The recent news on the economy confirms that the labor market continues to tighten, even though 7-1/2 million fewer people were employed in May than at the onset of the pandemic. Strains in the labor market are holding down gains in employment and growth in output and placing upward pressure on inflation. Indeed, hiring problems have been evident in the shortfall from expectations of employment growth in April and May and could be shaving 2 percentage points off growth in real GDP in the second quarter. The question is: Will these strains be receding sufficiently to avoid inflation ratcheting upward?

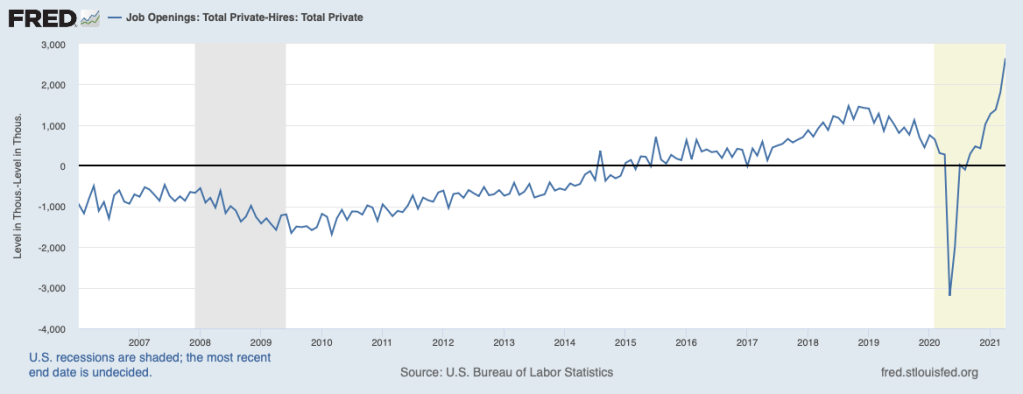

A scramble for labor can be seen by the excess of job openings over new hires, shown below. This gap moved further into uncharted territory through April (most recent data).

What is responsible for this extraordinary situation? There has been a pronounced reluctance on the part of many workers to reenter the labor force.

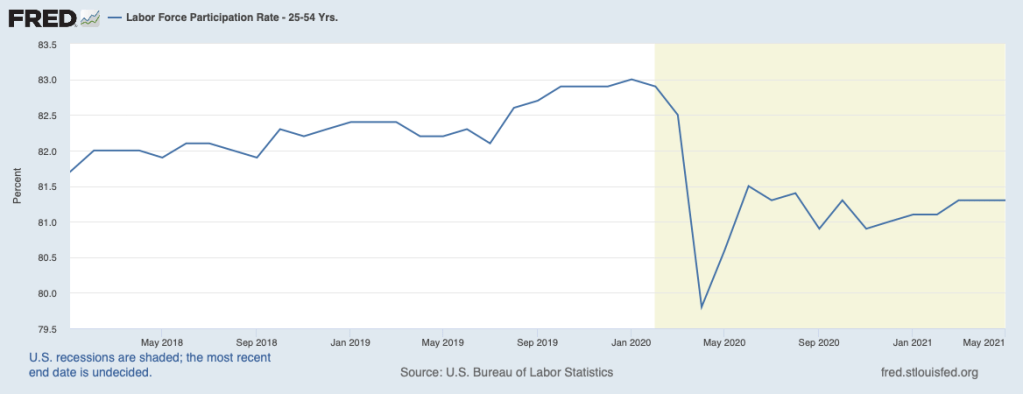

The next chart shows that the labor force participation rate on the part of prime-age adults (those in the 25-to-54-year-old age group who classify themselves to be in the labor force relative to all adults in that age group) remains well below the peak in early 2020 and has shown little movement since last summer.

