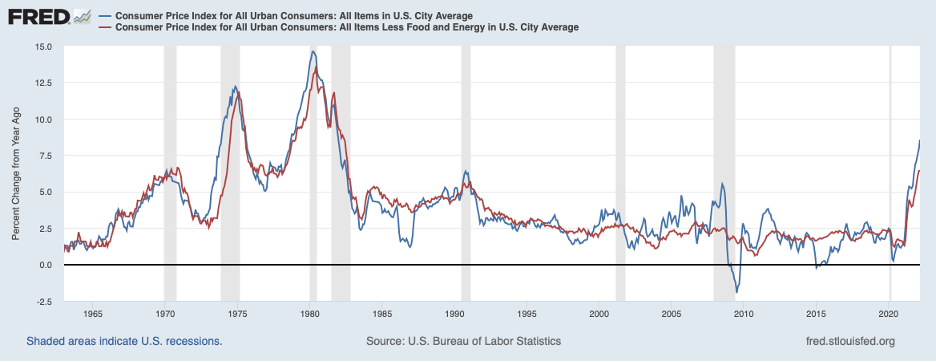

The inflation news has gotten worse. As shown by the blue line below, headline inflation rose further in March – to 8.5 percent. This increase was paced by a 32 percent surge in energy prices. Even after removing energy and food prices (so-called core inflation), prices rose 6.5 percent, the red line. Both measures of inflation reached their fastest pace in forty years. Forty years ago – in 1982 – inflation was coming down from a double-digit pace after the country had paid a heavy cost to get inflation under control. Notable about recent inflation news is the pervasiveness of price increases across the various categories of goods and services. The widespread increases in consumer prices are an indication that inflation has become more entrenched and difficult to reverse.

Portending further large price increases in the months ahead are the most recent readings on producer prices, shown in the next chart. The blue line shows that goods prices at the producer level rose nearly 16 percent over the past year while service prices at the producer level rose more than 8 percent.

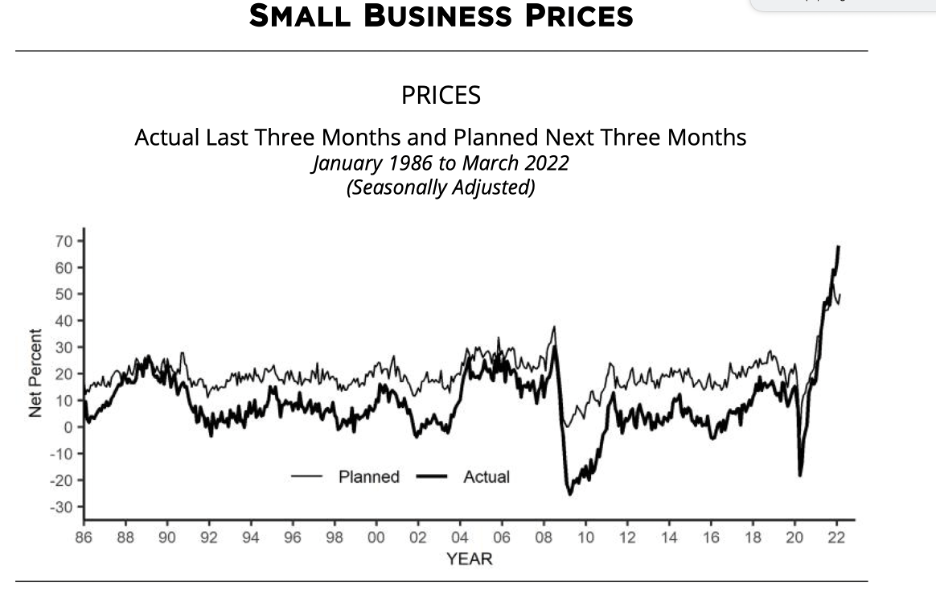

Another indicator of large forthcoming price increases is the March survey of small businesses by the National Federation of Independent Businesses (NFIB). The next chart shows that a very large share of NFIB respondents plan to raise selling prices in the coming three months. The NFIB survey also revealed that inflation was singled out by respondents as the largest problem facing small businesses. The last time inflation was isolated as the biggest problem facing small businesses was forty years ago.

