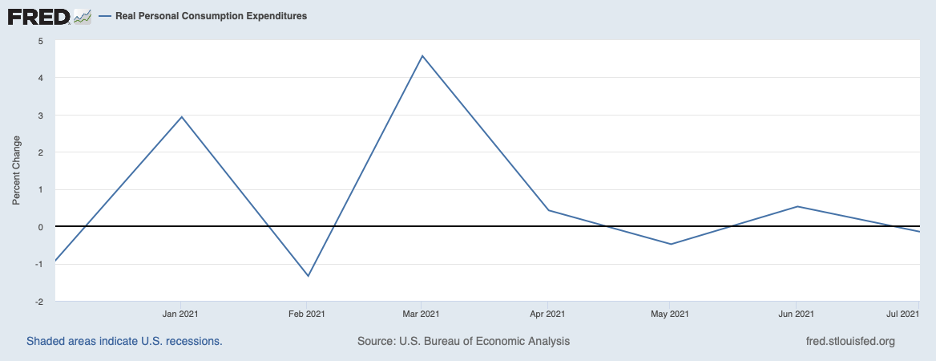

The economy has decelerated in the current quarter from the 6 percent plus rate of growth in the first half of the year. This slowdown has been most evident in spending by consumers. As shown in the chart below, growth in personal consumption expenditures—which account for nearly 70 percent of total output—has ground to a halt over recent months.

Real personal consumption expenditures have been flat since March.

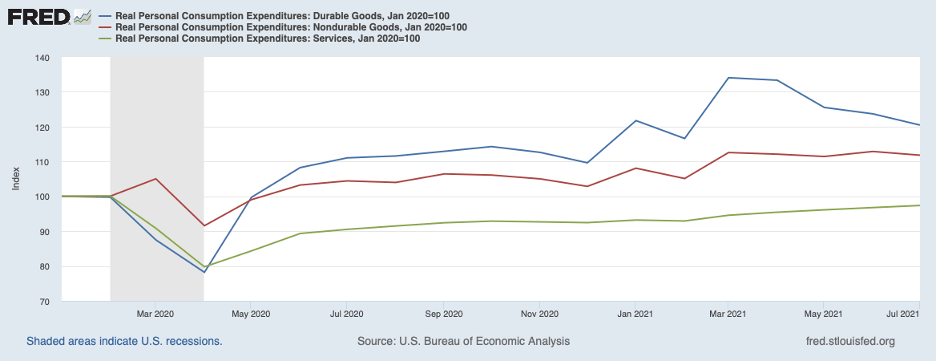

The next chart gives some insight into what accounts for the weakness in consumer spending in recent months. The chart shows spending patterns on the major components of real personal consumption expenditures in relation to their pre-pandemic levels—durable goods (the blue line), nondurable goods (the red line), and services (the green line). Despite being 20 percent above its early 2020 level in July, spending on big-ticket durables has declined over recent months. Over that same period, spending on nondurables has been flat but is still nearly 12 percent above its pre-COVID level. Meanwhile, spending on services, hit hardest by the lockdown, has continued on an upward path and had recovered all but 2-1/2 percent of COVID-caused losses by July.

