On June 15, the Fed stepped up its anti-inflation effort, raising the target for the federal funds by 75 basis points for the first time in nearly three decades. Larger than expected increases in consumer prices and higher expectations of inflation by consumers were given as reasons for the unusual policy action by the Fed. Fed Chair Jerome Powell noted that failing to restore price stability is not an option and that monetary policy needs to be restrictive to bring down inflation.

Inflation is highly corrosive in various ways. In principle, all prices—including stock and home prices—and wages will, in time, rise in line with the higher rate of inflation; similarly, interest rates will increase by the amount of additional inflation. However, this adjustment takes time, and many experience losses in the meantime. Savers who lent funds at the very low interest rates of recent years are finding that their interest earnings don’t come close to covering the more rapid increase in the prices that they have to pay for things. Also, to date, labor compensation has picked up, but not to the same extent as inflation and thus real wages have deteriorated. In addition, many living on pensions do not have cost-of-living adjustments or have incomplete adjustments and, with higher inflation, are experiencing a steady erosion of the purchasing power of those pensions. The evidence from past inflationary periods indicates that those in lower-income groups do not fare as well as others as the economy adjusts to higher inflation. In other words, inflation hits the most vulnerable hardest—a capricious redistribution of income and wealth.

In addition, inflation blunts the role of prices and wages as indicators of scarcity and as guides to movements in resources. In large, complex market-based economies such as ours, prices play a pivotal role in directing resources to their most highly valued uses. (See Chapter 3 of my book, Capitalism Versus Socialism: What Does the Bible Have to Say? (Kindle, 2020). Prices act to coordinate economic activity in a way that achieves high levels of output. But with inflation, businesses and workers have difficulty discerning whether price and wage changes call for a behavior change, as they do normally, or whether they instead represent broader inflation pressures. Furthermore, inflation leads businesses and workers to redirect precious time and effort to focus on protecting themselves against losses of purchasing power. Inflation also discourages business investment and leads to a redirection of investment from worthwhile longer-term investment toward shorter-term investment because returns on investment become more uncertain the longer the length of the investment. Inflation further reduces returns on investment because depreciation allowances for tax purposes do not grow with replacement costs (which grow with inflation). The end result is that inflation causes a loss in output and a reduction in our standard of living. In other words, there are good reasons why people have become alarmed by the acceleration of prices over the past year and a half.

The current bout of inflation can be traced back to the onset of the COVID pandemic in early 2020. As the pandemic took hold, both demand and supply collapsed and many prices came under downward pressure. However, demand recovered quickly, aided by massive fiscal stimulus programs and very aggressive easing of Fed monetary policy, while supply came back more slowly. Holding back supply has been supply chain disruptions and a reluctance on the part of many workers to return to the labor force in the wake of the pandemic. Excess demand began to show through in early 2021 (compounded by still more fiscal stimulus from the American Rescue Plan) and consumer prices began accelerating. More recently, the Russian invasion of Ukraine has led to additional upward pressure on energy and food prices and lockdowns in China aggravated supply-chain disruptions. With persistent acceleration in prices, inflation expectations have been moving higher.

In its updated forecast, the Fed foresees growth in real GDP slowing from 5.5 percent in 2021 to 1.7 percent this year and next year, and inflation slowing from 5.5 percent in 2021 to 5.2 percent this year, and 2.6 percent in 2023 on its way to the Fed’s target of 2 percent. Achieving the Fed’s forecast of 5.2 percent inflation for 2021 will require a substantial slowing of price increases over the final seven months of the year from the pace of the first five months—raising doubts about the plausibility of this component of the forecast. Meanwhile, the Fed foresees the unemployment rate rising only 0.5 percent from the current level of 3.6 percent to a level just 0.1 percent above the level thought by the Fed to be consistent with maximum employment. This forecast would have to be characterized as a highly desirable outcome—a soft landing.

Is the Fed’s forecast plausible? Economists generally agree that there are two primary factors that drive up inflation: strains on resources and higher expectations of inflation. Strains on resources result from aggregate demand exceeding aggregate supply—a so-called positive output gap. When this occurs, the unemployment rate will be below the level consistent with maximum sustainable employment. Changes in inflation expectations tend to pass through to actual inflation one-for-one. The process described here is symmetric: Inflation will fall if there is a negative output gap—demand falls short of supply—or if there is a decline in inflation expectations. To achieve the Fed’s goal of 2 percent inflation on a sustained basis, inflation expectations need to be anchored around 2 percent.

In the current situation, inflation is being driven by both an overheated economy—demand exceeding supply—and by rising inflation expectations. The positive output gap is accompanied by an unemployment rate of 3.6 percent, below the rate associated with maximum employment. As noted, the unemployment rate associated with maximum employment is estimated by the Fed to be around 4 percent, but some view other measures of strains in the labor market to suggest that it is higher—by as much as a percentage point or more.

