Just as trees don’t grow to the sky, the rate of inflation will stop rising. The question is when?

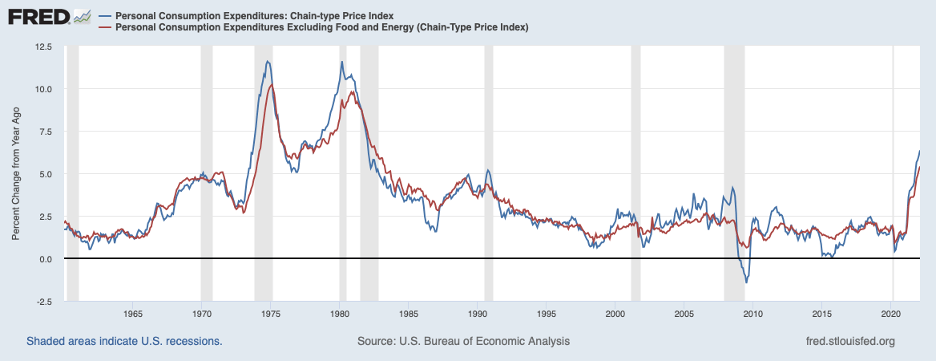

The chart below shows twelve-month percent changes in the Fed’s preferred measure of consumer price inflation—the Personal Consumption Expenditures (PCE) index. The headline index in blue rose 6.4 percent in February, the largest twelve-month increase in forty years, and the core index, which excludes prices of energy and food prices in red, rose 5.4 percent. What is worrisome about these numbers is that there has not been any slowing in monthly price changes over recent months as had been hoped by the Fed and others.

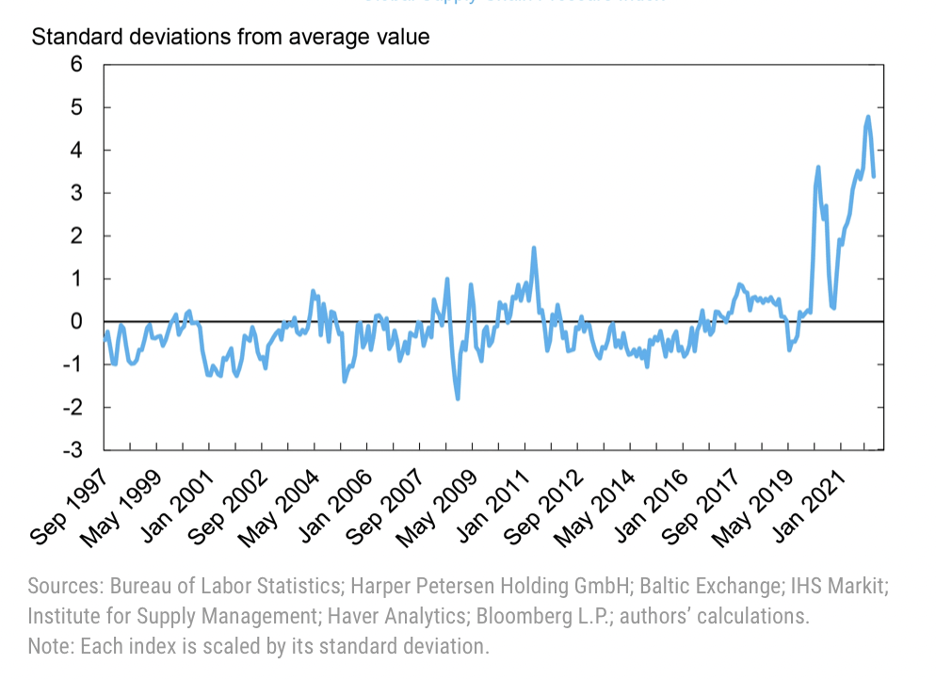

So, what will it take in the form of Fed actions to place inflation on a distinctly downward trajectory toward the Fed’s 2 percent target and when will we begin to see inflation relief? Note that a portion of the price increases over the past year reflect supply chain strains, which should ease in time. The next chart illustrates that supply chain pressures have eased only a little in recent months and remain intense.

Index of Supply Chain Pressures

Moreover, the Russian invasion of Ukraine will intensify supply chain strains, especially in food and energy. Thus, relief on the supply chain front may not be coming for a while.