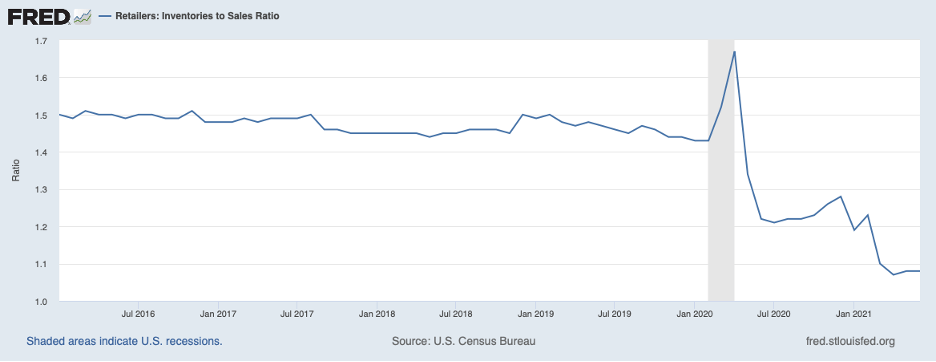

Has the slowdown in the economy owed to demand or supply factors? The next chart, showing the inventory-to-sales ratio at retailers points to supply-side factors, such as the shortage of chips and other supply chain disruptions. Retailers have been struggling to meet customer demands and rebuild their extraordinarily low inventories. This problem has been most acute in the durable goods sector, where the production of cars and light trucks, appliances, TVs, and computers continues to be crimped by long delays in getting chips. Perhaps you have noticed a paucity of cars and light trucks for sale on car lots and what remains has been picked over.

Supply-side problems also are revealed by prices. The following chart shows prices of each of these components–durable goods (blue line), nondurable goods (red line), and services (green line)—in relation to their early 2020 levels. The sharpest increases in prices over recent months have been for durable goods. Since December of 2020, prices of durable goods, which typically decline about ½ percentage point per year, have risen more than 6 percent (a 10 percent annual rate). Prices of nondurable goods and services—less affected by the chip shortage—have risen less rapidly than those for durables over this period (3.8 and 2.5 percent, respectively).

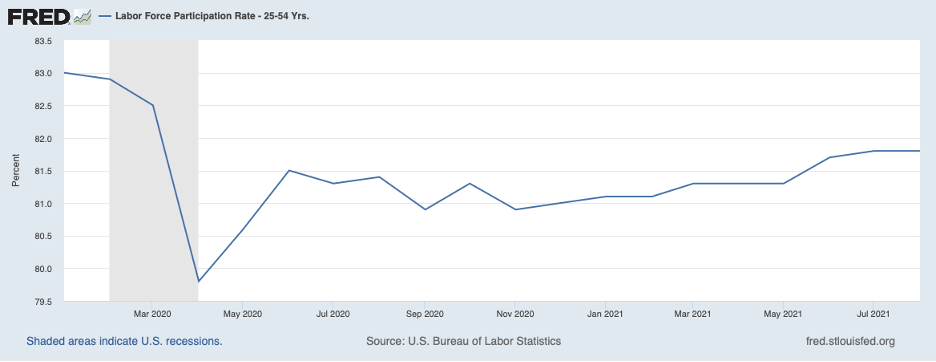

The employment report for August indicated that the slowdown in growth continues into the middle of the current quarter and that worker reluctance to re-enter the labor force is playing a role, another supply-side restraint. The chart below shows the labor force participation rate for persons aged 25 to 54 years, those in their prime working years. The participation rate dropped sharply at the onset of the pandemic and has recovered only a portion of that decline. And this reluctance to re-enter the labor force is happening at a time when job openings are at a historical record.

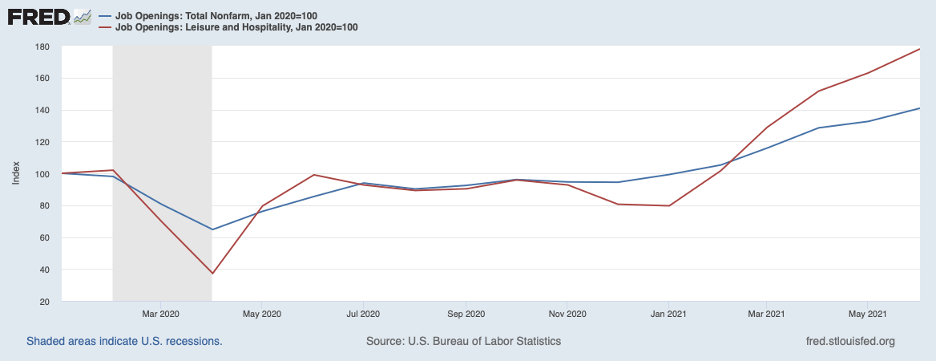

Shown next are job openings posted by nonfarm businesses overall (blue line) and the leisure and hospitality sector (red line), where strains have been most acute. Each is shown in relation to its pre-COVID level. Vacancies are up around 40 percent overall and 80 percent in the leisure and hospitality sector.

