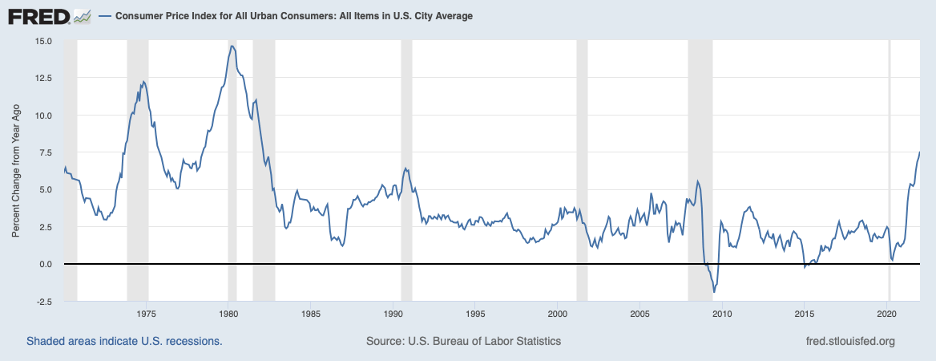

The recent news on the economy has been disappointing. The CPI rose 7.5 percent over the twelve months ending in January, shown in the chart below. This increase is the briskest since March 1982. Moreover, outsized price increases have become more widespread across various categories of goods and services, an indication that inflation has become more entrenched.

At the same time, there are mixed signs on the economy. Retail sales in January recovered losses posted in December while the Michigan survey of consumer sentiment in early February, the next chart, sunk to levels commonly associated with recessions (the shaded areas). Could we be entering a period of economic stagnation along with high inflation—stagflation?

