In light of the hot housing market, there is mounting concern about another housing bubble. Are things getting out of hand in the housing market? Is another crash coming soon?

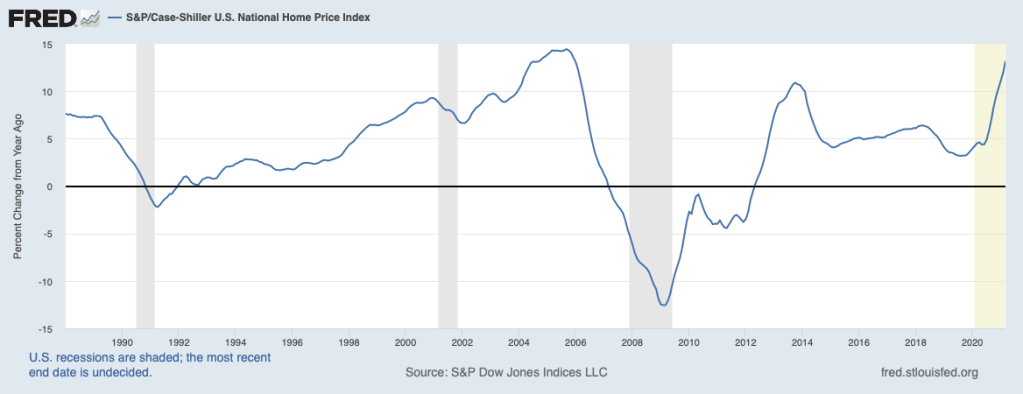

The first chart below illustrates that the twelve-month increase in the price of existing homes was 13 percent in March (the measure shown is not distorted by shifts in the mix of sales between lower-end and upper-end homes). This increase is reaching the territory of a decade-and-a-half ago. The bursting of the bubble that characterized that period triggered the worst financial crisis and economic downturn since the 1930s.

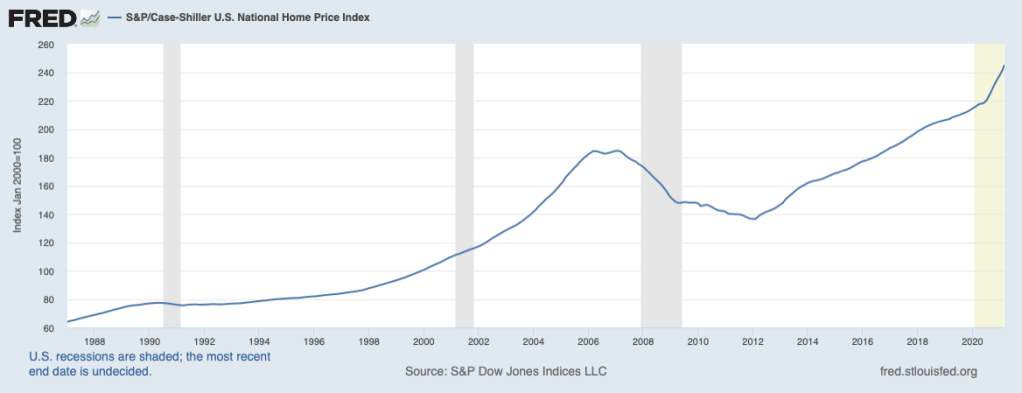

Adding to concern about home prices is the average price of an existing home which is now a third above the peak in 2006, shown in the following chart.

