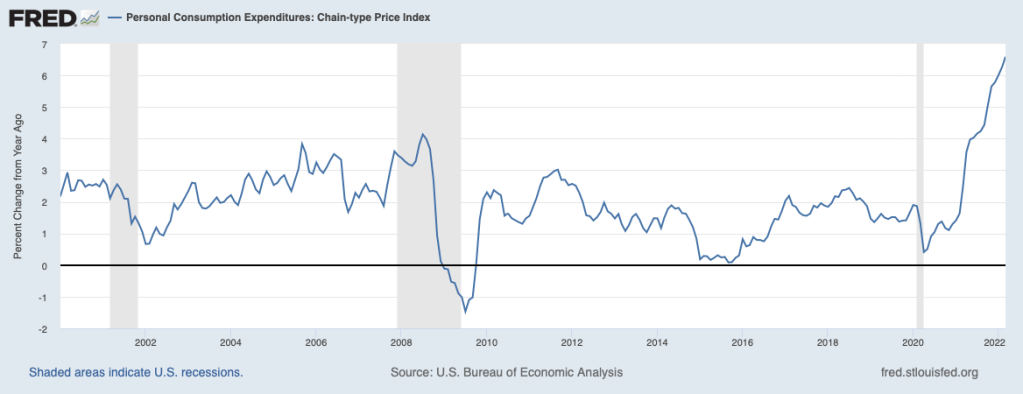

Inflation continues to dominate the news and has become firmly lodged as the number one concern faced by the public. The chart below illustrates that headline inflation continued to increase through March to a new forty-year high.

Meanwhile, output (GDP after removing the effects of inflation) declined 1-1/2 percent (at an annual rate) in the first quarter, following a nearly 7 percent increase in the previous quarter—the table below. This has led to concerns that we have entered a period of stagflation, much like the anguishing and painful era of the late 1970s and early 1980s (forty years ago).

| 2021-Q4 | 2022-Q1 | |

| Real GDP | 6.9 | -1.4 |

| Consumption | 2.5 | 2.7 |

| Durable goods | 2.5 | 4.1 |

| Nondurable goods | 0.4 | -2.5 |

| Services | 3.3 | 4.3 |

| Business fixed investment | 2.7 | 7.3 |

| Government | -2.6 | -2.7 |

Before jumping to this conclusion, let’s take a closer look at the GDP data for the first quarter. As shown in the table above, consumption growth continued in the first quarter at the moderate pace of the previous quarter, and business fixed investment accelerated. In contrast, output was again pulled down in the first quarter by a decline in government outlays, notably federal defense spending. Beyond this, a drawdown of business inventories cut nearly a percentage point off growth in output in the first quarter while a deterioration in (net) exports subtracted more than 3 percentage points from growth. Looking ahead, the drag from exports should diminish and, at some point, inventory investment will turn up and boost growth. (However, the decline in real defense spending will continue to hold down growth in real GDP.)

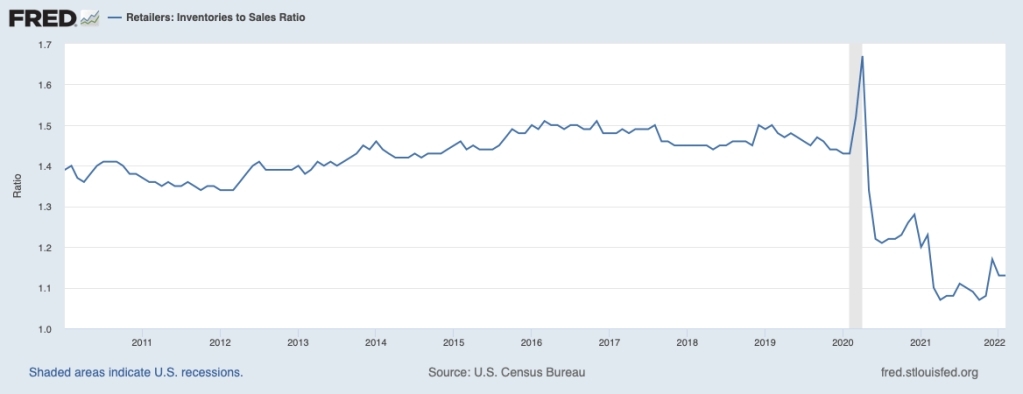

Note that consumer purchases of nondurable goods declined in the first quarter following essentially no change in the fourth quarter. To a significant degree, recent weakness in nondurable goods reflects a lack of availability, not a lack of demand. Retailers continue to struggle to replenish shelves as seen in the next chart showing the retail inventory-sales ratio.

Since mid-2021, retail businesses have made little progress in getting their stocks back in line with sales despite considerable effort.

