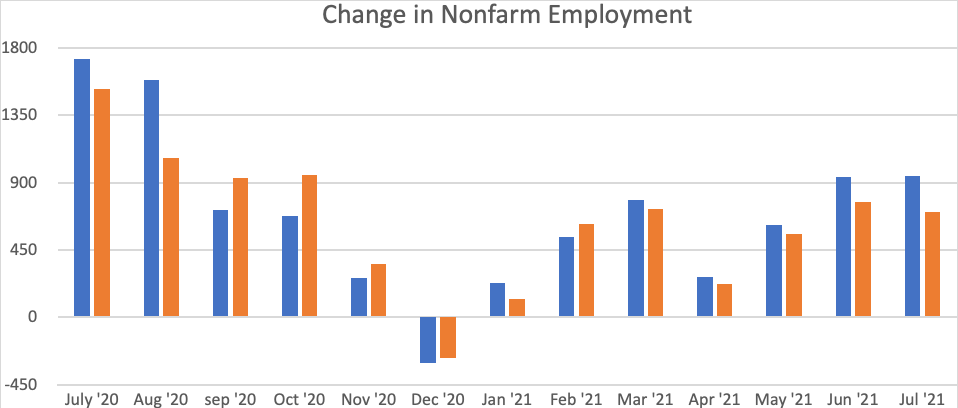

The employment report for July was widely hailed as a strong report. Total nonfarm employment rose nearly 1 million (943,000, the blue bar in the chart below) and the unemployment rate dropped 1/2 percentage points to 5.4 percent. However, as in June, a sizable portion of the gain in employment occurred in the state and local government sector. This likely owes to technical problems stemming from efforts to adjust for intra-yearly seasonal variations in public school educators caused by COVID-related disruptions (see July 8, 2021 post, The Economy: Lots of Demand, Not So Much Supply). When government workers are removed from the total, the increase was 703,000, similar to the increase in July (orange bars in the chart below). The shortfall in private employment from the February 2020 peak is nearly 5 million workers or 4 percent. At the rate that private payroll growth has occurred over recent months, it will take until next February before private employment has returned to pre-pandemic levels.

Source: Bureau of Labor Statistics, Monthly Labor Report (July 2021).

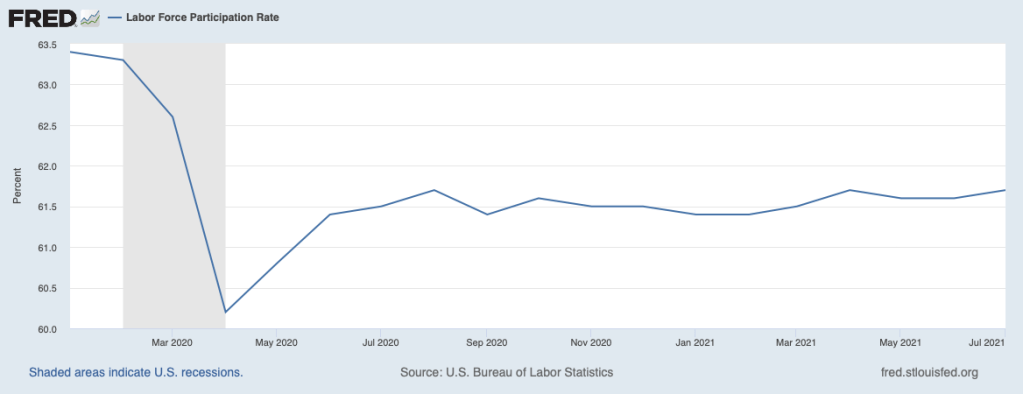

As noted in recent commentaries (see August 2, 2021 post, The Economy: What Have We Learned From the Second Quarter? and July 8, 2021 post, The Economy: Lots of Demand, Not So Much Supply), the recovery of the labor market—and economic growth—has been held back by a reluctance of people to return to the labor force. The next chart illustrates that, while the labor force participation rate ticked up last month, it is still 1-1/2 percentage points below early 2020.

And this reluctance to re-enter the labor force is occurring despite record job vacancies, shown next.

Indeed, the number of job openings now exceeds the number of unemployed persons, shown on the following chart. This has contributed to a very tight labor market.