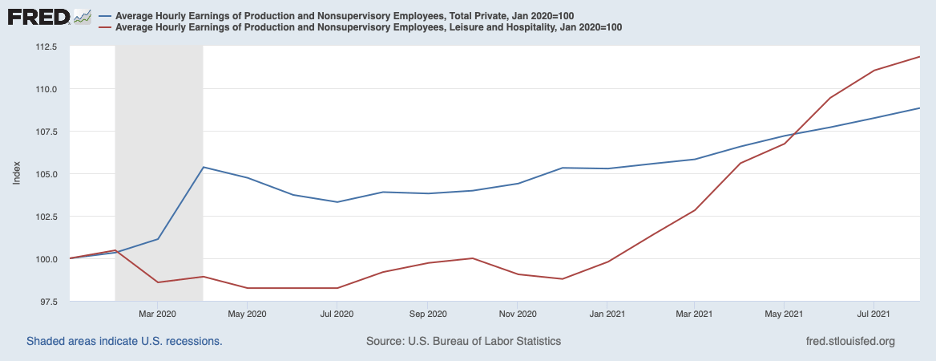

Competition for workers is adding to wage pressures. The next chart shows average hourly earnings for all employees (blue line) and the leisure and hospitality sector (red line), each in relation to its pre-pandemic level. Wages for all workers have risen nearly 9 percent above pre-COVID levels, while those in leisure and hospitality have risen 12 percent. All of the increase in the leisure and hospitality sector has occurred since January of this year, in keeping with the surge in job openings. The cost pressures coming from the pickup in wages will be continuing to boost consumer prices in the months ahead.

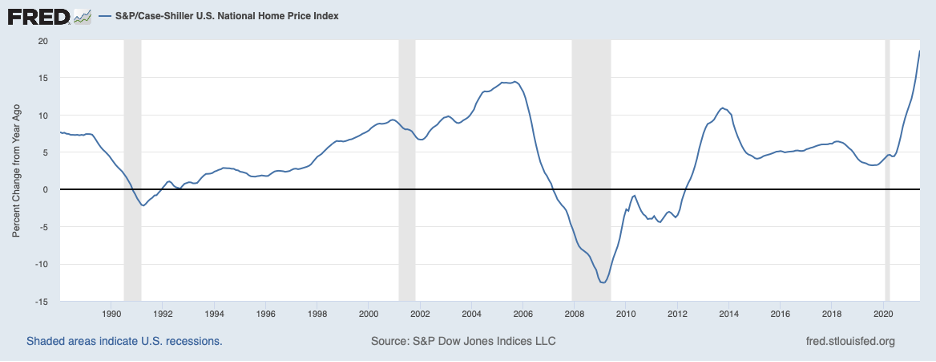

The housing sector continues to face intense price pressures, as shown in the next chart. In recent months, the twelve-month change in home prices has surpassed the pace during the peak of the housing bubble of nearly two decades ago.

The surge in home prices has been pulling the ratio of home prices to rent—a rough gauge of whether another bubble is developing—further above its normal range, shown below. Some of the increase since the spring of 2020 can be attributed to ultra-low interest rates stemming from the Fed’s highly aggressive monetary policy. But even allowing for low interest rates, home prices are becoming stretched in relation to rents as this gauge has moved into amber-light territory and is pointed higher. This is an area that deserves close watching.