Commonly mentioned reasons for this reluctance are fear of being exposed to COVID, the need to stay at home to care for children who have not returned to the classroom, and the attractiveness of unemployment insurance benefits, especially with the $300 per week federal supplement. Pointing to a lessening of the first two factors is substantial progress in reducing the incidence of COVID and reopening the economy and the return of many students to the classroom. This leaves the supplement. We will be seeing the impact of the supplement more clearly in the coming months as half of the states have dropped it in an effort to incentivize workers to return to the workforce and fill vacant positions (the federal supplement program is scheduled to expire at the end of September).

Persons for whom the supplement is most attractive are those at the lower end of the pay scale. They tend to be employed by smaller businesses. The trade association for smaller businesses, the National Federation of Independent Businesses (NFIB), reported that in its survey for May a record 48 percent of employers reported difficulty in filling jobs.

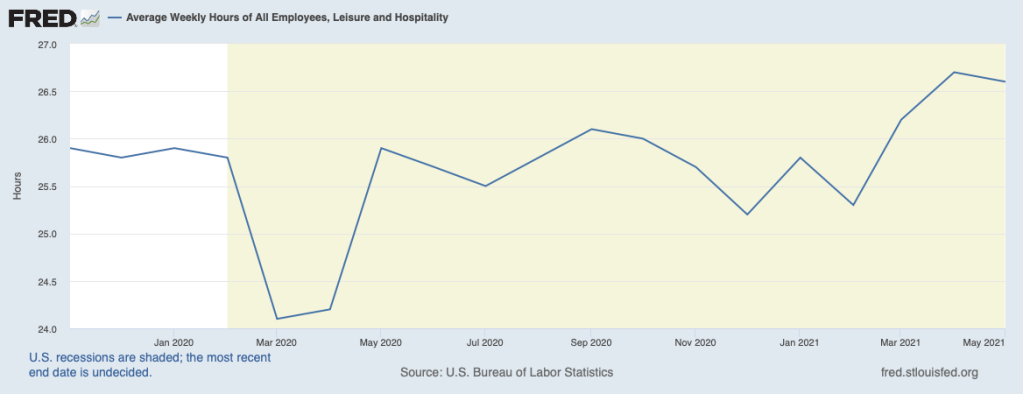

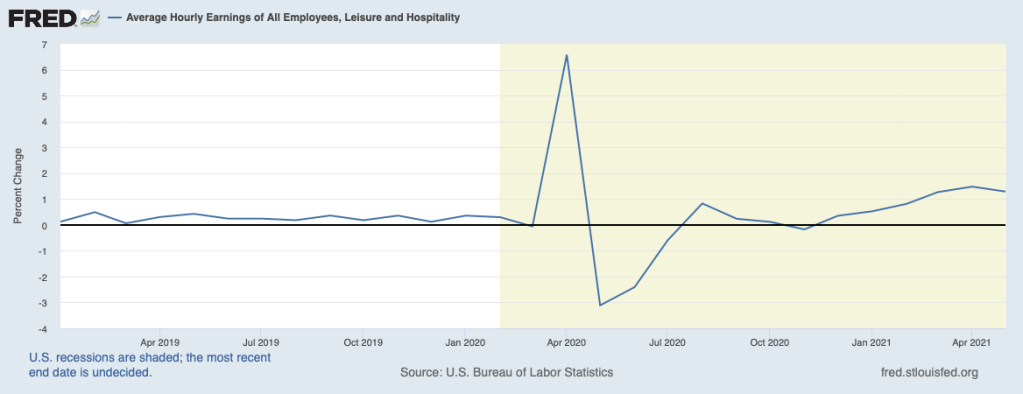

Most vocal among small businesses has been the employers in the leisure and hospitality sector. This includes restaurant and bar owners. Employers in the hospitality sector have responded to excess demand and difficulty in attracting new workers by boosting the hours of current workers, shown below, to above pre-pandemic levels. These employers have also been raising compensation. The next chart shows that average hourly earnings in the leisure and hospitality sector have been rising at rates well in excess of the pre-COVID pace since the beginning of the year as this sector has been trying to reopen.