What accounts for the continued reluctance of workers to remain on the sidelines? Concerns about contracting COVID on the job and the need to remain at home to attend to children unable to return to school (including pre-school) have frequently been mentioned. However, the participation rate did not recover much while vaccinations were increasing rapidly and the incidence of COVID was diminishing. Various government programs that have made it easier to stay at home—generous extended unemployment benefits and the moratorium on rental and student loan payments—also have contributed to the reluctance. Enhanced unemployment benefits have been expiring in roughly half the states and are scheduled to expire in the rest in September. The moratoriums on rent and student loan payments have been extended by executive order and would be extended even further under the $3-1/2 trillion “infrastructure” bill currently being considered by Congress.

There are only hints to date that the removal of supplemental unemployment benefits in some states is inducing people to return to the workforce. The next chart shows that the share of those unemployed who have been unemployed for twenty-seven weeks or longer has begun edging lower on net over recent months as supplemental benefits have been lifted.

A similar pattern can be seen in the number of people collecting unemployment insurance benefits, the next chart. That number ticked lower through the end of July.

The tightening in the labor market can be seen in the upturn in average hourly earnings—the next chart. Growth in average hourly earnings picked up further in July.

Moreover, the pickup is understated because a disproportionate share of newly hired workers have been in lower-wage occupations, tending to pull down the average.

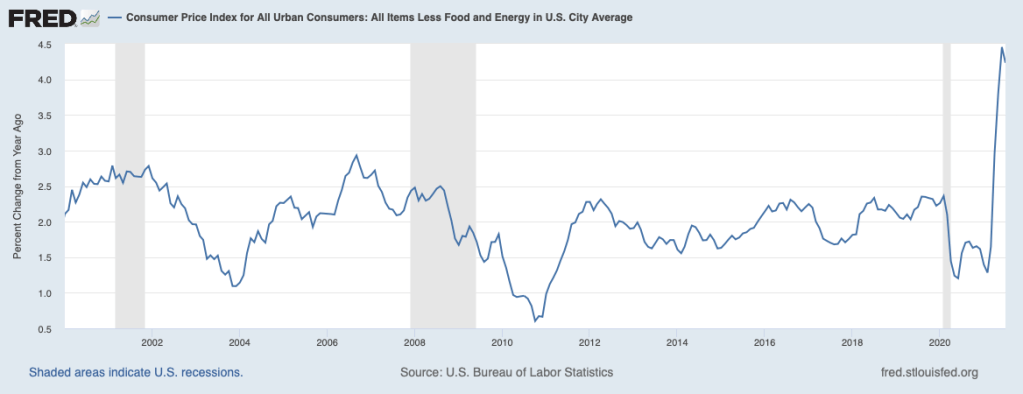

The tightening labor market and supply chain disruptions are contributing to faster inflation.

The consumer price data (CPI) for July showed large price increases again last month, charted above for the twelve-month change for all items excluding the volatile food and energy components. The categories registering outsized increases were again those affected by chip shortages and supply chain disruptions (see August 2, 2021 post, The Economy: What Have We Learned from the Second Quarter?)—new cars and trucks, TVs, computers and peripherals, and appliances. In addition, the price of food away from home showed another big increase as growth in wages in the hospitality sector, chart below, picked up more.

