The Federal Reserve (Fed) in recent statements has been emphasizing the need to bring inflation down. The Fed has said that it will continue to raise its target for the policy interest rate—the overnight federal funds rate—until it restores price stability. The Fed has not explicitly acknowledged that it is behind the curve in achieving its goal for inflation, but its recent action to boost the federal funds target 50 basis points (100 basis points equals one percentage point)—instead of the standard 25 basis points—is a tacit admission of the need to catch up quickly.

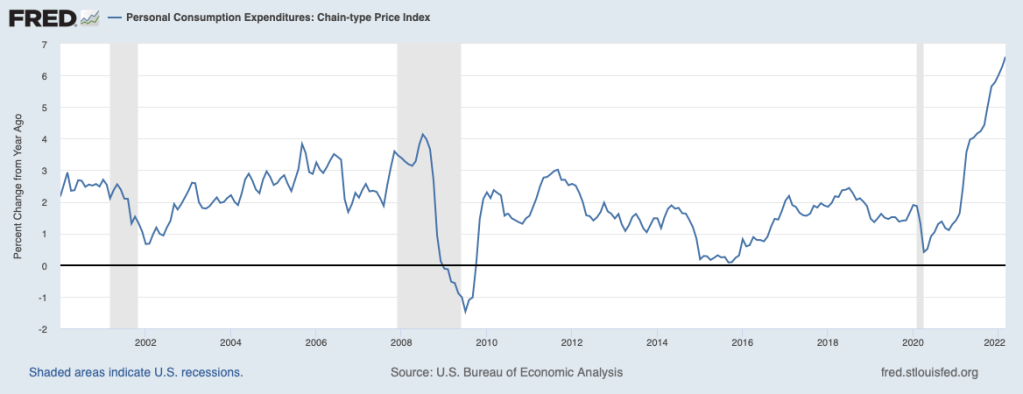

The statutory goals of the Fed’s monetary policy are maximum employment and stable prices—the so-called dual mandate. With the unemployment rate at historic lows, the maximum employment goal has been achieved—indeed, overachieved—even though employment remains below pre-pandemic levels. Regarding the price stability goal, the Fed for the past decade has stated that it regards price stability to be a 2 percent annual increase in consumer prices based on its preferred measure, the Personal Consumption Expenditures (PCE) index. As shown in the chart below, inflation according to the PCE index has soared to 6.6 percent over the past year and continues to be pointed upward. Once inflation gets into this area, it disturbs the role that ordinary prices play in our economy in guiding resources to where they make their greatest contribution. Another consequence of high inflation is that it has distributional effects as those at the lower end of the income scale typically experience more of an erosion of their purchasing power than others.

The surge in inflation owes to an excess of demand over supply. Demand has been fueled by massive amounts of fiscal stimulus—aimed at providing relief to households during the pandemic and rebuilding infrastructure—and monetary stimulus aimed primarily at boosting interest-sensitive spending. At the onset of the pandemic, the Fed lowered its target for the federal funds rate to the lower bound of zero to 25 basis points and embarked on a program of asset purchases that accumulated to nearly $4 trillion over two years. At the same time, COVID immediately curbed supply and has been followed by ongoing supply-chain disruptions, exacerbated more recently by supply disruptions coming from the Russian invasion of Ukraine and lockdowns in China. In addition to demand-supply imbalances, once inflation gets underway, as it has in the past year, momentum builds that is hard to break. The longer high inflation persists, the greater that momentum.

The two increases in the target for the federal funds that the Fed has made since mid-March—amounting to 75 basis points—are only the opening salvo. But how much higher will the federal funds rate go? The Fed and many observers like to discuss the stance of monetary policy in the context of the neutral federal funds rate—the level of the federal funds rate at which monetary policy is neither expansionary nor contractionary. The neutral federal funds rate can be thought of as the sum of the neutral real federal funds rate (the federal funds rate abstracting from inflation) and the underlying rate of inflation. The Fed views the neutral federal funds rate to be around 2-1/2 percent when the underlying rate of inflation matches its goal of 2 percent. However, the underlying rate of inflation currently is well above 2 percent, but how much higher is hard to determine with any reasonable precision.

Furthermore, inflation is becoming increasingly entrenched, and breaking its back will require that the federal funds rate reach a level well above neutral. Based on these considerations, the Fed’s projections in March that the federal funds rate would reach a peak of 2-3/4 percent by the end of next year seems highly unrealistic. Even current expectations of market participants, which have risen markedly over recent weeks, have not caught up with the reality of what it will take to bend the trajectory for inflation in a downward direction. Current Treasury yields imply that market participants see the federal funds rate being raised to 3 percent at the end of this year and to around 4-1/4 percent at the end of 2023 before leveling off. The above considerations imply that the federal funds rate will need to be increased to well above the 4-1/4 percent rate expected by the market if the Fed is truly serious about achieving the 2 percent inflation target.

The Fed will try to avoid surprising markets by signaling rate moves ahead of taking action. Bitter experience from past episodes of catching markets by surprise, especially when the Fed is in a tightening posture, has convinced the Fed that laying the groundwork for rate hikes is important for limiting market disruptions. Moreover, markets will need to digest run-offs of assets from the Fed’s portfolio, which will increase the amount of assets that private investors will be absorbing. These balance sheet runoffs will place added upward pressure on interest rates and assist in the Fed’s efforts to restrain demand to curb inflation. Helping also to bring inflation down will be an easing of supply-chain disruptions. But, at this point, such easing will not be enough to get inflation under control.

Recently, Fed Chair Powell has invoked the name of Paul Volcker who persevered with a highly restrictive monetary policy to get the last major bout of inflation under control. This invocation was no doubt intended to suggest that the current Fed has comparable resolve to the Volcker Fed to wring inflation out of the economy. Chair Powell’s comments are intended to convince workers, businesses, and financial market participants that the inflation situation is being brought under control and thereby hold down increases in the public’s expectations of inflation. Higher expectations of inflation tend to become self-fulfilling as workers and businesses become more proactive in raising prices and seeking higher wages to limit the damage they face from inflation. Higher inflation expectations add to the momentum in the inflation process and the Fed is now attempting to check this momentum before it further complicates its disinflation task. If the Fed is successful in convincing the public that inflation will be brought back to a slow pace, the number of forthcoming increases in interest rates will be tempered. However, if this effort proves unsuccessful—as did for Volcker—then interest rates will need to rise considerably more to bring the expansion to a halt and produce enough slack in resource markets to cool inflation—a recession. And, the greater the underlying strength of consumer and business demand, the higher will interest rates have to go to bring on this slack.

It is worth noting that it took the Volcker Fed three years of restrictive policy—and the most severe recession of the postwar period to that time—before it became clear that inflation was licked and monetary policy could ease off. During that time, the White House stayed out of the fray, and that hands-off posture limited political pressure on the Fed to reverse course. This time around, it likely will not require three years of restrictive monetary policy (the federal funds rate above its neutral level) to break the back of inflation. However, the adverse effects on the economy of prospective Fed restraint are likely to begin being felt in the latter part of 2023 and in 2024 which could well lead to mounting political pressure on the Fed to throw in the towel prematurely. Clearly, the Fed is about to be tested, as it has not in forty years, in its resolve to achieve the price stability mandate.