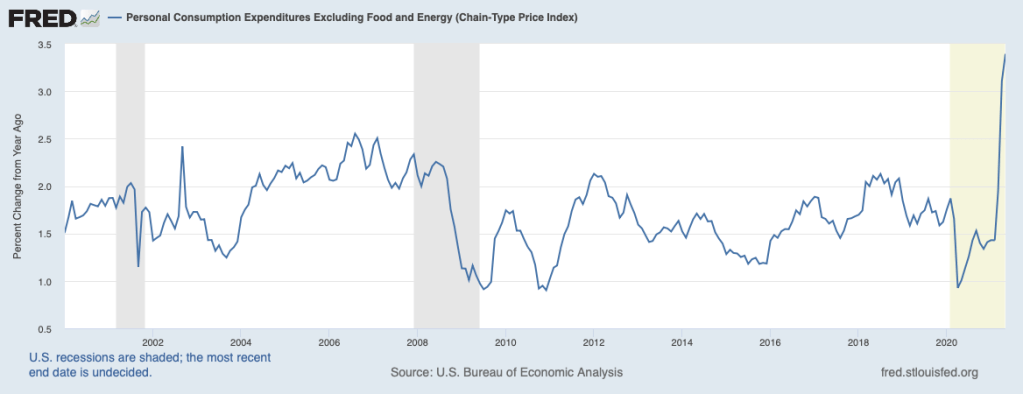

The pickup in inflation in recent months has spurred worries about whether we are entering an uncomfortable new era beset by large price increases. The chart below illustrates that core inflation (which excludes volatile food and energy prices) has spiked recently. For nearly a decade before the pandemic, core inflation ran at a 1-1/2 to 2 percent on a twelve-month basis, but jumped to 3.4 percent in May.

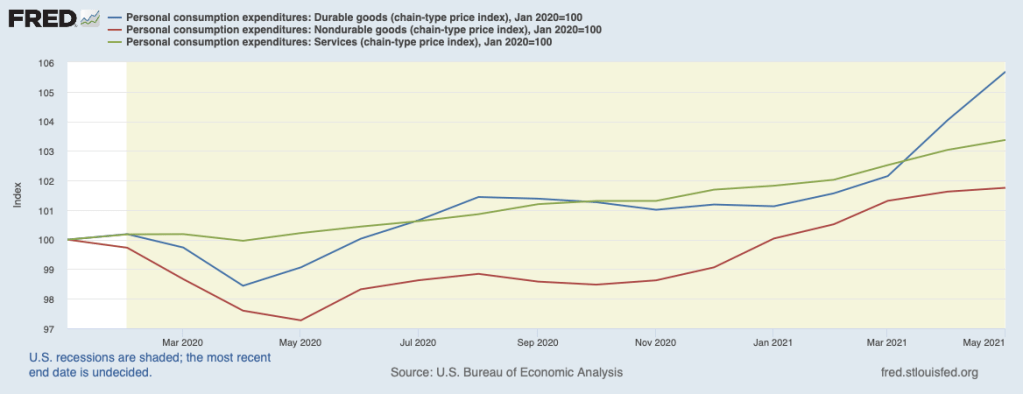

The following chart examines the levels of prices of the principal components of consumer spending—durable goods, nondurable goods, and services—indexed to be 100 in January 2020. Prices of all three categories are now above their pre-Covid levels, even though durable goods prices (blue line) and service prices (red line) fell immediately after the onset of COVID. Since early this year, the prices of both durable goods and services have registered sizable increases, largely reflecting supply restraints interacting with strengthening demand. Is this only a blip on the radar screen, or does it portend that disruptive inflation is becoming the new normal?

Various factors can contribute to inflation in the shorter term, but sustained inflation ultimately can be traced to monetary policy. The Federal Reserve, which sets monetary policy, has noted that much of the recent surge in prices is transitory—that is, short-lived. They point to the recovery of prices in those areas of the service sector that were hit hardest by COVID. They also point to supply chain disruptions that are curtailing supplies temporarily (especially the chip shortage disrupting production of motor vehicles and appliances) in the face of very strong demand.

It should be noted that the Fed has established a target of 2 percent inflation, but currently is seeking inflation above 2 percent for some unspecified length of time. In a policy announced last August—so-called flexible average inflation targeting—the Fed stated that it is attempting to make up for the shortfall from 2 percent inflation in recent years to achieve 2 percent average inflation over time. This is based on the recognition that 2 percent inflation will not be achievable on a sustained basis unless inflation expectations are anchored around 2 percent and there had been growing evidence that inflation expectations had moved down below the 2 percent area in response to persistent below-2 percent readings on inflation.