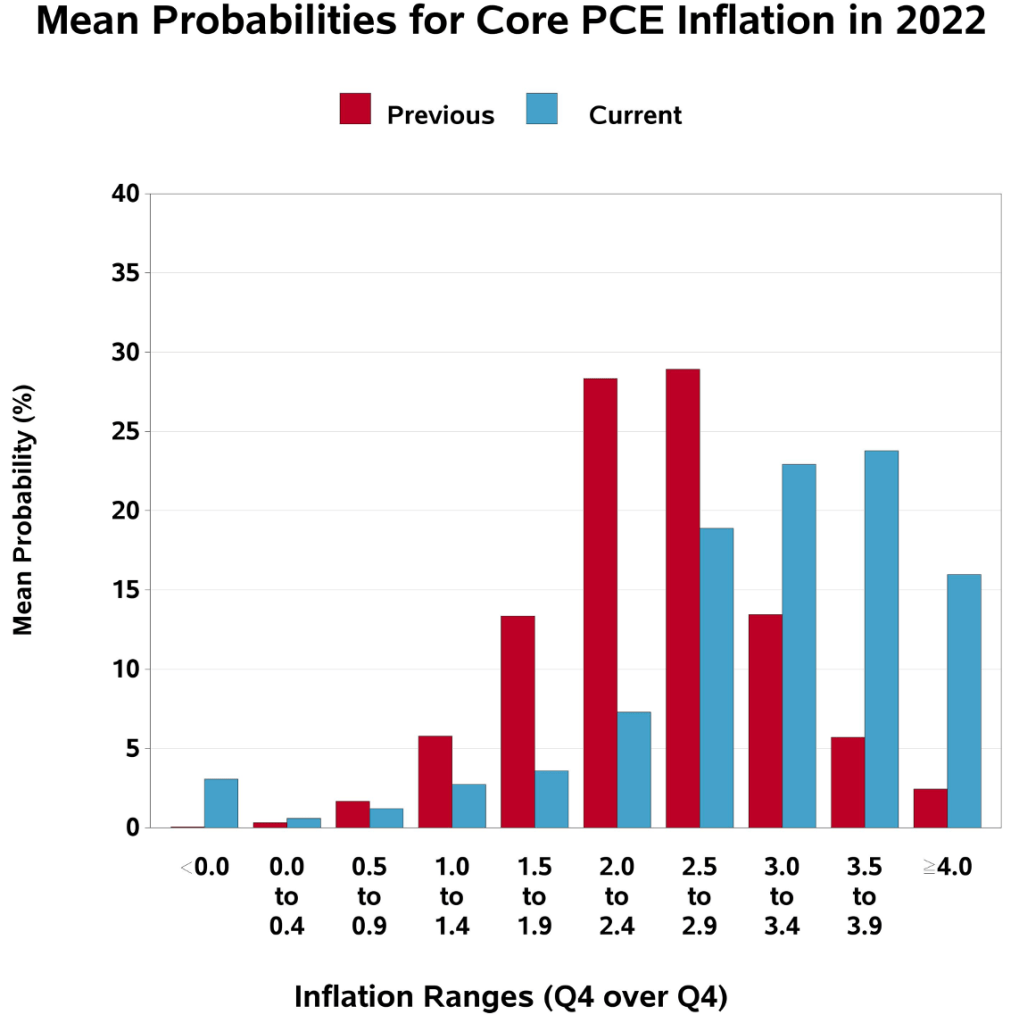

As noted in recent commentaries (see, What Will It Take to Tame Inflation?, January 31, 2022, and Tough Choices for the Fed, January 19, 2022), inflation has ratcheted higher. Also, the inflation trajectory has become more uncertain. The chart below displays the distribution of inflation forecasts for the current year—2022—by professional forecasters. The red bars show their forecasts made last November and the blue bars most recently. Not only have the projections for inflation moved higher, but the projections have also become more dispersed—implying more uncertainty regarding the inflation outlook.

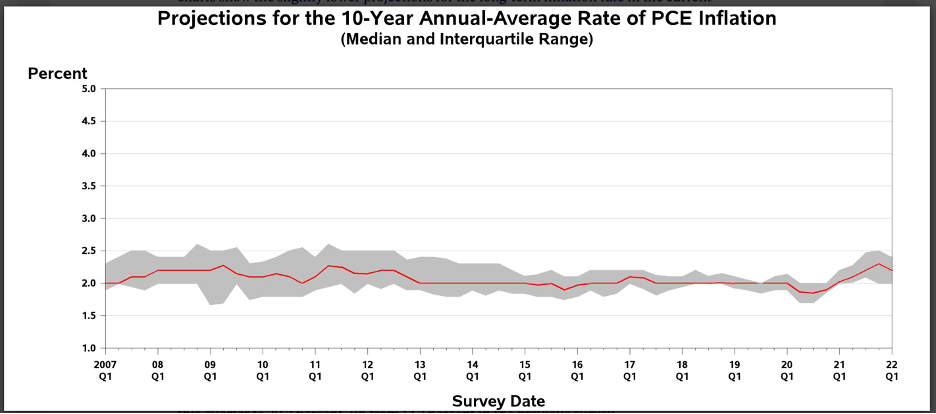

These forecasters also foresee inflation over the coming ten years being elevated and above the Fed’s 2 percent target, shown below.

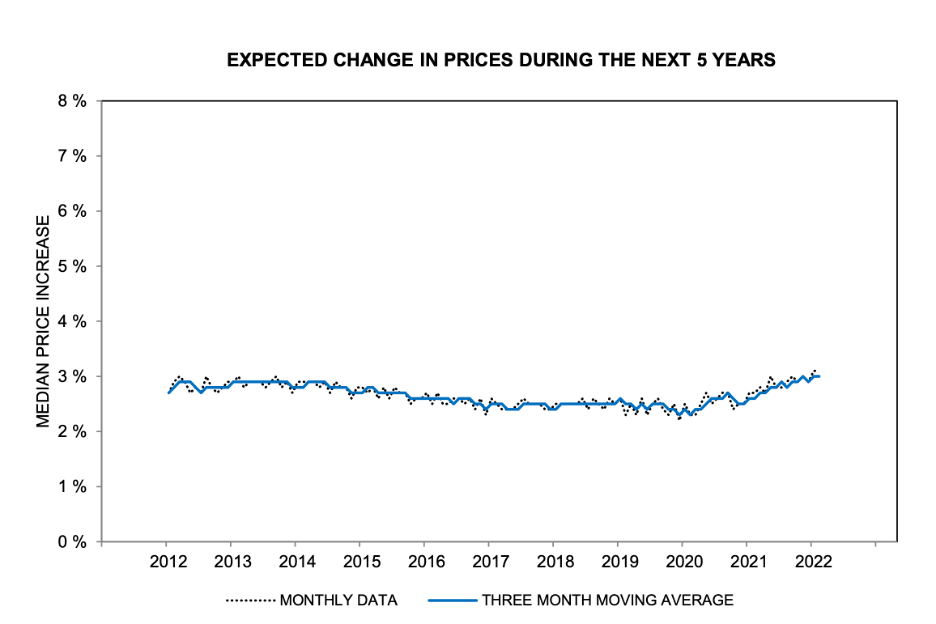

Consumers, too, are expecting higher inflation over coming years, the next chart (below).

