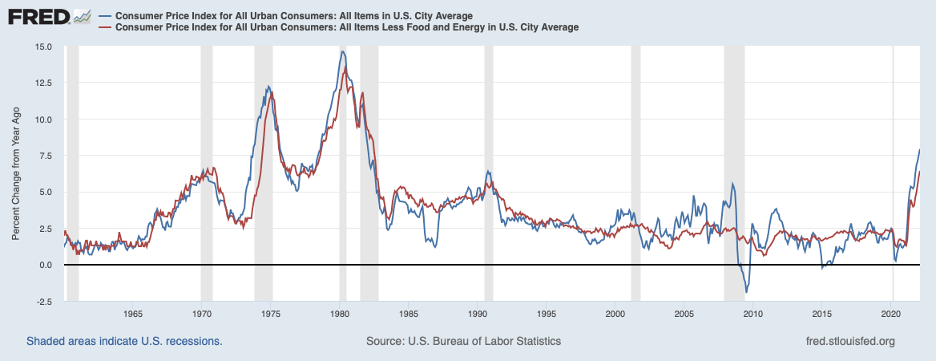

The latest news on the inflation front has not gotten any better. The Consumer Price Index (CPI) rose 7.9 percent over the twelve months ending in February, the blue line in the chart below, and, even after removing escalating food and energy prices, the CPI rose 6.4 percent, the red line.

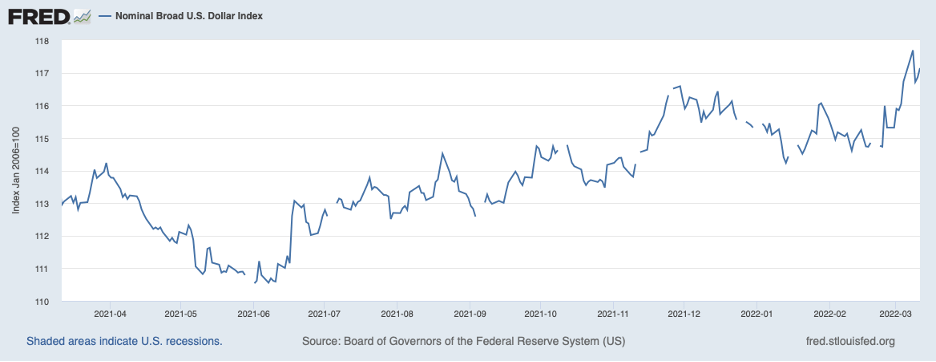

These measures are up sharply from a year earlier when both measures had increased only about 1-1/2 percent. Moreover, rising prices have become more widespread across categories of goods and services. This upturn in inflation has been taking place at a time when the dollar has strengthened against the currencies of our major trading partners, the next chart.

The stronger dollar has been acting to hold down increases in the prices of imports as well as the prices of domestic goods that compete with them.

Not surprisingly, according to public opinion polls, inflation (notably the surge in the price of gas at the pump) has become the number one concern facing the nation. The Federal Reserve at its mid-March meeting acknowledged that the inflation situation will require removing the considerable amount of monetary stimulus that has been in place during the past two years. At that meeting, the Fed raised the target for the federal funds rate 25 basis points and signaled that it would continue to raise this rate 25 basis points at each of the remaining six meetings this year. At the same time, the Fed conveyed that it envisions making four more 25 basis point rate hikes in 2023—stopping at a level of the funds rate of 2-3/4 percent—to put inflation on a downward path toward the Fed’s 2 percent target. The Fed also indicated that it will accompany rate hikes with a paring of assets from its balance sheet which ballooned $5 trillion since March 2020. Whether these measures will be sufficient depends on how entrenched inflation has become.