In the chart below, the spike in this measure of earnings early in the pandemic owes to the change in the mix of higher and lower wage employees as lower-wage workers were the first to be let go. The readings in recent months no doubt understate actual increases as lower-wage employees have been returning to work.

Small business owners more generally report boosting compensation to get workers back on the job. One-third of NFIB respondents reported raising compensation (including offering bonuses) in May to attract and retain employees. Furthermore, a net 40 percent reported raising their prices in response, the largest number in forty years.

In May, for the second month in a row, CPI inflation exceeded expectations by a sizable margin (the core CPI—that excludes volatile food and energy components—rose 0.7 percent compared with expectations of 0.4 percent). Price increases were widespread across categories and notably large in certain components. In some cases, the increase represents a delayed recovery in some of the hardest-hit sectors, such as airfares (up 7 percent on the month and 24 percent on the year), hotels (up 10 percent on the year), and food away from home (up another 0.6 percent in May). Much of these increases reflect rising labor costs being passed through to consumers. In other cases, outsized price increases are due to supply chain disruptions, new cars (up 1.6 percent in May), and TVs (up 0.9 percent in May and 4.5 percent over the year for a category that typically declines).

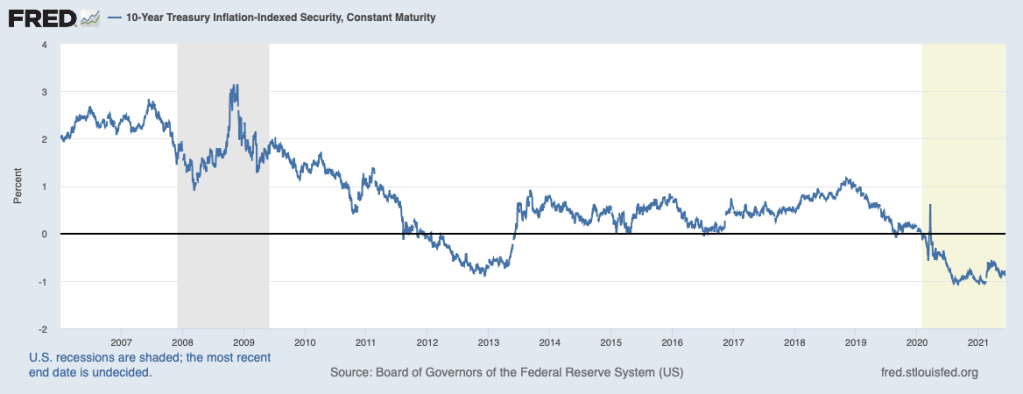

More price increases are coming in the months ahead. Whether the increases will prove to be transitory or more lasting will be determined largely by their impact on inflation expectations of businesses, households, and financial market participants. Until recently, inflation expectations have been relatively stable. The presence of fairly stable (well-anchored) inflation expectations around the Fed’s 2 percent inflation target has allowed the Fed to direct the tools of monetary policy to its maximum employment mandate. But if inflation expectations move higher, those tools will need to be redirected to the other mandate—stable prices—or the Fed’s credibility and its effectiveness will be under threat. To illustrate, at the onset of the COVID shock, the Fed was able to shift to an extremely accommodative monetary policy to counter weakness in the economy and a wholesale loss of jobs. This policy shift caused real interest rates—borrowing costs after removing expected inflation—to move into and stay in negative territory, as shown below.

Such attractive borrowing terms have fueled a surge in demand for housing and other big-ticket items purchased on credit (see May 31, 2021 post The Economy: Housing Bubble Redux?).

However, this highly accommodative monetary policy has also added to pressures on prices. If the greater attention given to inflation recently is causing the public to raise its expectations of inflation beyond the 2 percent area, the Fed will be faced with a dilemma—either remove accommodation to restrain inflation with adverse implications for employment and output or risk inflation ratcheting still higher.