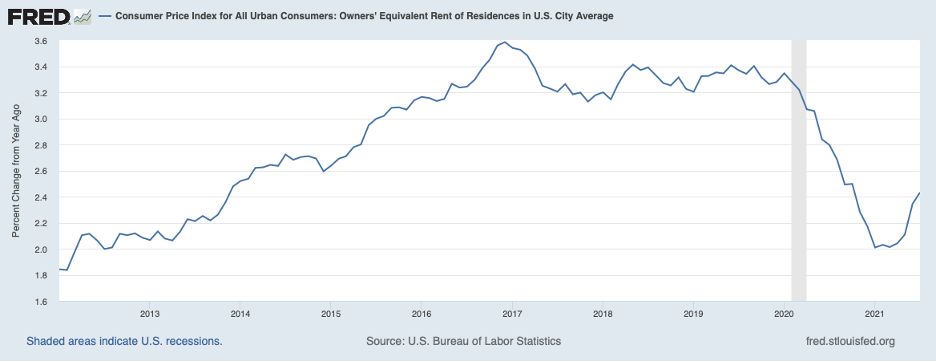

Note that home prices do not enter into measures of consumer prices directly. But they do affect consumer prices indirectly to the extent that they affect rent (including owner’s-equivalent rent). The growth of rent slowed in response to the COVID shock and the moratorium on rent payments, as seen in the next chart. It has picked up recently but is well below its pre-pandemic pace.

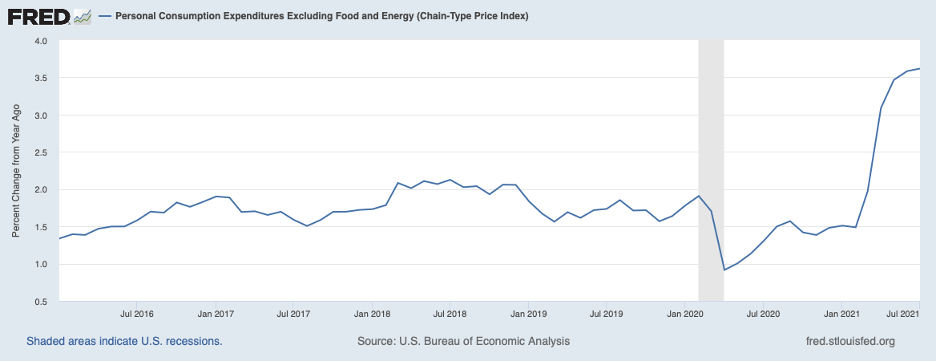

The pickup in consumer prices, boosted by prices of durables, is shown next by a closely watched measure of consumer price inflation. This chart displays the twelve-month percent change in average prices for all goods and services excluding the volatile food and energy categories. In the past couple of months, this measure of inflation has surpassed 3-1/2 percent.

As noted in recent commentaries (see, August 13, 2021, Supply Restraints Continue to Hold Back the Economy, and June 25, 2021, The Economy: Will Inflation Be Contained?), the Fed has indicated that it sees inflation above 2 percent for a period of time to compensate for several years of shortfalls in order to bring average inflation up to 2 percent. Thus it would appear that the Fed will tolerate above 2 percent inflation for a while longer before raising its target for the federal funds rate. Of some concern, though, is the Fed has been underpredicting inflation for some time. For example, as recently as June, the median forecast of inflation for the full year 2021 by Fed policymakers was 3.4 percent. However, by July inflation had reached 3.9 percent, implying that prices would need to decline on balance over the remainder of the year for this forecast to be realized—not very likely at all.

Looking ahead, we can expect some consumer price pressures to ease as supply-chain bottlenecks unwind and workers return to the labor force to fill job vacancies. Whether the Fed will be able to achieve its 2 percent average inflation objective will depend on how long some of these temporary factors persist, and, more importantly, whether the current bout of inflation leads businesses and households to expect above 2 percent inflation going forward. As noted in a recent commentary (see, August 13, 2021, Supply Restraints Continue to Hold Back the Economy), both households and professional forecasters have been steadily marking up their expectations of inflation and any further increases could pose a dilemma for the Fed. In these circumstances, one cannot rule out the Fed falling behind the curve on inflation, leading to disruptions to financial markets and the economy. Stay tuned.