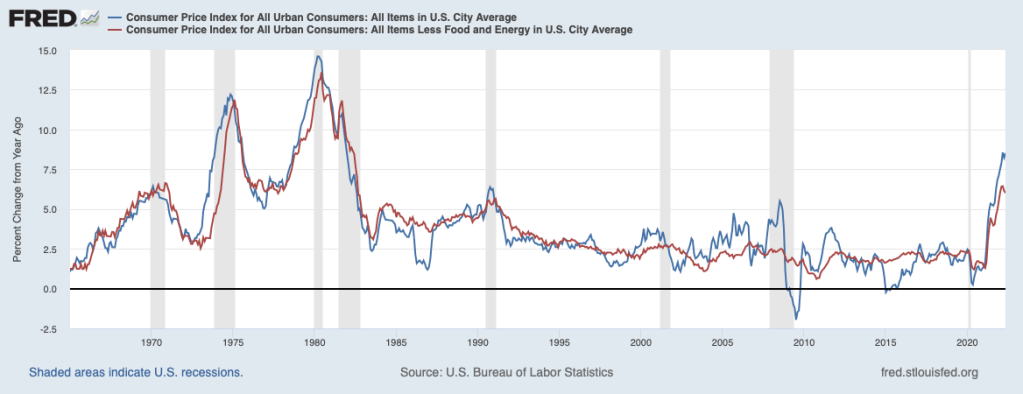

If there was any doubt about inflation becoming entrenched, the CPI for May should have dispelled that doubt. Shown below is the twelve-month percent change in the headline CPI and the core CPI which removes food and energy prices. Headline prices rose 8.6 percent and core prices rose 6 percent, the difference reflecting the recent surge in both energy and food prices. Moreover, there is little evidence of a slowing over recent months. Indeed, over the most recent three months, headline inflation strengthened to a 10 percent annual pace while core inflation stayed at 6 percent. Furthermore, large price increases have become widespread across the various types of goods and services that consumers buy, a good indication that inflation has developed considerable momentum.

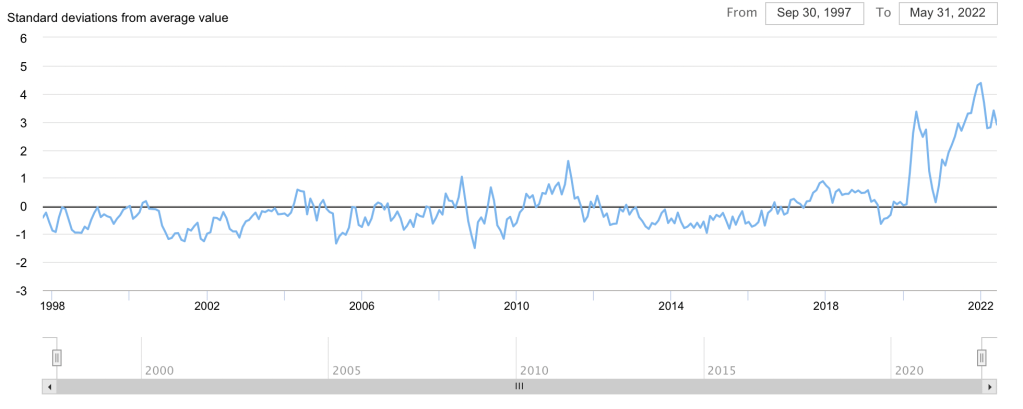

Adding to this momentum have been supply-chain disruptions which have curbed the supply of many goods. The next chart shows that supply-chain pressures have eased a little in recent months, but remain intense compared to the past decade. This index suggests that we are unlikely to get much relief from an unwinding of supply chain disruptions in the months ahead. Moreover, even once supply-chain pressures return to more normal levels, inflation momentum likely will persist.

Global Supply Chain Pressure Index

All now agree that the Fed has fallen far behind the curve on inflation and has a lot of catching up to do. This year, the Fed has raised its target for the federal funds rate from 0 (actually, a range from 0 to 25) basis points to 75 basis points (100 basis points is one percentage point) and has signaled clearly that a number of additional rate hikes are in store. Markets are expecting that the Fed’s target will end the year around 3-1/4 percent or so and top out in the 4.50 percent area in early 2024 before easing off. Will this be enough?

Previous experience has shown that once inflation has persisted this long, it develops a momentum that is hard to break. Businesses transition from viewing price changes as indicators of movements in relative scarcity to indicators of broader-based inflation, and these businesses change their pricing strategy to raise their prices frequently to protect against anticipated losses of the purchasing power of their dollar receipts. Similarly, workers seek increases in compensation that cover the anticipated loss of purchasing power that they face. Worker compensation has picked up this year, but compensation has lagged the pickup in prices. For most workers, their compensation will in time adjust upward to the higher rate of inflation, but those in lower-income brackets typically fall behind other workers. Similarly, prices of stocks and other assets will rise in line with underlying inflation after a period of adjustment to higher underlying inflation.