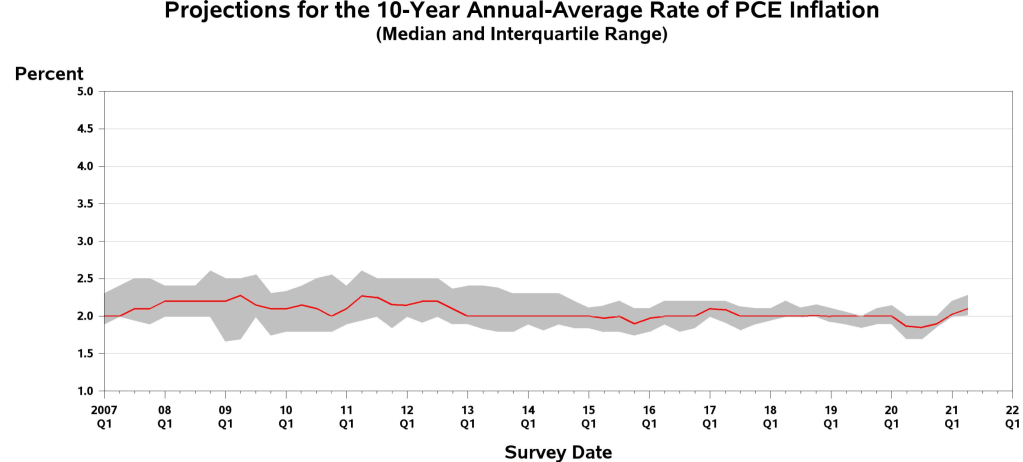

The recent evidence on inflation expectations raises some concerns. The chart below plots professional forecasters’ expectations of inflation over the next ten years. In the most recent survey, released in mid-May, this measure continued to move upward and climbed above 2 percent.

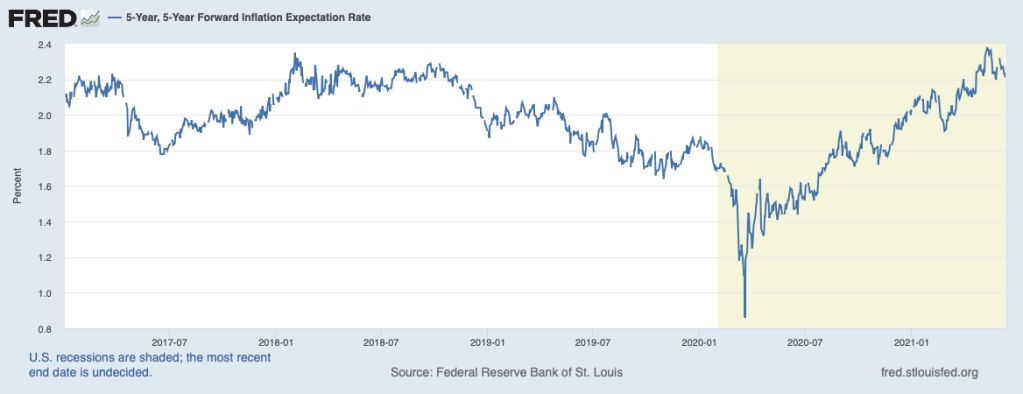

Similarly, longer-term expectations of inflation taken from the market for Treasury securities, shown next, have moved up a good bit over recent months.

Recent upward movements in both measures of inflation expectations are not enough to cause alarm right now, but do suggest that with more public attention becoming focused on inflation, additional inflation surprises in coming months will put the Fed in the hot seat.

In sum, strains in the labor market are adding to inflationary pressures. A portion of the bigger inflation numbers of late reflect temporary factors that should be abating in the coming months. However, more lasting inflation problems coming from difficulties in getting workers back on the job and rising expectations of inflation could threaten an orderly economic recovery. The sooner the unemployment insurance supplement expires, the better are the odds that we will avoid a more serious inflation problem. For more on the impact of generous subsidies on the willingness to work, see Chapter 5 of my book, Capitalism Versus Socialism: What Does the Bible Have to Say?