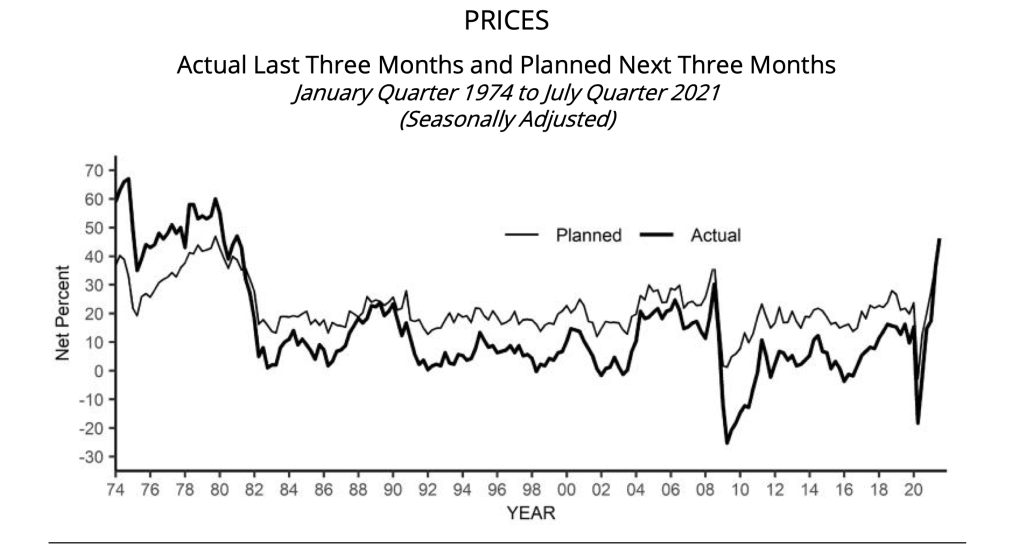

Small businesses more broadly report that labor and other cost pressures are leading them to raise prices, as shown in the next chart. The thick line illustrates the percent of respondents to the monthly National Federation of Independent Businesses (NFIB) survey that have raised their prices through July. This share of respondents has climbed to levels last seen in the late 1970s and early 1980s—when ravaging inflation gripped the nation. The thin line shows that a similarly large share of respondents plan to raise prices over the next three months—suggesting that inflation is not going away anytime soon.

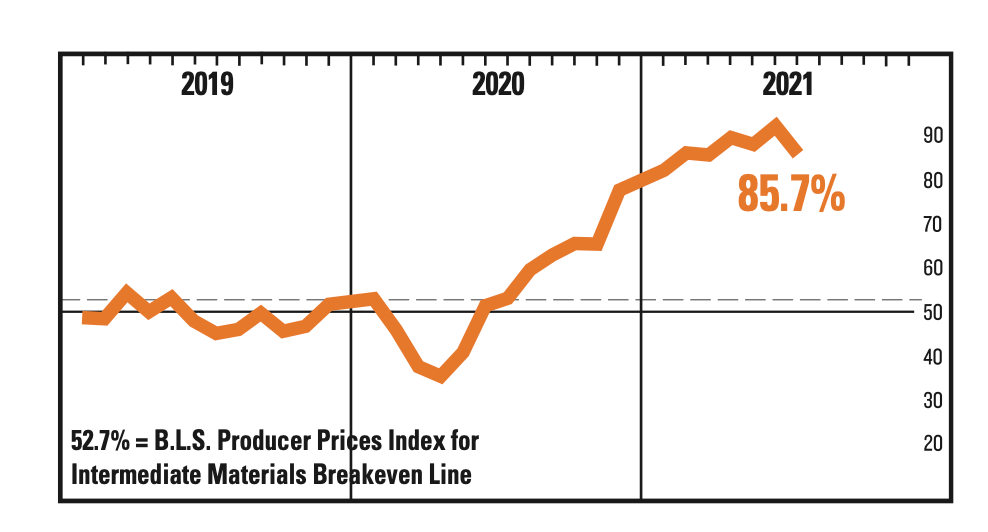

Also pointing to upward pressures on inflation is the following chart from the Institute for Supply Management (ISM)—representing larger businesses—report for July. The chart presents an index of prices paid for intermediate inputs which has stayed in extremely high territory—territory that typically leads to sizable increases in the prices of goods that these businesses sell.