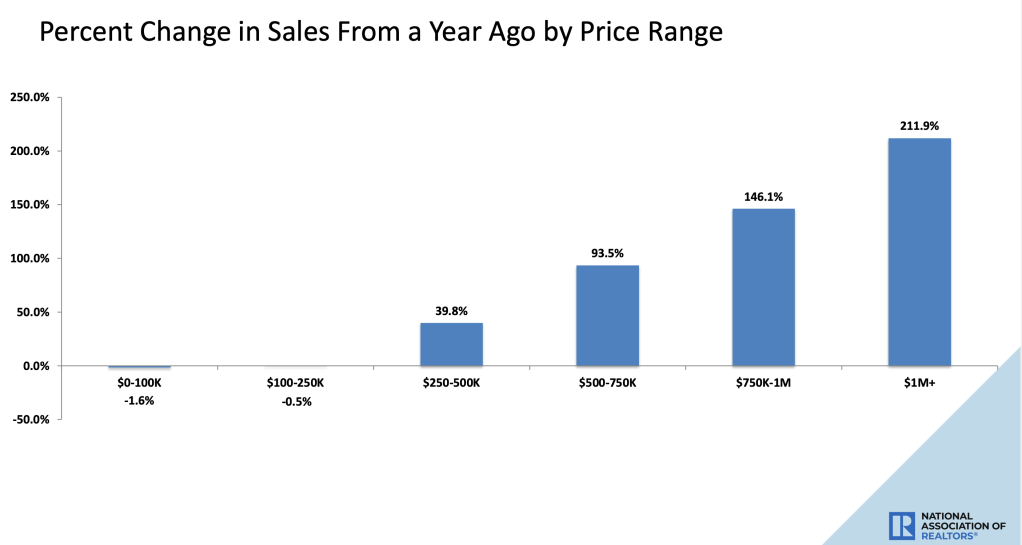

Activity in the housing market continues to be concentrated in the $500 thousand and above price range, shown in the next chart. Over the twelve-month period to April, sales in the $500 to $750 thousand range nearly doubled, sales in the $750 thousand to 1 million range were up nearly 150 percent, and sales in the above $1 million range were up more than 200 percent.

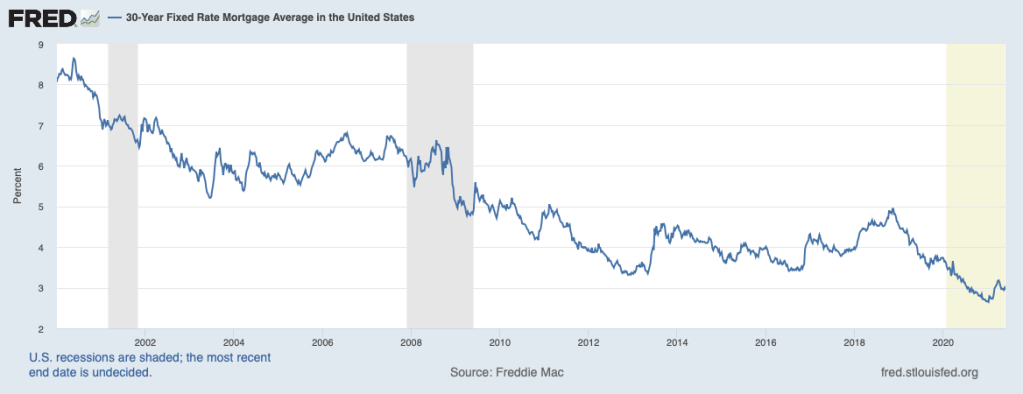

What is driving activity in the housing sector, especially outsized increases in prices? Lower mortgage rates, shown in the next chart, have been playing a major role. Rates on a thirty-year fixed-rate mortgage were roughly 3.75 percent at the onset of the pandemic in 2020 (down about a percentage point from a year before) and have fallen to 2.95 percent more recently. This decline can account for the bulk (roughly 10 percentage points) of the 13 percent increase in prices over the past year. Also factoring into recent home price gains is the growing likelihood of higher marginal tax rates on income, which add to the value of the mortgage interest deduction.