The issue now is whether the upturn in inflation recently will prove to be short-lived and sufficient to bring average inflation up to 2 percent or whether we are entering a new inflationary era, perhaps replaying the debacle of the 1970s. It should be noted that the Fed has been behind the curve in its forecast of the strength of the economy and inflation for some time. The Fed’s lag can be seen in the table below, containing forecasts for the year 2021 (the FOMC is the Fed’s monetary policy body). The forecast for output growth has been raised from 4 percent last September to 7 percent this June. This implies that growth will slow from an 8-1/4 percent rate over the first half of this year to a rate of 5-1/2 over the second half (a plausible outcome). The forecast for core inflation has moved up from 1.7 percent last September to 3.0 percent in June.

FOMC Forecast for Output Growth and Inflation for 2021

| Forecast Date | Growth in real GDP (percent) | Core inflation |

| Sep. 2020 | 4.0 | 1.7 |

| Dec. 2020 | 4.2 | 1.8 |

| Mar. 2021 | 6.5 | 2.2 |

| Jun. 2021 | 7.0 | 3.0 |

Based on price data through May, this implies that core inflation must slow from the nearly 0.4 percent pace per month from last November to a 0.1 percent pace per month over the remainder of this year (a less plausible outcome).

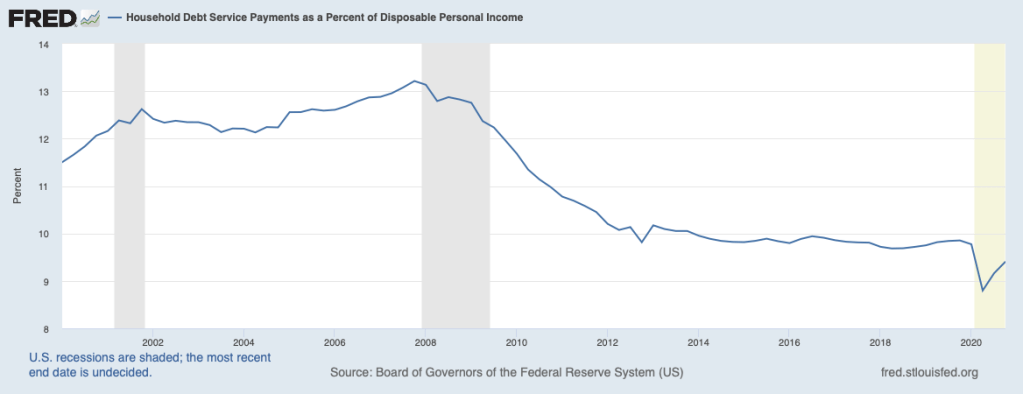

Going forward, the potent mix of very strong demand—powered by the ultra-low interest rate policy of the Fed and outsized fiscal stimulus already in place—pressing against restraints on supply in many sectors of the economy will mean continued upward pressure on prices. On the demand side, consumers are well-positioned to spend based on steady income growth, very strong wealth positions (buoyed by lofty stock prices and soaring home equity), accommodative credit conditions, and extremely low debt-service claims. The next chart illustrates that consumer debt service (interest plus scheduled principal payments relative to disposable personal income) is at historic lows, implying that consumers have plenty of capacity to finance big-ticket purchases in the period ahead. This includes the capacity to purchase homes at historically low mortgage rates (see May 31, 2021 post, The Economy: Housing Bubble Redux?).

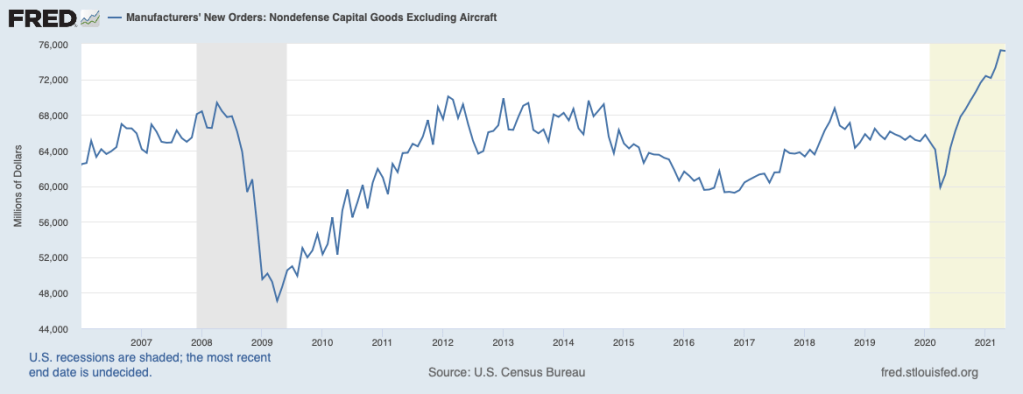

Businesses, too, are well-positioned to undertake new investment based on low financing costs, favorable credit availability, and solid prospects for sales. Indeed, new orders for capital goods (excluding the volatile aircraft component), shown next, have been rising rapidly over the past year and are likely to continue on an upward trajectory.