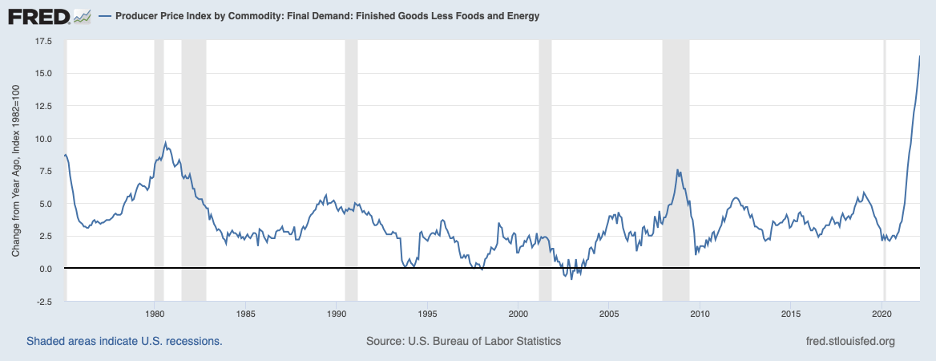

We can expect little inflation relief in the months ahead. Supply chain disruptions, which have been adding to inflation pressures for more than a year, are being aggravated by dislocations in recent weeks caused by the war in Ukraine and by reported production shutdowns in China stemming from outbreaks of COVID. The next chart shows that finished goods prices at the producer level continued their steep upward march through February, which will be adding to consumer price inflation in the coming months.

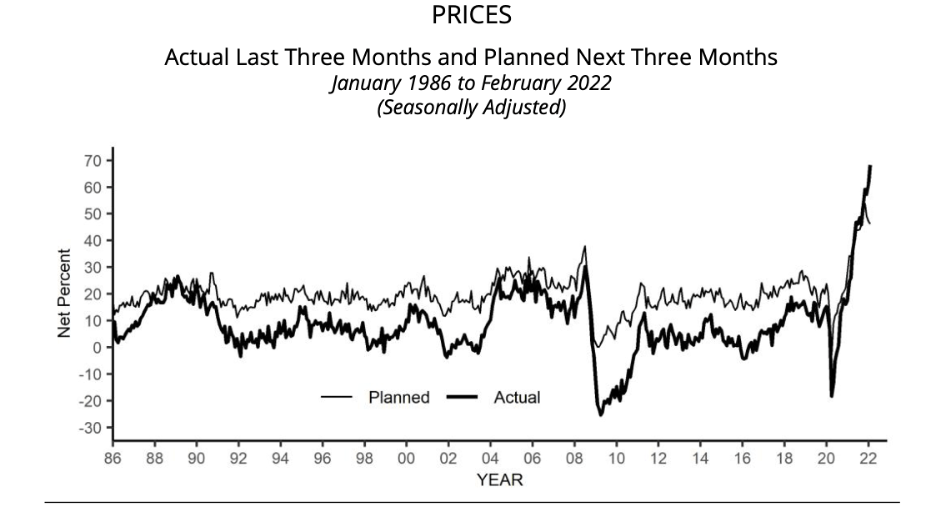

Further pointing to high inflation in the months ahead is the most recent survey by the National Federation of Independent Businesses (NFIB); nearly the same proportion of small businesses that raised their sale prices in the past three months, the thick line in the chart below, noted that they plan to raise their sale prices in the coming three months, the thin line. Additionally, once the dollar stops strengthening, this restraining force that has been holding down the prices of imports will be removed.