Supply constraints are not only affecting sales of consumer goods but are also affecting prices of consumer goods as shown in the chart below. Prices for each category shown are indexed to be 100 in February 2020, the eve of the pandemic. The blue line, showing the price of nondurable goods, has risen sharply this year reflecting shortages of these items. The price of consumer durable goods, the red line, also has risen markedly since the pandemic but may be leveling off, consistent with the pickup in spending on durable goods shown in the above table. Prices of services—which grew more rapidly than prices of durable and nondurable goods before the pandemic—have risen at a slower and more steady pace than prices of goods.

The above discussion suggests that recent weakness in the economy can be attributed to supply constraints, not inadequate demand. Moreover, with unemployment extraordinarily low, owing to a huge excess demand for labor, and households enjoying solid financial positions, the outlook for consumer demand remains favorable in the period just ahead. Much the same can be said about business investment demand. Thus, remaining strength in final demand and inventory rebuilding will continue to put pressure on available resources and thereby on inflation.

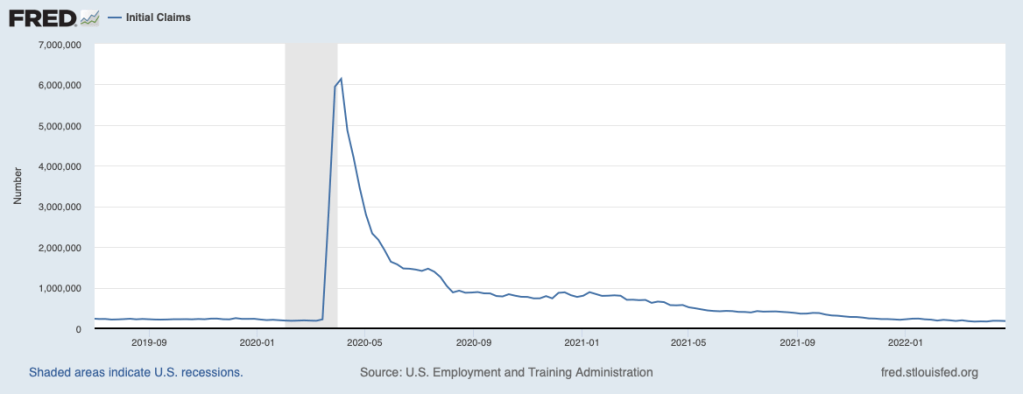

Meanwhile, the labor market remains red hot. Initial claims for unemployment insurance, the following chart, have, in recent weeks, edged below the pre-COVID period when the labor market was very hot.