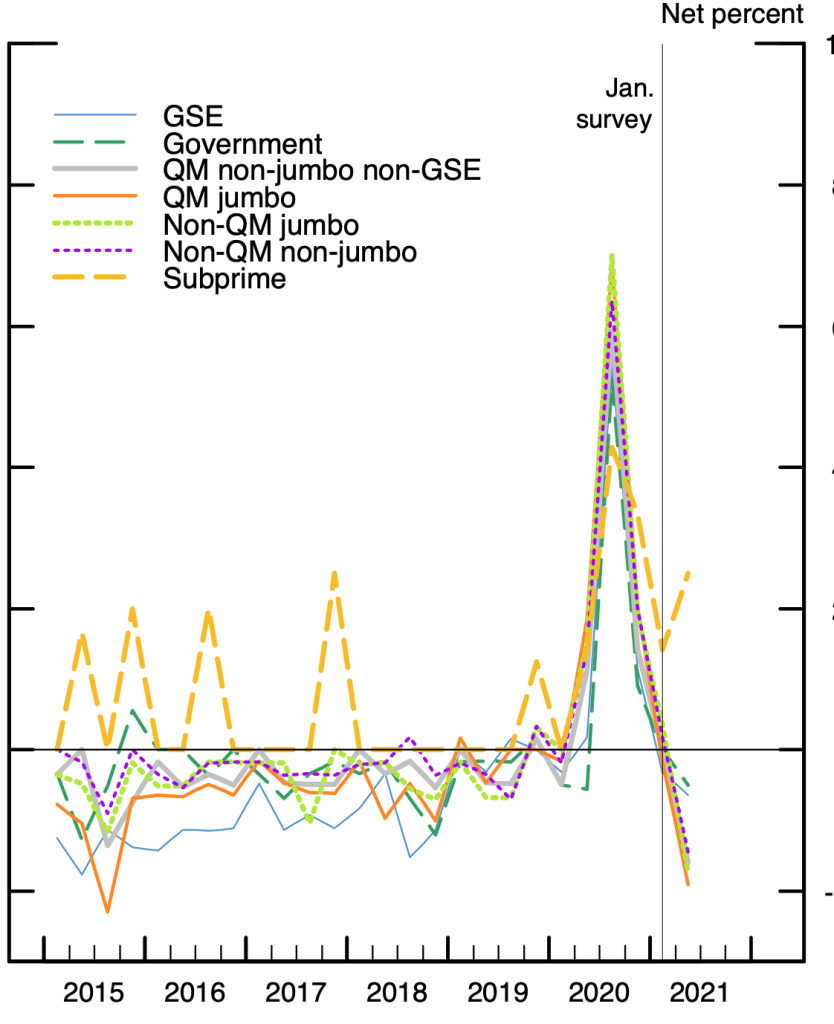

Furthermore, lenders have been easing underwriting standards for mortgages, including for nontraditional loans. This easing can be seen in the next chart showing the percent of commercial banks tightening underwriting standards for borrowers seeking traditional mortgages (GSE and Government) and for borrowers seeking nontraditional (such as jumbo) and subprime mortgages (QM in the chart refers to qualifying mortgages which have certain properties that reduce default risk).

During the financial crisis of 2008 and 2009, lenders sharply tightened underwriting standards for all types of mortgages, and those standards remained tight until early this year. During this period, mortgage credit was only available to homebuyers with strong credit ratings and could make relatively large down payments. But lenders have begun to ease standards for all borrowers except those seeking subprime loans. Looking ahead, the easing of standards on both qualifying and nonqualifying jumbo mortgages should be giving a further boost to the upper end of the housing market.

Net Percent of Domestic Commercial Banks Tightening Home Mortgage Standards

Another contributor to the increase in home prices has been the jump in the cost of building materials, notably lumber prices. Some of these increases have been the result of pandemic-caused supply chain disruptions. While materials prices directly affect the price of new homes, they indirectly affect the prices of existing homes as higher new home prices lead homebuyers to bid up the price of existing homes.

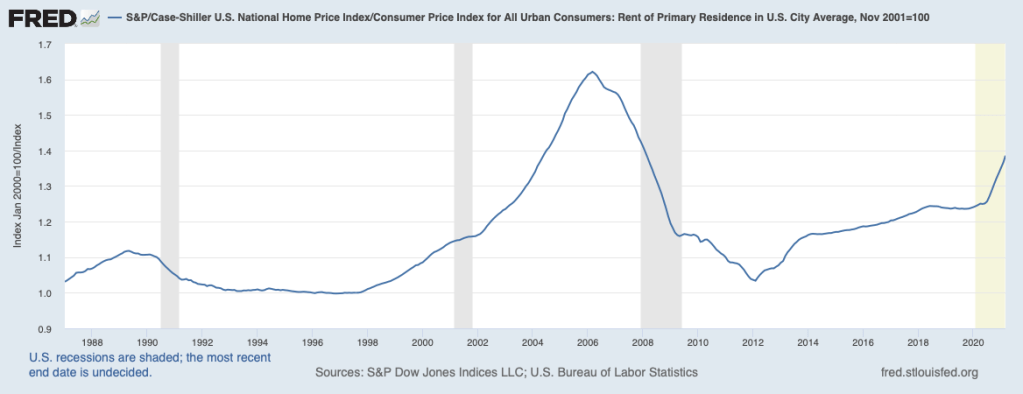

In judging whether the housing market has entered into a new bubble phase, a useful metric is home prices in relation to rents. The next chart presents the ratio of home prices to rents (the level of this ratio has no intrinsic meaning, but is useful for determining whether prices are out of line with historical norms). This ratio is somewhat high by historical standards and has risen a good bit since the onset of the pandemic. Very low mortgage interest rates can explain both the relatively high ratio and much of the recent increase. Despite the recent increase, the ratio is still well below the levels that characterized the bubble period of the early 2000s.

To sum up, frenzied activity in the housing market has been accompanied by a return to double-digit increases in home prices. Playing a key role in this situation have been extraordinarily low interest rates, which have also contributed to a lofty stock market and various other indications of investors scrambling for higher returns. As lenders continue to ease underwriting standards for nontraditional loans, there is likely to be more upward pressure on home prices. At this point, it does not appear that a worrisome bubble has developed, but the situation deserves close attention. A turnaround in interest rates—coming from a surge in inflation or even more debt-financed fiscal stimulus—could bring a quick end to rising home prices.

The functioning of markets and the role of interest rates are discussed in Chapter 2 of my book, Capitalism Versus Socialism: What Does the Bible Have to Say?