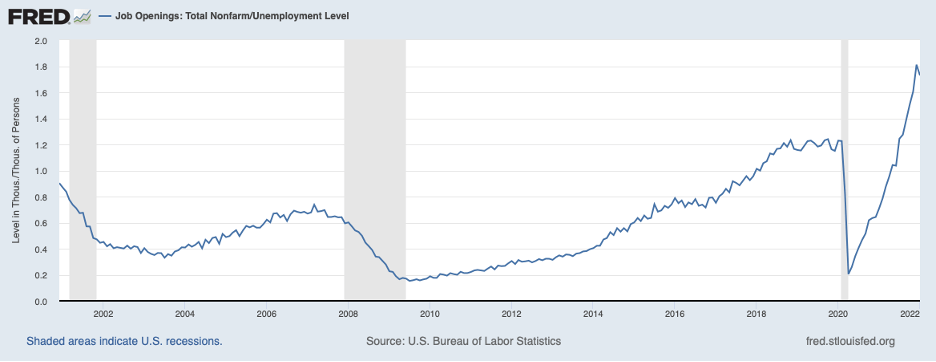

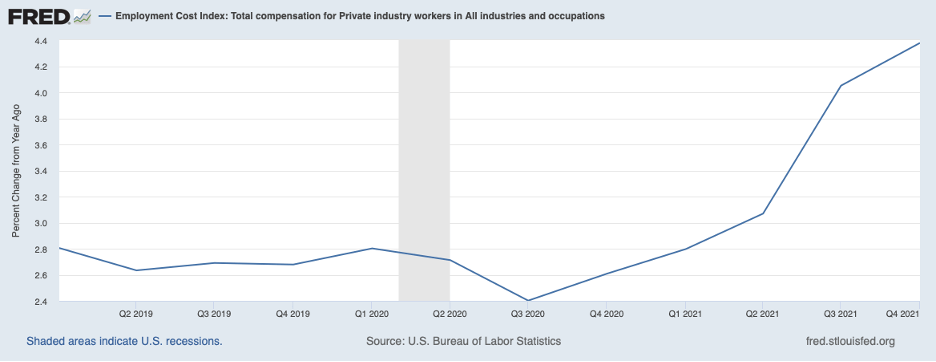

Conditions in the labor market also point to substantial upward pressure on prices in the months ahead. The next chart shows the ratio of job openings to the number of unemployed persons, an indicator of the tautness of the labor market. The chart shows that the excess of job openings over the number of unemployed remains in unprecedented territory, implying a very tight labor market. Employers have been responding by boosting growth in compensation, shown in the following chart that goes through the end of 2021.

Various reports indicate that competition for workers has remained intense more recently, and this competition is being reflected in continued large increases in compensation. Employers can be expected to respond to rising labor costs by raising the prices that they charge consumers.

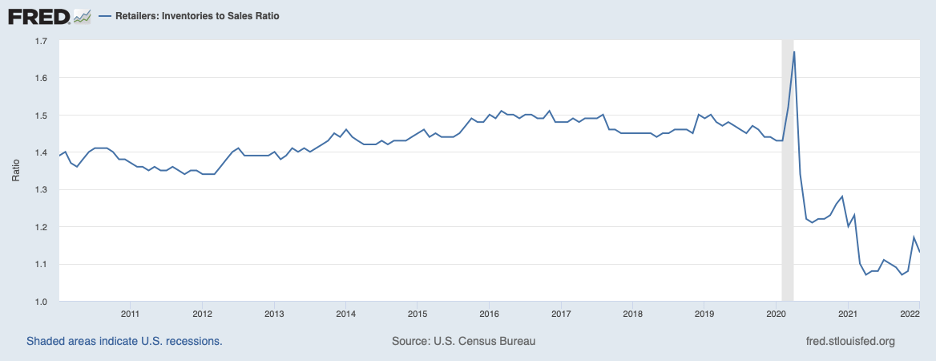

Further adding to pressures on resources in the months ahead is the need for retailers to step up orders to rebuild inventories. The next chart shows the inventory-to-sales ratio at the retail level. Despite considerable effort, retailers have made little progress to date in rebuilding stocks, which remain extremely lean. Retailers’ elevated orders will continue to pressure suppliers to boost production—and employment.