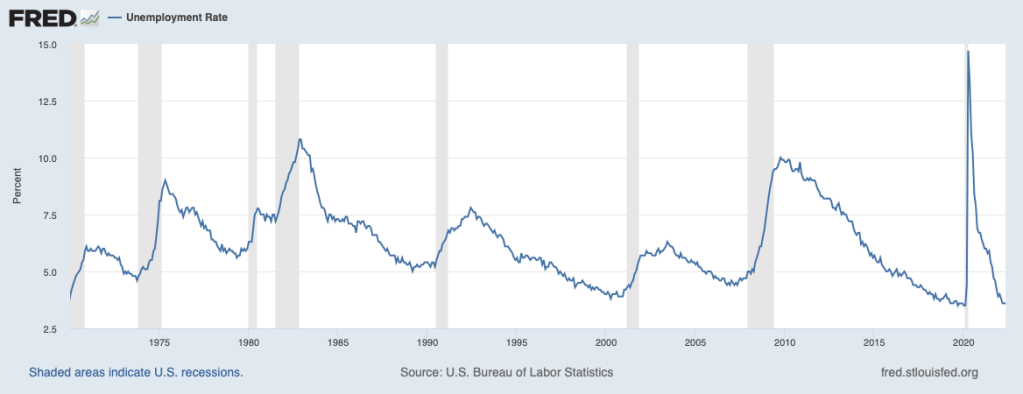

The higher and more deeply inflation is entrenched, the more monetary tightening by the Fed will be needed to bring inflation under control. Because of the inflation momentum that has developed, the tightening must be sufficient to create a degree of economic slack—caused by a shortfall of demand in relation to supply—for inflation to slow. A common measure of slack is the unemployment rate, shown next. The unemployment rate in recent months has been touching historical lows, below levels that are sustainable and deemed consistent with full employment. The May unemployment rate of 3.6 percent is roughly ½ to 1-1/2 percentage points below the level thought to be aligned with maximum sustainable employment. The current tight labor market means that demand has to slow a good bit to bring aggregate demand below aggregate supply and open up a sufficient degree of slack to curb inflation.

To bring demand below supply will require that the federal funds rate rises above underlying inflation. Determining underlying inflation is always difficult, but it is especially difficult under current circumstances.

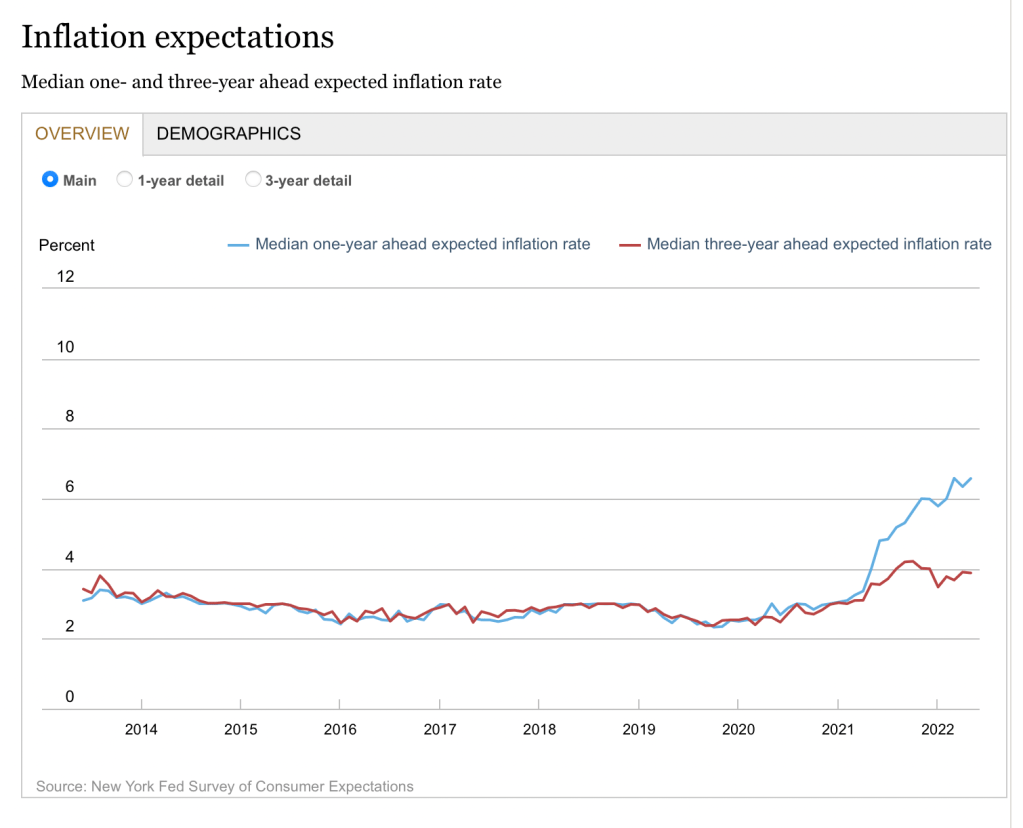

Nonetheless, underlying inflation likely is at least 5 percent, consistent with readings of consumer expectations of inflation from the New York Fed Survey of Consumer Expectations, shown above. This reasoning implies that the target for the federal funds rate will need to rise to at least the area of 6 percent to create the amount of slack that will break the back of current inflation—well above that being contemplated by the Fed and market participants.

