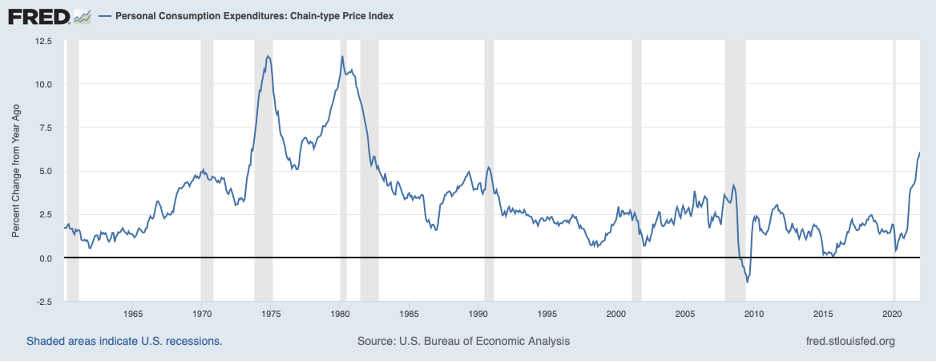

You have almost certainly discovered that prices at the pump have jumped over recent days. Unfortunately, pump prices are still headed higher. The Russian invasion of Ukraine has disrupted the global oil market and pushed energy prices higher. This impact is coming at a time when inflation is running at the fastest pace in four decades. As seen in the chart below, the Personal Consumption Index (PCE)—the Fed’s chosen measure of consumer prices—increased 6.1 percent over the twelve months ending in January, up from 1.4 percent over the previous twelve-month period.

Moreover, inflation picked up over the past year and averaged a 7 percent annual pace over the four months ending in January. At the same time, price increases became more pervasive across goods and services categories. Against these developments, the inflation outlook is a matter of concern.

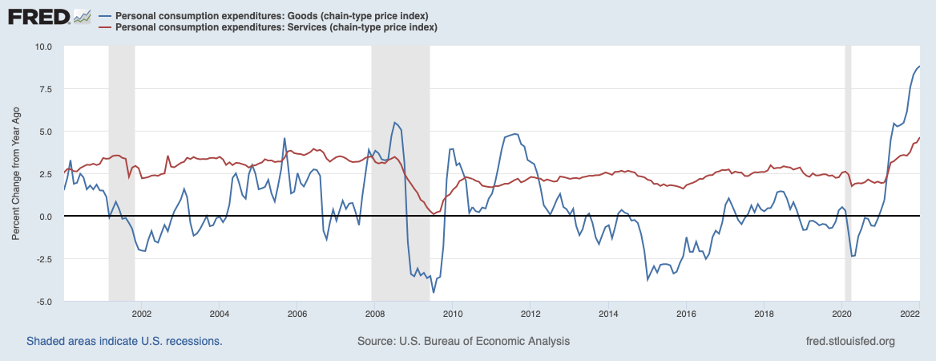

As noted in other commentaries, inflation over 2021 was boosted by supply chain disruptions—especially for microchips and goods that utilize microchips—and by a reluctance of some workers to return to the workforce despite an abundance of jobs. Supply chain disruptions primarily affect goods prices, represented by the blue line in the chart below. Over recent decades, goods prices had been subdued on balance but have climbed to the double-digit area in the past couple of months. Labor shortages have been affecting the prices of both goods and services, with some service prices affected appreciably. The red line in the chart above illustrates that service prices also have accelerated a good bit over the past year.

Prospects for relief of supply chain disruptions in the months ahead are not very favorable. For example, the most recent Institute of Supply Management survey of manufacturers for February noted that order backlogs continued to grow, price pressures remained intense, and supply chain challenges persisted. The war in Ukraine and the various measures taken to isolate Russia—not to mention possible cyberattacks coming from Russia—will be compounding the supply chain problem in the period ahead and adding to inflation pressures. Regarding the oil market, futures prices suggest that the price of oil, which has climbed above $110 per barrel in recent days from around $75 per barrel at year-end, will remain above $100 per barrel until midsummer and then drift down gradually to around $90 per barrel by the end of this year.

Should other supply constraints ease up similarly, we can expect that measures of inflation will moderate later in the year. At issue is how much moderation is in the cards? It can be safely said that the Fed is going to miss its 2 percent target for inflation by a good bit again in 2022. Even if monthly increases in prices were to slow to 4/10 of a percentage point for the remainder of this year (from nearly 6/10 tenths over the four months ending in January), annual inflation would still be 5.2 percent—not much below the 5.8 percent increase registered for 2021.

To get inflation on a distinctly downward trajectory will require that the Fed deliver a series of interest rate hikes—increases in the target for the overnight federal funds rate—over the next couple of years. The amount of those rate hikes will depend on how intransigent inflation has become. The longer elevated inflation rates persist, the more intransigent inflation will become, and the greater will be the size of rate hikes needed. As noted, elevated inflation will persist for a while longer, implying more action will be required of the Fed to achieve its inflation target of 2 percent.

