forward (meaning that investors do not need as much compensation for the erosion of purchasing power that accompanies inflation).

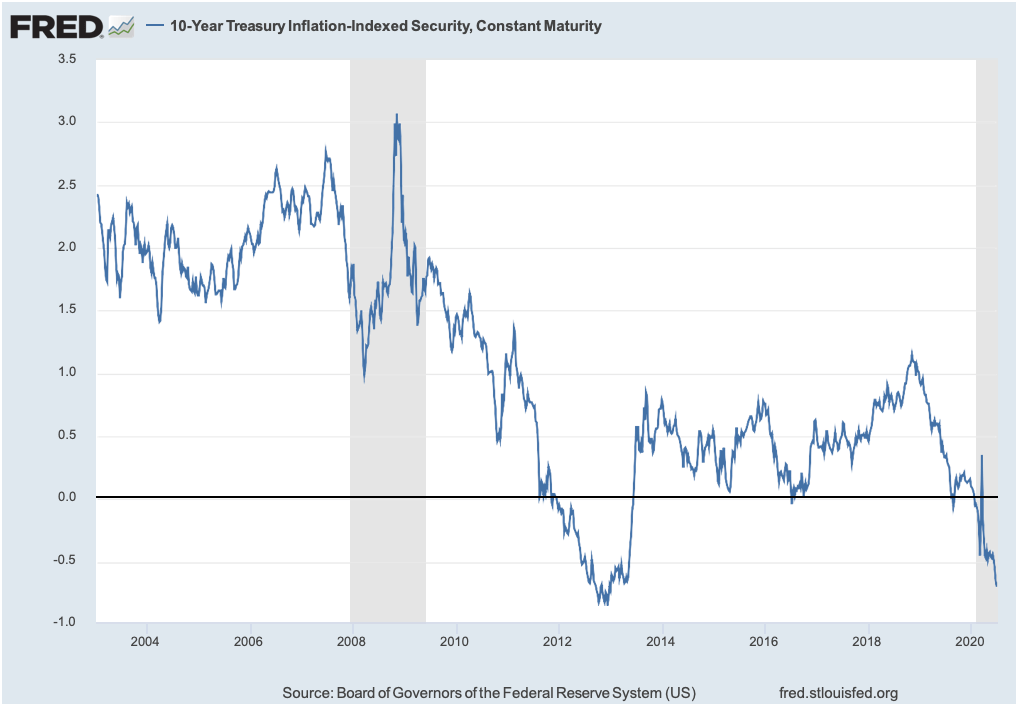

Beyond low inflation, a greater supply of savings and reduced demand for funds by businesses have caused real interest rates (interest rates after inflation) to drop to extraordinary levels. The next chart plots the real interest rate on a special type of ten-year Treasury security (a Treasury Inflation Protected Security or TIPS). For this security, investors are promised a given interest rate (a given real interest rate) and are given additional compensation based on the actual change in the Consumer Price Index. Before the pandemic, the real interest rate had been flirting with zero.

However, more recently it has moved into negative territory. This means that investors have been willing to accept inflation compensation that falls short of actual inflation—willing to lose purchasing power!

As the economy gets back to a firmer footing, some of the recent declines in interest rates will be reversed. However, interest rates are going to stay low for quite some time. This is because the Federal Reserve, in response to the COVID-19 shock, has committed to keeping the short-term interest rate that it controls—the federal funds rate—low (near zero) for some time to come. This commitment, coupled with its commitment to ongoing large purchases of Treasury securities in the open market, will keep Treasury yields low, and, with them, a wide range of other interest rates (see my May 5 post, Are We Drowning in Fed Liquidity?).

In the coming weeks, wild daily swings in stock prices will continue to result from news on the COVID-19 front. These will be augmented by corporate earnings reports for the just-concluded second quarter. However, share prices will continue to be supported by upward pressure from the new era of ultra-low interest rates. Investors have heeded the message.

Check out Chapter 2 of my new book—Capitalism Versus Socialism: What Does the Bible Have to Say?—for a discussion of the role of financial markets in a market-based economy.

2 thoughts on “Buoying the Market: An Era of Ultra-Low Interest Rates”