ISM Input Prices

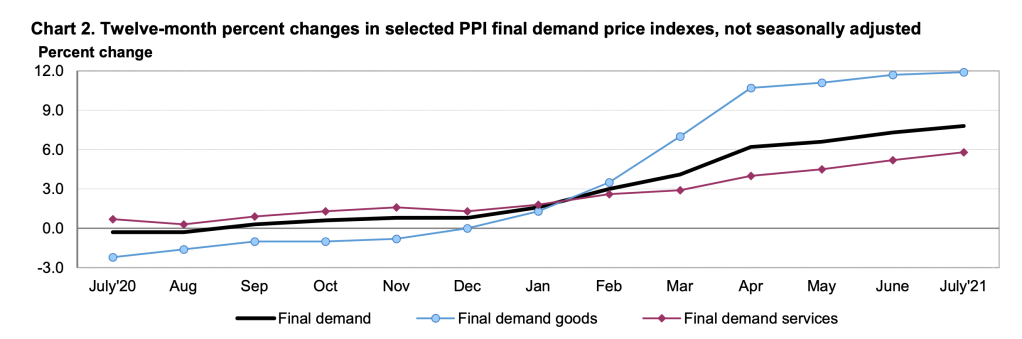

Faster increases in producer prices more broadly were displayed in the July Producer Price Index, next chart. The pickup has been most pronounced in the prices of goods (light blue line) which have been increasing at a double-digit rate in recent months. The accompanying cost pressures on sellers will be boosting consumer prices in the period ahead.

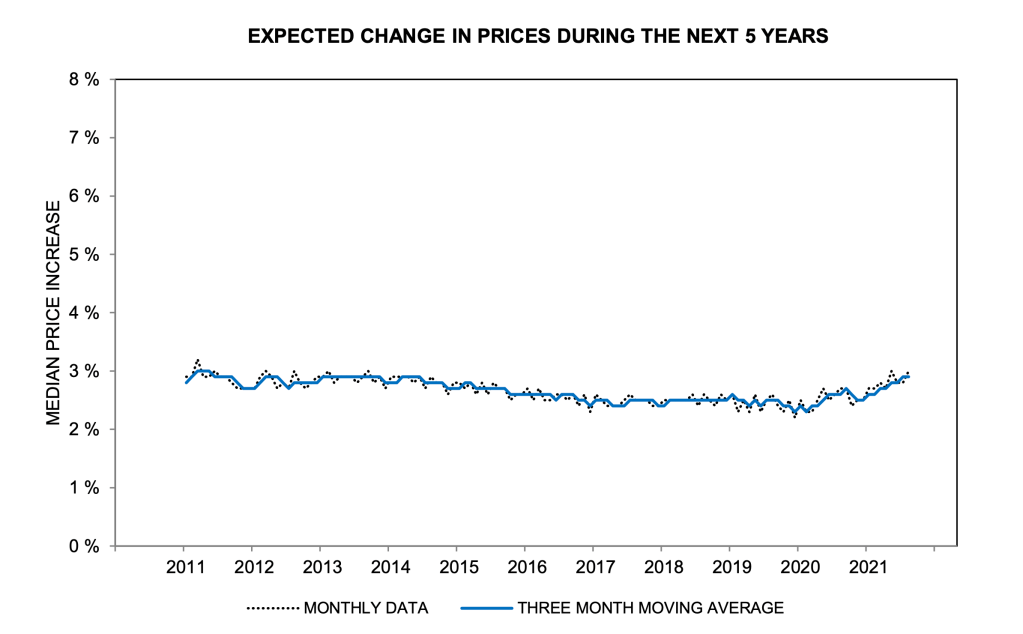

As noted in other postings, critical to whether the current bout of inflation will be transitory or lasting will be the behavior of inflation expectations (see June 25, 2021, The Economy: Will Inflation Be Contained? and August 2, 2021, The Economy: What Have We Learned from the Second Quarter?). Shown next is the Michigan survey of longer-term inflation expectations of consumers through early August.

Inflation expectations have been moving higher over recent months, climbing into the upper reaches of the past decade. A very similar story is being told about longer-term inflation expectations by the professional forecasters, the next chart.

Should this upward drift in inflation expectations continue, the Fed will be confronted with a dilemma—whether to tighten policy to rein in inflation expectations and inflationary pressures or whether to continue with their announced policy of aggressive accommodation (see, August 2, 2021, The Economy: What Have We Learned from the Second Quarter?).

To sum up, supply restraints are continuing to curb economic growth and place upward pressure on inflation. Some of these inflationary pressures will ease as supply chain disruptions abate. Also, holding back growth and boosting inflation has been a reluctance of workers to return to the labor force. Progress on this front is less certain and heavily dependent on prospective federal legislation. Meanwhile, keep a close watch on whether inflation expectations continue to ratchet higher. The coming months are going to be a major test of the Fed and other policymakers.

One thought on “Supply Restraints Continue to Hold Back the Economy (Revised)”