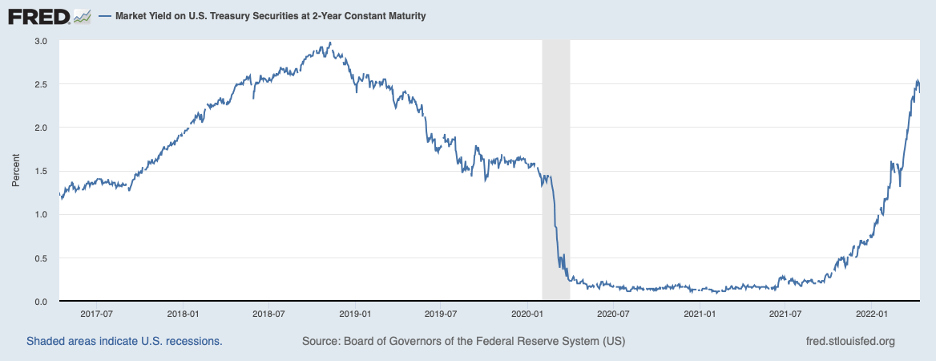

With the forces propelling inflation currently in place, it will take a fairly heavy dose of monetary medicine to turn the path for inflation downward toward the Fed’s 2 percent target. Both the Fed and financial market participants are waking up to this reality. As shown in the next chart, the yield on the two-year Treasury note (which can be thought of as the average level of the overnight federal funds rate expected over the next two years) has risen sharply over recent weeks to above its pre-pandemic level. The most recent reading on the two-year yield implies that the Fed will be raising the federal funds rate from its current level of around 0.33 percent to around 3.75 percent by the end of 2023. Treasury yields for other maturities suggest that market participants do not foresee the federal funds rate going much higher than 3.75 percent before coming down.

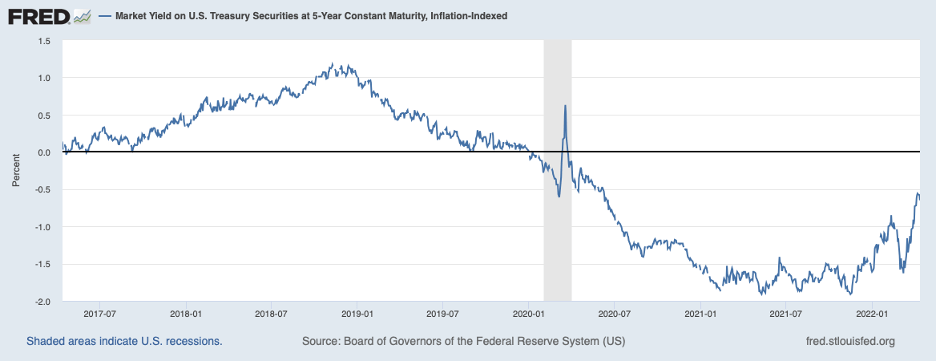

But a federal funds rate of 3.75 percent will not be high enough to break the back of inflation. The next chart shows the real interest rate on a five-year Treasury Inflation Protected Security (TIPS). The real interest rate abstracts from inflation. Note that this yield has risen in recent weeks, in keeping with the two-year yield in the chart above. But the TIPS yield remains in negative territory, implying that market participants foresee real short-term real interest rates staying negative in coming years. As noted in a recent commentary (see, Inflation: When Will it Slow?, April 2, 2022), real short-term interest rates will need to move into positive territory to place inflation on a distinctly downward trajectory. All of this points to the Fed needing to raise the federal funds rate to the vicinity of 5 percent or even higher before we will see a return to low inflation. Helping to restrain demand has been the rise in Treasury yields and other interest rates that has already taken place in anticipation of moderate increases in the Fed’s target for the federal funds rate and run-offs of assets from the Fed’s balance sheet.

Will the amount of monetary tightening required for the Fed to reach its 2 percent inflation target be enough to push the economy into recession? The longer high inflation readings persist, the greater the odds that a recession is on the horizon. Bolder action by the Fed in the months ahead will restrain the economy sooner but will also begin to take a bite out of the inflation process sooner and limit the ultimate amount of monetary medicine that will be needed to get us back to low inflation.