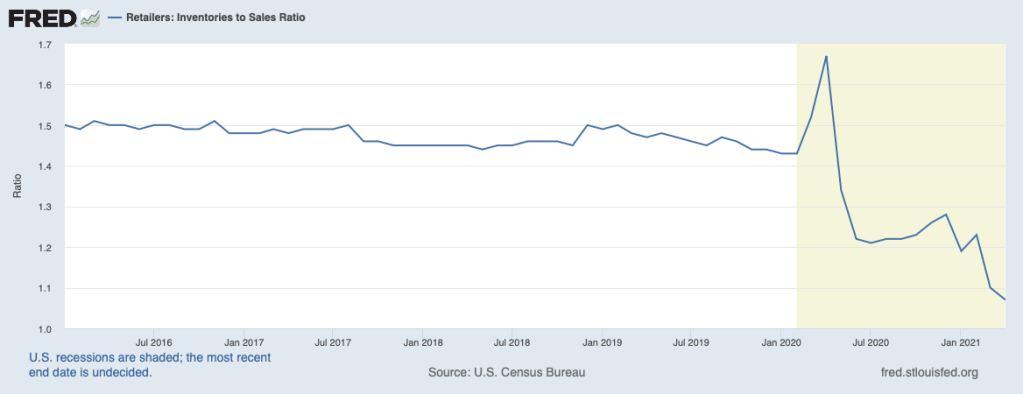

Adding to pressures on resources will be the need for retailers to restock empty shelves. The next chart illustrates that retail inventories are nearly one-third below normal levels (motor vehicle inventories are fully 60 percent below normal). Lack of availability of such goods has been holding down sales across a broad category of items, including homes, for some months.

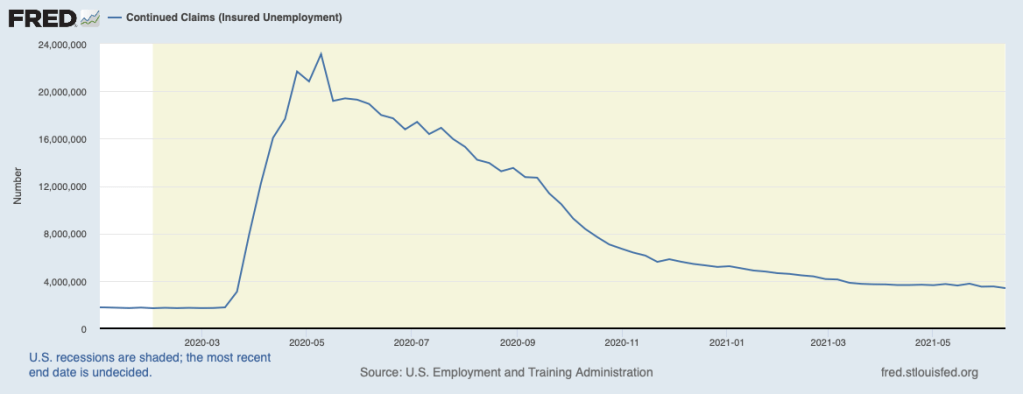

On the supply side, significant restraints continue. Supply-chain bottlenecks have yet to ease for products using computer chips, building materials, and certain other items. In addition, employers are facing serious hiring difficulties (see June 13, 2021 post, The Economy: Greater Strains Have Become Evident). The next chart shows that continuing claims for unemployment insurance have not changed much over recent months and remain more than one million above normal even though new claims for unemployment insurance have been dropping. Stubbornly high continued claims suggest that a lot of workers have elected to continue to collect unemployment insurance benefits, including the $300 per week federal supplement, even as job openings and help wanted signs continue to proliferate. The federal supplement is being removed in the near term by half of the states and is scheduled to end for the rest of the states in September. The bulk of the other supply restraints will be resolved over time, but, in the meantime, they will be placing upward pressures on prices.