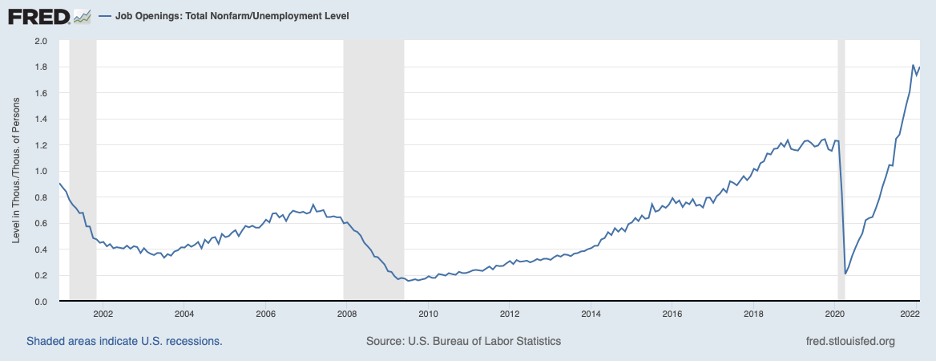

Beyond supply chain pressures, there are more persistent forces boosting inflation. The labor market continues to be hot. Employment growth over the first three months of 2022 kept up the brisk pace of 2021—about 560 thousand per month. In addition, workers who withdrew from the labor force at the onset of COVID have been slow to return, limiting growth in supply. Furthermore, as shown by the next chart, the ratio of job openings to the number of persons unemployed has continued to run around 1.8 job openings for each person who is unemployed.

This ratio is well above the pre-COVID period which—is deemed to have been a very hot job market.

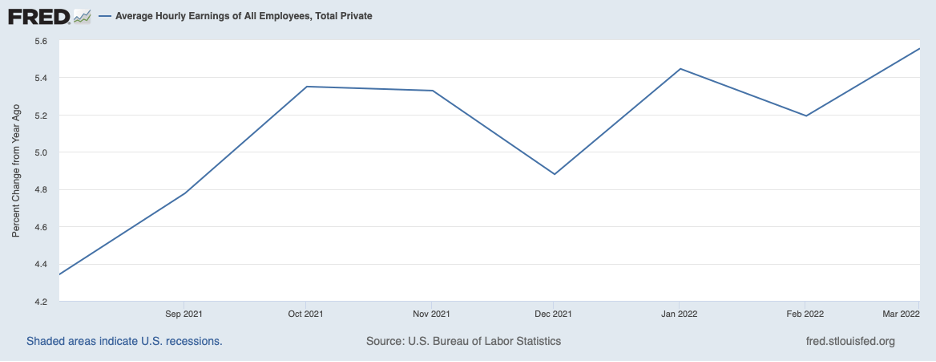

Employers are responding to labor shortages by bidding more aggressively for workers. Shown in the next chart is the twelve-month percent change in average hourly earnings.

Wage growth has been trending upward since last summer. However, this measure of wage growth is understating the actual pace because there has been disproportional growth in the number of new workers in lower-wage sectors of the economy over recent months. Thus, this disproportionate employment growth in lower-wage sectors is holding down average hourly wages for private workers overall.

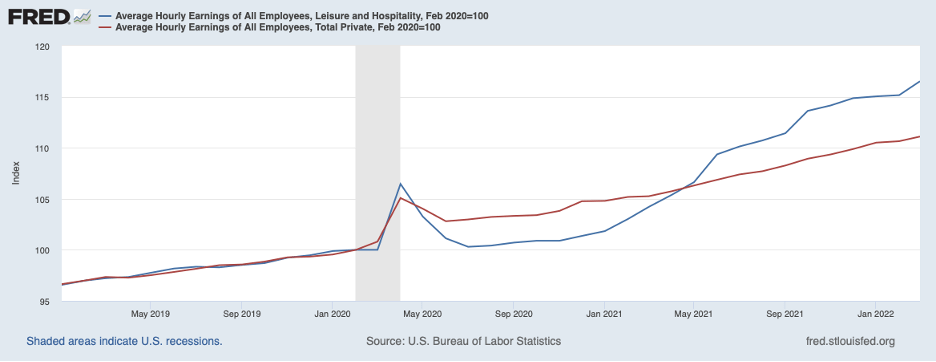

Strong growth in employment in low-wage sectors owes importantly to aggressive bidding for workers by employers, as seen in the next chart. This chart shows wages in relation to their levels at the onset of the pandemic in February 2020. The chart shows average hourly wages for all private industry workers in red (averaging roughly $31.50 per hour)—the group charted above—and those in the lower wage leisure and hospitality sector in blue (averaging roughly $19.50 per hour).