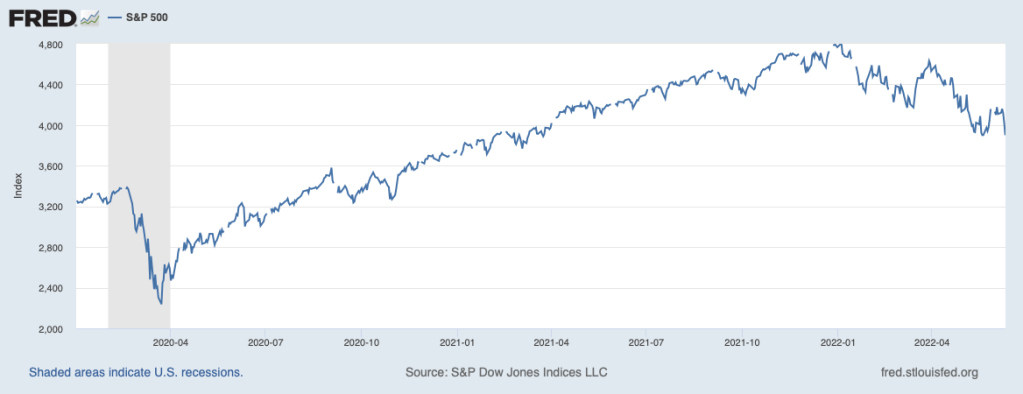

The recent and prospective increases in interest rates are having an impact on markets which is beginning to restrain demand. Reports are mounting that the sting of higher mortgage rates is cooling the previously torrid housing market. Moreover, stock prices, shown below for the S&P 500, have fallen roughly 20 percent from their peak at the beginning of this year. This decline translates into a loss of $8 trillion of household wealth, which is acting to restrain household consumption spending, and this loss of wealth will trim about 1-1/4 percent from growth in demand over the coming quarters. But that likely will not be enough.

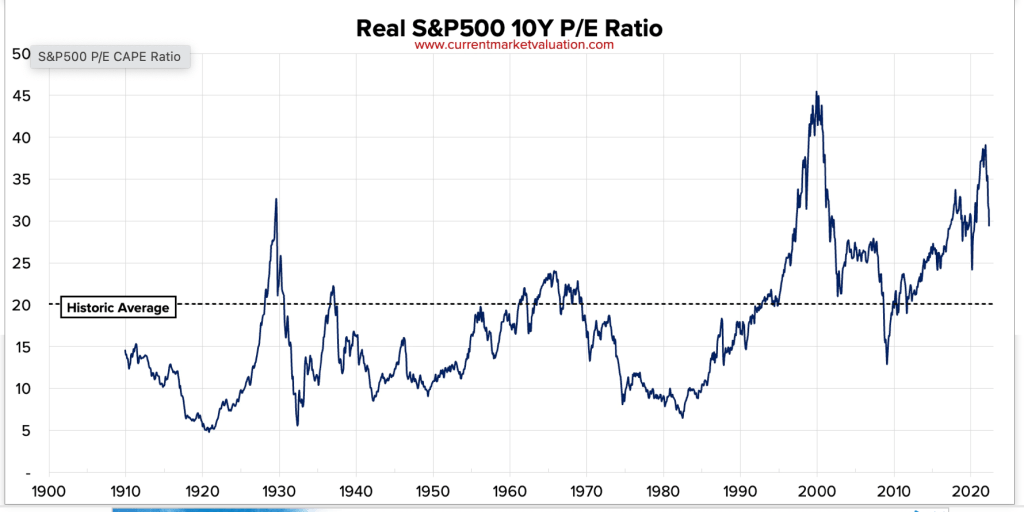

Moreover, the following chart, showing equity prices per dollar of earnings (adjusted for the cyclical variations), illustrates that the stock market sell-off has brought the P-E ratio closer to historical norms. But the P-E ratio is still high by historical standards implying that there is scope for further share price declines, especially as interest rates march even higher than currently expected and markets stay volatile. The P-E will move lower as market participants come to realize that the trajectory for the federal funds rate will have to be steeper than currently believed if the Fed is serious about its 2 percent inflation target. Forthcoming increases in interest rates will also act to restrain spending in the housing sector and other interest-rate-sensitive sectors.

Putting the pieces together, inflation has become so entrenched that it is going to take strong medicine by the Fed to get inflation pointed toward the Fed’s 2 percent target. This entrenched inflation means that interest rates will be heading for their highest levels in decades and that home and equity prices will be moving lower for a while. A negative shock to the economy, which cannot be ruled out, would limit forthcoming increases in interest rates. It all adds up to a recession in the next year or so. Hopefully, the downturn will not be protracted.

Get ready for some even harder times.