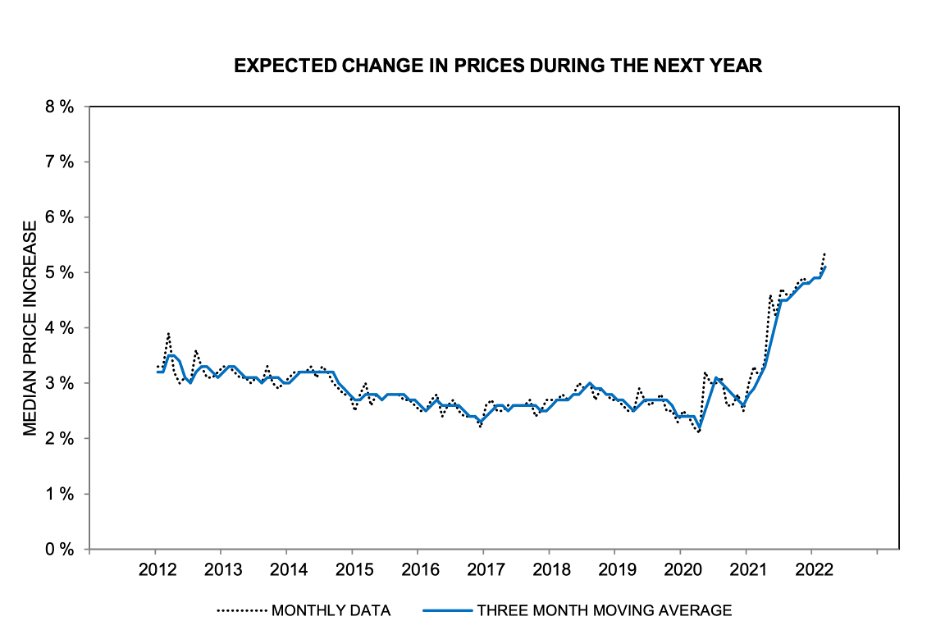

Brisk inflation and prospects for more of the same are leading to upward revisions in inflation expectations, as shown in the chart below for consumers in the Michigan Survey Research Center for early March. Consumer expectations for inflation in the year ahead have risen smartly in recent months. Higher inflation expectations strengthen inflation momentum.

Inflation has become more entrenched and consequently has become more difficult for the Fed to subdue. In the coming months, inflation could well run even further above the Fed’s 2 percent target before leveling off. The Fed’s preferred measure of inflation, the Personal Consumption Expenditures index, rose 5.5 percent in 2021 well above the target and the 1.8 percent rate projected at the end of 2020. For 2022, the Fed foresees inflation slowing to 4.3 percent. To achieve this, monthly increases in prices would need to slow to 0.3 percent from nearly 0.6 percent over the past four months. This seems highly unlikely given the view of the forces in place that have been mentioned above.

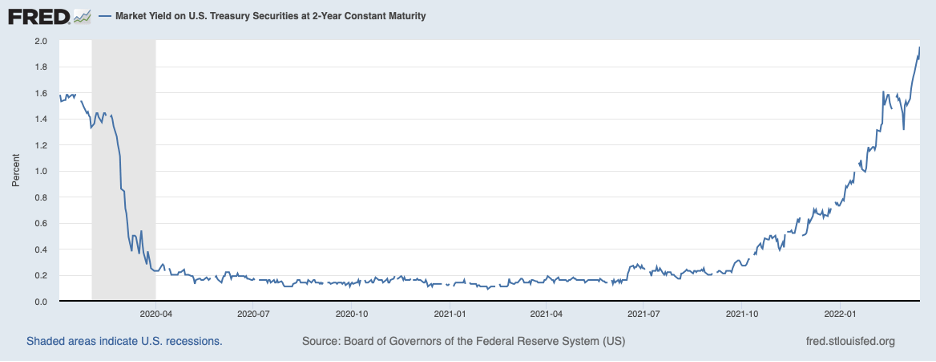

In light of these considerations, the federal funds rate will need to be raised above the underlying rate of inflation by some margin (that is, the real federal funds rate will need to be distinctly in positive territory), implying that the Fed will need to increase the federal funds rate well above the 2.8 percent level that was included in their recent projections. Financial market participants also have come to expect the federal funds rate to rise above 2.8 percent. The next chart shows the interest rate on a two-year Treasury note which has risen sharply in recent weeks to 1.95 percent. This rate on the two-year note implies that the federal funds rate is expected to be nearly 3.25 percent by the end of next year, 50 basis points above the Fed’s expectation.

But even the level embedded in Treasury yields would not exceed inflation by enough to counter the current momentum in the inflation process. The sooner that the Fed and market participants come to realize the need for greater monetary restraint, the more quickly inflation can be placed on a solid downward trajectory. Meanwhile, get ready for some excitement in financial markets in the coming months.