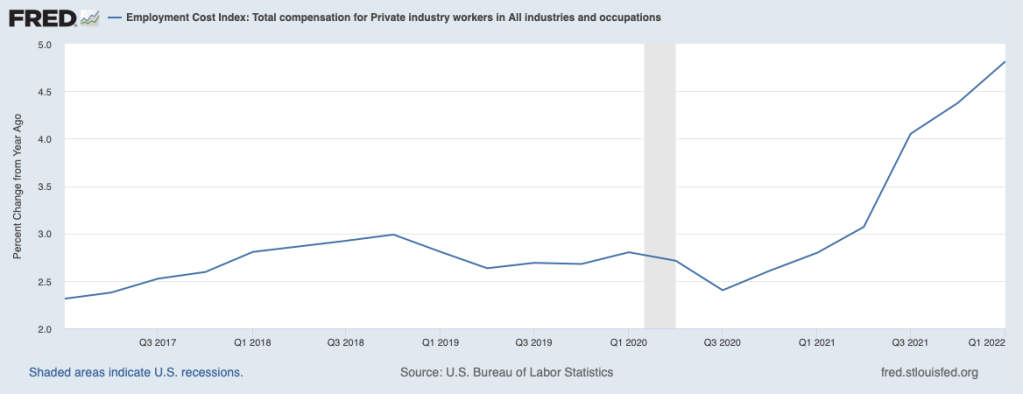

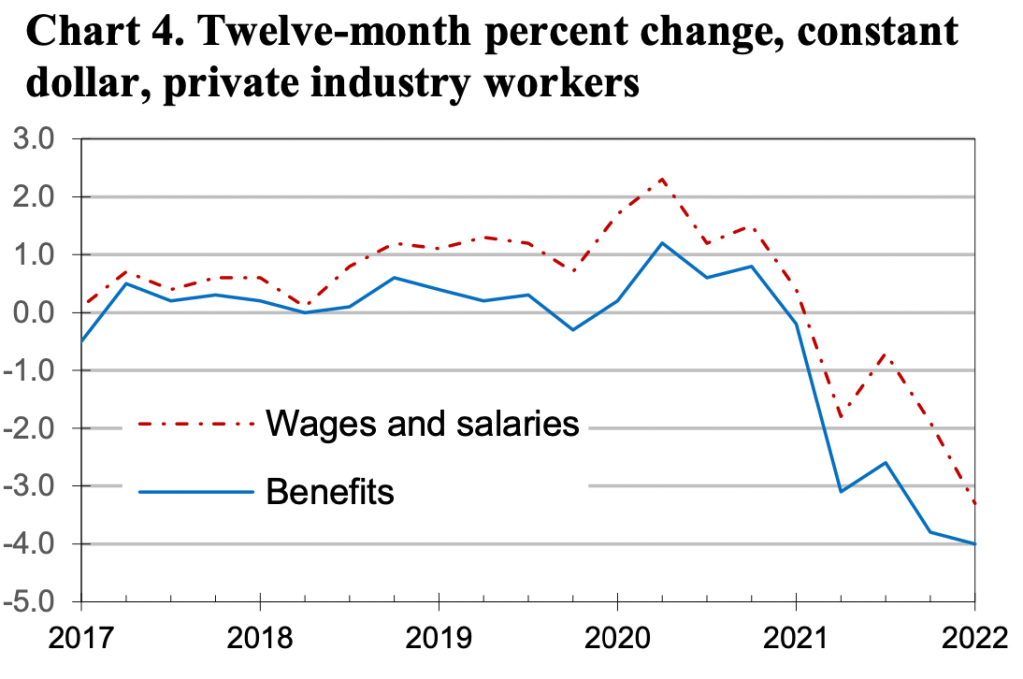

Furthermore, labor compensation has accelerated in the past two quarters, illustrated in the next chart.

Nonetheless, labor compensation has continued to lag consumer prices and real wages and real benefits, shown in the next chart, have fallen further. Looking ahead, we can expect labor costs to continue to accelerate, adding to upward pressure on consumer prices.

An easing of supply chain bottlenecks, still some time away, will act to lower inflation. However, momentum in the inflation process has been gaining traction, and the Fed must take very aggressive measures to get inflation under control and on a clear path to its 2 percent target. Based on recent readings in the Treasury securities market, market participants envision the federal funds rate rising to 4 percent or a little above by the end of 2023 before leveling off. As noted in previous commentaries, this degree of monetary tightening will not be nearly sufficient for the 2 percent target to be in sight over the next few years.

Among the sectors affected most by prospective Fed tightening will be the housing sector. The following chart illustrates that mortgage interest rates, the red line, already have been rising sharply in 2022, even faster than Treasury benchmark rates.

And the rise in mortgage rates is affecting pending sales of existing homes, shown in the following table. The cooling of existing home sales has become more evident this year.

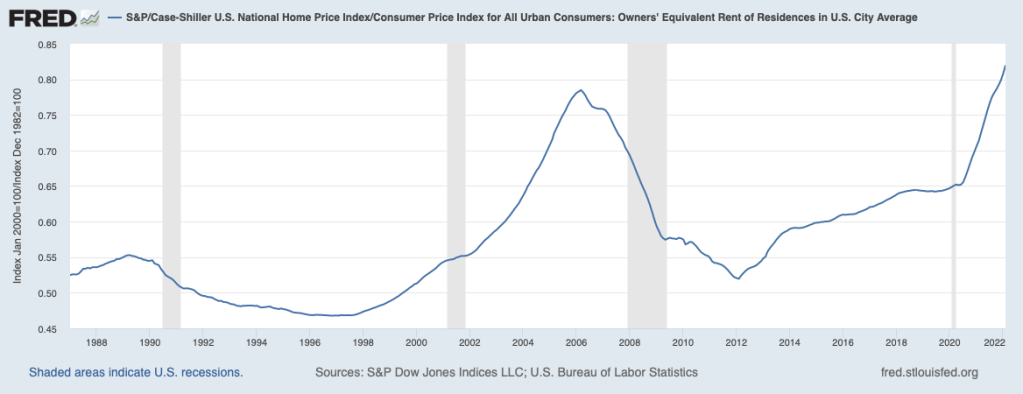

The housing sector will be taking the brunt of forthcoming increases in interest rates. Shown in the next chart is the ratio of home prices to rents through February of 2022. The price-to-rent ratio has continued to increase over recent months as home prices have risen faster than rents. Indeed, this ratio has recently risen above its peak in 2006, before the bursting of the housing bubble that precipitated the financial crisis of 2008 and 2009.

To some degree, the return of this ratio to a more normal level will occur through a pickup in rents. However, some of the correction of this ratio will take place through home price declines, especially in response to the forthcoming rise in mortgage rates. The road ahead for the housing sector increasingly is looking like it will be rocky.

The prospective downturn in the housing sector will not be sufficient to restrain demand enough to break the back of inflation. Business investment and consumer spending on goods and services will also need to be curbed. In light of the above considerations, a soft landing—regaining control of inflation while avoiding a recession—seems increasingly unlikely. The sooner the Fed puts its shoulder to the wheel, the less will be the dislocation.