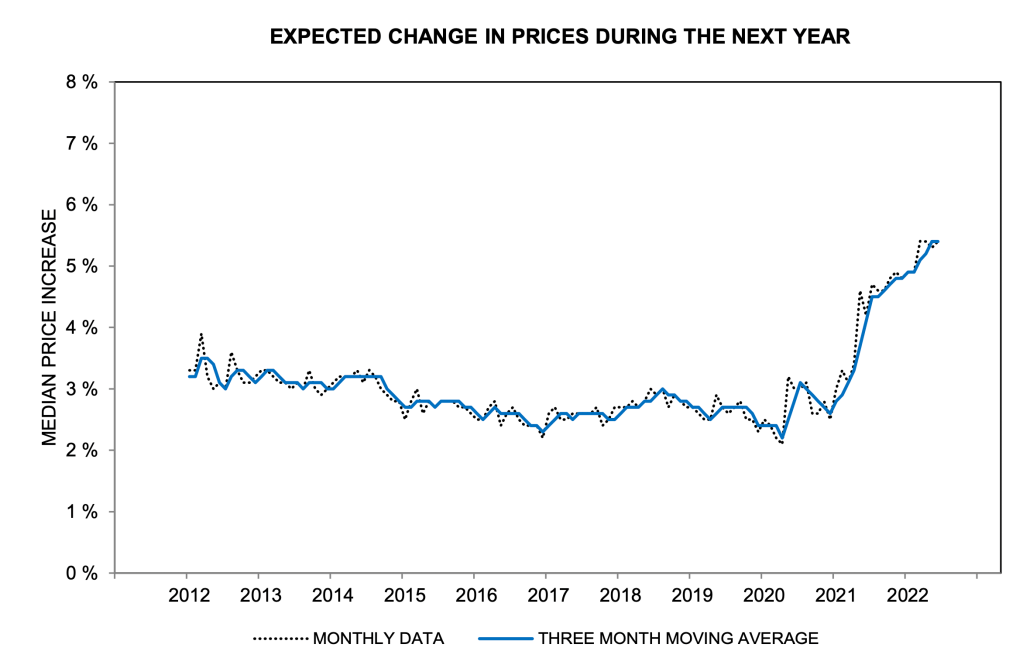

Also, inflation expectations have moved outside the range consistent with the Fed’s 2 percent target. The Michigan Survey of Consumers produces a closely watched measure of consumer expectations of inflation. The Michigan Survey asks consumers for their prediction of price increases over the next year and over the next five years. The two charts below show year ahead and five-year ahead expectations of inflation. (It is well known that consumers routinely overpredict price increases and this needs to be taken into account in reading the charts.) The first chart shows that year-ahead inflation expectations turned up briskly in early 2021 and have climbed roughly 2-1/2 percentage points above the level that characterized the period before 2021 when inflation was under control.

Longer-term expectations in the next chart have also moved higher over this period but to a lesser degree. Recent readings are roughly ½ percentage points above the level that characterized the period before 2021. The Fed tends to focus on longer-term expectations of inflation as the more important driver of inflation and evidently was concerned about the upturn in the most recent survey (the dotted black line). While longer-term expectations of inflation play an important role in the inflation process, one should not overlook the information contained in shorter-term measures, which have moved up most sharply recently.

In light of the above considerations, what will it take to bring down inflation to the Fed’s 2 percent goal? Clearly, the upward movement in inflation expectations over the past year-and-a-half will need to be reversed, and the positive output gap will need to be closed. However, at this point inflation expectations likely have become sticky and are unlikely to move much lower solely based on anti-inflation rhetoric by Fed officials. People will need to see inflation moving lower on a sustained basis before they come to expect lower inflation. Thus, to get inflation to move lower, the output gap must not only be closed but a negative output gap must be created (the unemployment rate must increase above the rate associated with sustainable maximum employment) to turn inflation downward.

Creating a negative output gap will require that the Fed move the federal funds rate above the underlying rate of inflation. Right now, the federal funds rate of 150 (to 175) basis points is well below the underlying inflation rate, and the Fed is providing substantial stimulus to an overheated economy. Moreover, the Fed sees its optimistic forecast being achieved by the federal funds rate rising to 3.4 percent by the end of this year (well below its forecast of inflation for this year) and 3.8 percent by the end of 2023 (a little more than a percentage point above its implausibly low forecast of inflation for 2023). Recent readings imply that financial market participants have priced in only a little higher federal funds rate over this period than the Fed.

What is missing from this assessment is that once inflation gets to where it has gotten now, it develops a momentum that is hard to break. There are dynamics to the inflation process that are not captured by the standard framework presented above and are not fully understood by economists. In other words, not only are inflation expectations stubborn to be reversed but there is an underlying dynamic that adds to inflation momentum. In such circumstances, it takes even more stringent monetary policy to break the back of inflation—that is, a still higher level of the federal funds rate. This reasoning implies that the federal funds rate will need to go well above 3.8 percent to create a negative output gap sufficiently large to break the back of inflation. The stronger is growth in aggregate demand and the more that inflation has become entrenched, the higher will the federal funds rate have to go.

What are the implications of a recession? The above discussion suggests that restoring price stability will require demand to be restrained sufficiently through higher interest rates to fall short of supply—unemployment to rise a good bit from the current level. This means that interest rates will need to rise well above those forecasted by the Fed if the Fed is going to be successful in restoring price stability. In other words, a recession likely is on the horizon. Even though output is likely to be stagnant over the first half of this year, there are good reasons to expect business and consumer spending to pick up in the coming quarters and the recession to come later. It is more likely that if the Fed takes the action required to subdue inflation, signs of the downturn will become clear in the latter part of 2023. Note that in this scenario the recession develops a year ahead of the general election in 2024 which will throw the Fed into the middle of a political lion’s den.