The leisure and hospitality sector was among the hardest hit by COVID in early 2020 but started coming back in early 2021. To draw employees back to the workforce, employers in leisure and hospitality stepped up wage offers. By March of this year, wages in this sector were a full 16 percent above February 2020 levels. The aggressive bidding by employers in leisure and hospitality has been only partially successful, though, as the number of workers employed in this sector is still more than 9 percent below February 2020. In the leisure and hospitality sector and elsewhere a reluctance by workers to re-enter the labor force has been adding to wage and price pressures.

The tight labor market is also adding to momentum in the inflation process and to the difficulty of getting inflation under control. Beyond the tight labor market, the dynamics of the inflation process are such that the longer high inflation runs the more entrenched it becomes. In part, entrenched inflation results from inflation expectations ratcheting higher, which to a degree becomes a self-fulfilling prophecy: When businesses and households come to expect more inflation, they post higher prices and hold out for higher wages. Beyond higher expectations of inflation, there are still other forces at work in the dynamics of high inflation that add to inflation momentum and to the degree of monetary restraint required to bring inflation down to desired levels.

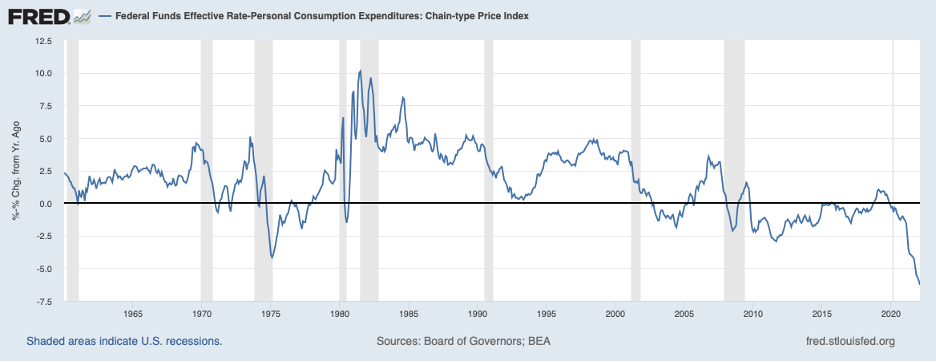

To get a better understanding of what the Fed will need to do to break the back of inflation, it is instructive to look back at the last time that inflation became highly entrenched—the end of the 1970s and early part of the 1980s. Shown in the next chart is a measure of the real federal funds rate, the nominal federal funds rate less the twelve-month PCE inflation rate. Expressed differently, the real federal funds rate is the amount by which the nominal federal funds rate exceeds the rate of inflation. Note that in the early 1980s the real interest rate fluctuated around 7-1/2 percent for a couple of years before the back of stubborn inflation was broken.

In contrast, the current real federal funds rate is well into negative territory. Simply moving the real federal funds rate to zero will require much larger increases in the nominal federal funds rate than the Fed was contemplating in mid-March. At that time, the Fed predicted that it would raise the nominal federal funds rate from zero to 1.9 percent by the end of this year and to 2.8 percent by the end of 2023. (These moves were thought to be sufficient to bring inflation down to 2.3 percent in 2023 on its way to the target of 2 percent.)

Given the momentum that inflation currently has, the real federal funds rate will need to move into positive territory if the Fed is to succeed in breaking the back of inflation. However, the level of the real federal funds likely will not need to go as in the past to bring down inflation because of long-term forces that have been depressing real interest rates. Nonetheless, the real funds rate will need to be a good bit higher than it is now. Serving to complement increases in the federal funds rate in restraining the overheated economy will be the impending run-off of assets from the Fed’s balance sheet which will add to upward pressure on other interest rates.

At this point, the Fed is sufficiently behind the curve so that a determined effort to get inflation under control will risk a hard landing—a recession. Notice in the previous chart the number of times the economy entered a recession—the gray shaded regions—after the Fed boosted real interest rates well above zero. The odds are growing that the level of the real federal funds rate that is consistent with the Fed’s current objective of disinflation will once again bring on a recession.