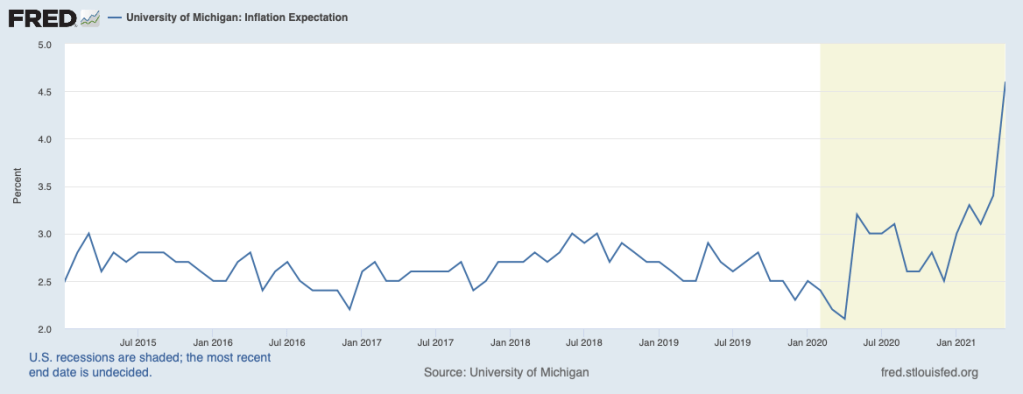

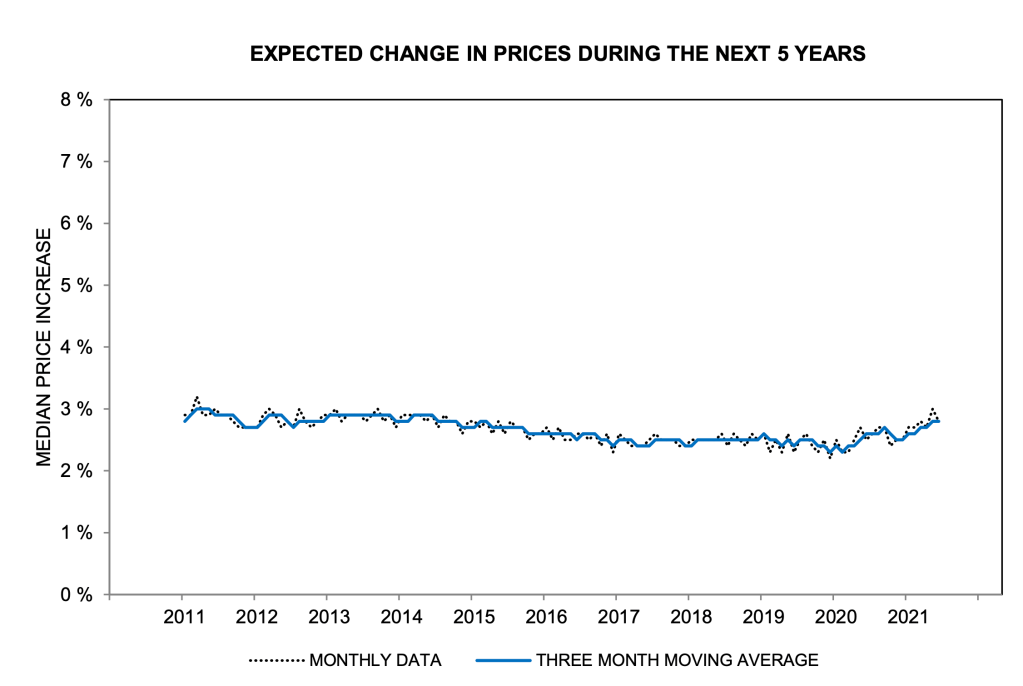

Whether we can avoid inflation becoming a new normal will rest importantly on whether the public comes to expect that inflation will be much higher going forward—that is, whether inflation expectations rise outside the 2 percent area. The chart below has year-ahead expectations of inflation based on the University of Michigan survey of consumers. This measure of inflation expectations has spiked in keeping with the recent pickup in actual inflation. Longer-term inflation expectations of consumers, the next chart, have also moved higher over recent months but are not outside the range of recent history (which was associated with subdued actual inflation).

But, like other measures of inflation expectations, this measure is pointed upwards (see June 13, 2021 post). (Note that this measure tends to average around 3 percent even though actual inflation has run well below this pace, a well-known and consistent bias in this survey).

At this point, the Fed is seemingly threading a needle trying to achieve its 2 percent average inflation rate objective. It is risking that forthcoming pressures on prices will cause the public’s expectations of inflation to ratchet higher and unwanted inflation to get built-in. There is a dynamic that is unfolding now that is not understood very well and, in the past, has been associated with actual inflation running above expectations and model forecasts, resulting in inflation getting out of control. Should this happen again, the Fed will find itself behind the curve and will need to take bold action to get to its longer-run goal of 2 percent inflation. And the farther it falls behind the curve, the bolder and more disruptive the monetary action will need to be.

2 thoughts on “The Economy: Will Inflation Be Contained?”