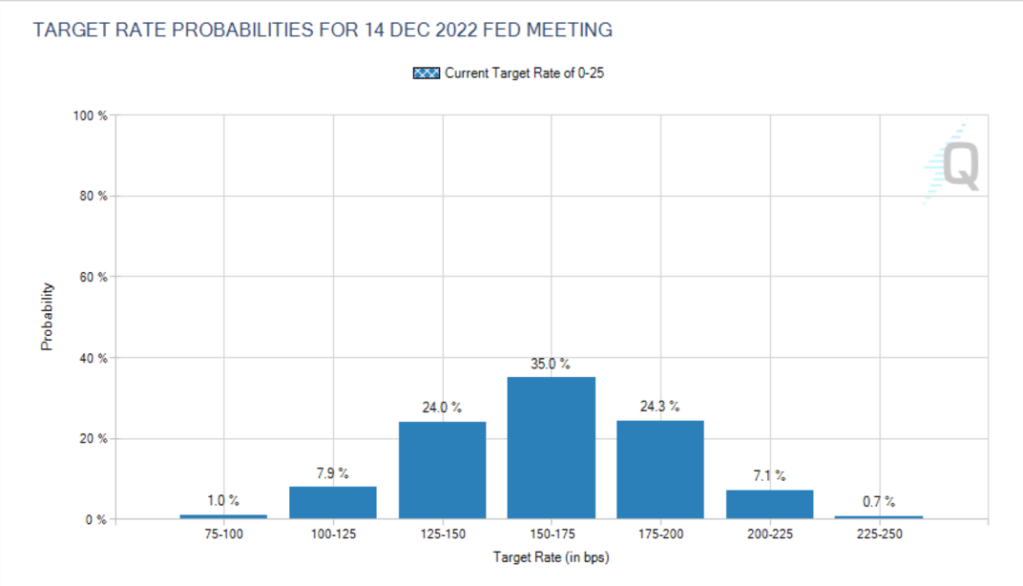

Fed Chair Powell has said that he will favor a 25 basis point increase at the upcoming mid-March FOMC meeting (from its current 0 to 25 basis point target) but has not specified how many more increases may be coming after that. The chart below shows futures market expectations for the federal funds at yearend. Market participants now see nearly a 70 percent chance that the federal funds rate will be raised 150 basis points or more by yearend—roughly 25 basis points per meeting at each of the seven additional meetings in 2022.

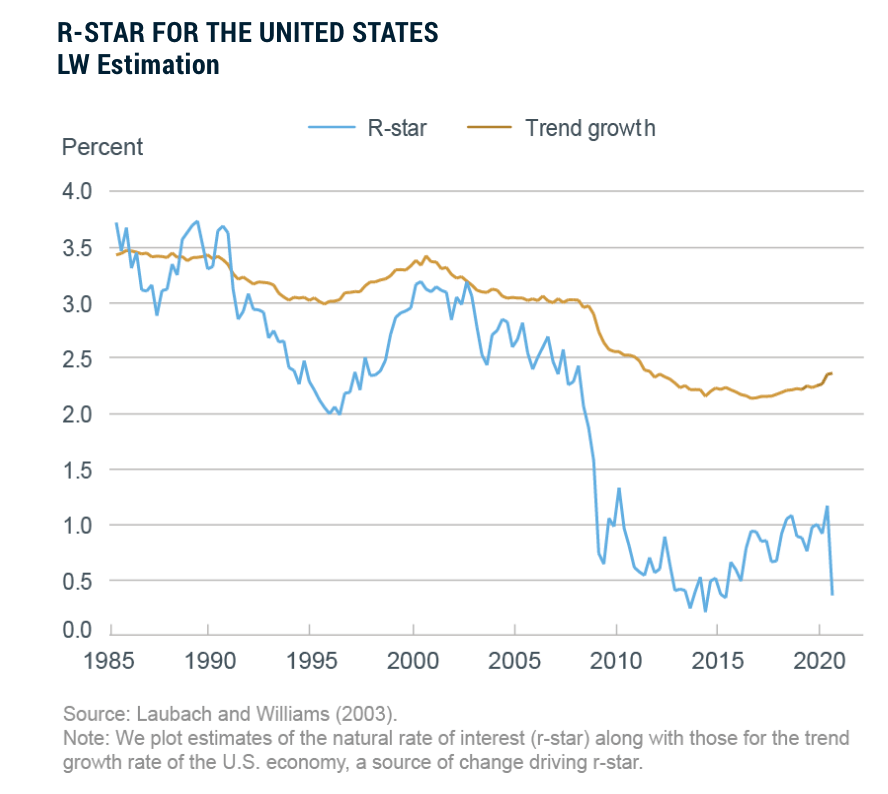

Will increases of 150 to 175 basis points in the federal funds rate be enough? The next chart shows the neutral real federal funds rate (R-star, the blue line)—that is, the extent to which interest rates must exceed the underlying rate of inflation for monetary policy to be neither stimulative nor restrictive. The most recent reading for the real neutral rate is around 50 basis points. The actual real interest rate currently is deeply negative because the Fed is setting the nominal federal funds rate at near-zero and inflation is running high.

However, to bring inflation down under present circumstances, monetary policy needs to be restrictive. This means that the real interest rate needs to exceed 50 basis points by a sizable margin. Even if underlying inflation were at the Fed’s target of only 2 percent, the federal funds rate would need to be a good bit above 250 basis points to be restrictive. However, inflation has been running well above 2 percent and various measures of inflation expectations foresee inflation over the next year or so exceeding 2 percent by a good amount. All of these considerations suggest that the federal funds rate will need to go a lot higher than currently envisioned by the Fed or market participants, thanks only in part to the Ukraine war. So much for the soft landing!