These higher long-term inflation expectations are adding momentum to the inflation process and increasing the odds that the Fed will, to get inflation back under control, need to tighten monetary policy to the extent that the economic expansion stalls out.

Since March 2020, the Fed has implemented a highly accommodative monetary to counter the COVID shock. The Fed lowered its policy interest rate—the federal funds rate—to the rock bottom level of 0 to 25 basis points and resumed purchasing Treasury and mortgage securities in massive amounts. These measures have resulted in a considerable amount of monetary stimulus which has been accompanied by huge injections of fiscal stimulus.

At the upcoming monetary policy meeting in mid-March, the Fed assuredly will begin to remove monetary stimulus by raising its target for the federal funds rate by at least 25 basis points. Meanwhile, large-scale asset purchases, which have augmented monetary stimulus and ballooned the Fed’s balance sheet from $4 trillion to nearly $9 trillion, are coming to an end in early March. This combination of policy measures suggests that in the coming months there will continue to be a considerable amount of monetary stimulus. The federal funds rate will have to keep increasing until it reaches 2-1/2 percent—the so-called neutral federal funds rate—before monetary stimulus coming from the federal funds rate has been removed. But, even then, there would still be stimulus coming from the Fed’s balance sheet, absent measures to shrink its balance sheet.

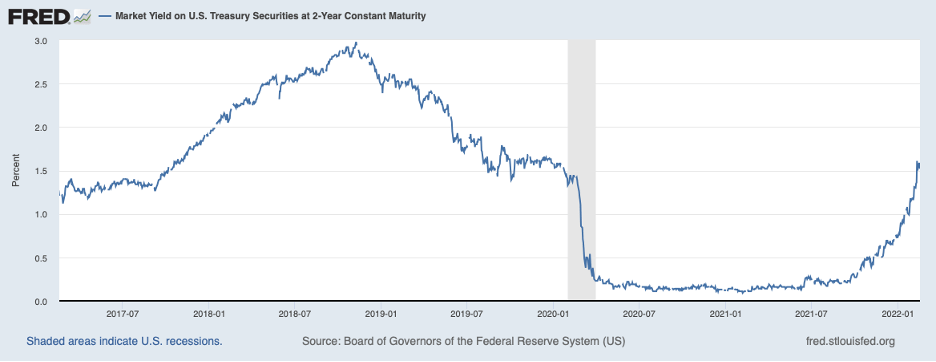

Recent news on inflation and the economy has led to a substantial rethinking of the near-term trajectory of the federal funds rate. Shown below is the yield on the two-year Treasury note—which can be thought of as an average of short-term interest rates expected by market participants over the coming two years. This rate has gone from about 25 basis points in mid-2021 to 150 basis points recently. These readings on the two-year yield are broadly consistent with the Fed raising its target for the federal funds rate to the neutral rate by the end of 2023. With the inflation outlook so highly uncertain, the Fed has been reluctant to pinpoint the path of the federal funds rate over the months ahead.

Will the amount of Fed tightening implied by the two-year Treasury yield be enough to break inflation momentum and place inflation on a path toward the Fed’s 2 percent target? Keep in mind that, under the outlook for the federal funds rate implied by the two-year Treasury yield, the federal funds rate would reach the neutral level toward the end of 2023, and policy would remain stimulative until then.

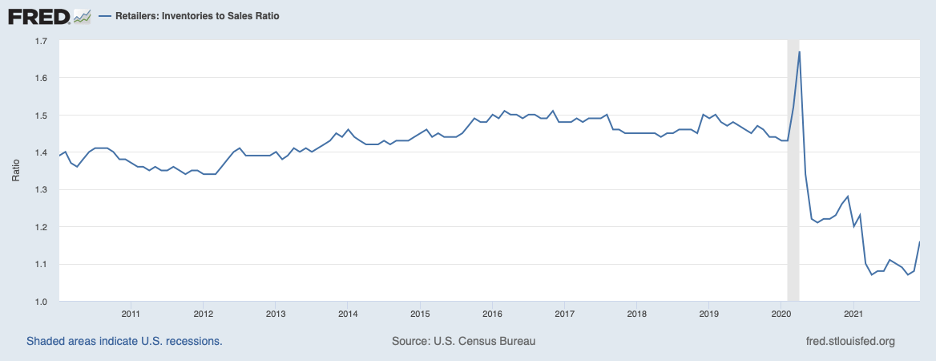

Currently, the economy can be characterized by substantial demand—coming from Fed policy and fiscal stimulus—pressing against restrained supply. The more uncertain outlook for the economy and prices is no doubt adding to caution by consumers and businesses, but there remains a considerable amount of pent-up demand for goods that will keep the economy moving forward for some time. Moreover, the depletion of inventories at the retail level appears to have come to an end, the next chart, but inventory investment has a long way to go before returning to pre-COVID levels, which reflected the now-discredited just-in-time lean inventory management strategy. Efforts by retailers to rebuild depleted stocks—including to more comfortable levels than during the pre-COVID period—will be adding to pressures on producers and prices.

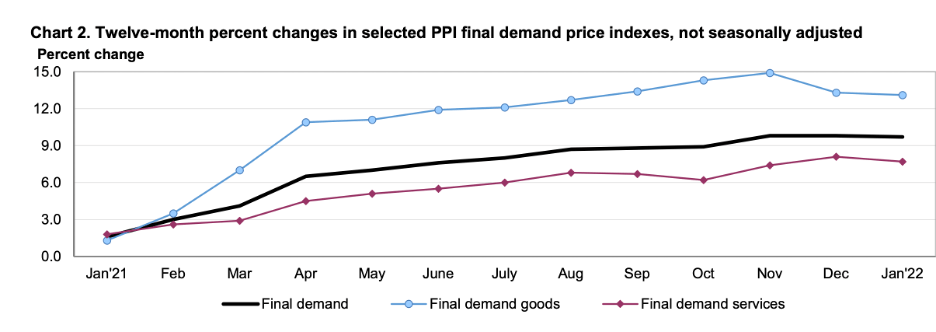

Supply is being restrained by global supply chain disruptions and a reluctance to reenter the labor force by many workers, despite the plethora of unfilled jobs. Both supply chain disruptions and the reluctance to take available jobs will ease in time. Meanwhile, they will undergird price pressures and inflation momentum. Indeed, the most recent producer price index (PPI) for January shows that prices for goods at the producer level remain in the double-digits, as seen by the blue line in the next chart, and thus large price increases continue to be in the pipeline at the consumer level. Various reports indicate that there is very little relief in sight for supply chain bottlenecks. This is especially true for the ongoing chip shortage which is affecting the availability and prices of motor vehicles. appliances, computers, and other tech products. Moreover, nearly one-half of small business owners reported in the most recent National Federation of Independent Businesses (NFIB) survey that they intend to raise selling prices in the coming months, a percentage reminiscent of the intransigent inflation period of the early 1980s.

The longer outsized price increases persist at the consumer level, the more they will become entrenched in the inflation dynamics, making it more difficult—and painful—to bring inflation under control.

These considerations suggest that it will take monetary restraint—a higher than neutral federal funds rate—to place inflation on a firm downward trajectory, given the persistence and pervasiveness of price increases and the attention to inflation coming from both consumers and producers. Keep in mind that the current setting of the federal funds rate at 0 to 25 basis points is well below neutral and highly accommodative, and, if the Fed charts a course consistent with market expectations contained in the yield on the two-year Treasury note, the policy will remain accommodative until the federal funds rate reaches neutral by the end of next year. To the degree that inflation stays entrenched through the end of next year, the federal funds rate will need to rise above the neutral rate for some time to get inflation to point decisively downward. Such sizable rate hikes would create economic slack and possibly a recession—stagflation. Buckle up: The ride might be getting wild!