Worries about a looming recession have been ebbing and flowing over recent weeks. Real gross domestic product (GDP) contracted 1-1/2 percent at an annual rate in the first quarter of this year, and estimates for the second quarter suggest another decline. One widely followed estimate comes from the Federal Reserve Bank of Atlanta and utilizes a statistical model that relies on data for the quarter to date to produce an estimate of real GDP. This model suggests that output contracted in the second quarter by a similar amount as in the first quarter.

A popular definition of a recession is two consecutive quarters of declines in real GDP. By that definition, we are very close to slipping into a recession in 2022. However, the arbiter of business cycles, the Business Cycle Dating Committee of the National Bureau of Economic Research (NBER), has yet to weigh in on the matter. Moreover, that committee will be looking for the widespread evidence of weakness throughout the economy. To date, the labor market and some other sectors appear to still have considerable strength. Indeed, the labor report for June revealed that the private sector added a solid 381 thousand workers last month, pushing private-sector employment above pre-pandemic levels, and unemployment remained at a historically low 3.6 percent rate. Nonetheless, the labor force participation rate stayed about 1-1/4 percentage points below its pre-COVID level, constraining the supply of labor and, along with it, the supply of goods and services.

A recession will be caused by a sustained downturn in aggregate demand which does not seem to be in the cards, despite a souring of consumer attitudes recently. Shown below is the consumer sentiment index from the Michigan Survey of Consumers. The index dropped sharply in June to one of the lowest levels on record. Typically, declines of this sort presage a downturn in consumer spending which accounts for about two-thirds of aggregate spending. Moreover, the recent plunge in sentiment comes on the heels of a softening in consumer spending in April and May.

The table below shows that overall PCE spending ticked down over those two months, dragged down by spending on both durable and nondurable goods. Those spending declines on durable and nondurable goods owed, at least in part, to restraints on supply (discussed more fully below). Nonetheless, retail sales data for June suggest that consumer spending on goods recovered somewhat last month.

Growth in Real Personal Consumption Expenditures (PCE)

(Percent change at a monthly rate)

| 2021 | 2022 Q1 | 2022 April-May | |

| Total PCE | 0.7 | 0.5 | -0.1 |

| Durable goods | 1.5 | 2.0 | -0.7 |

| Nondurable goods | 0.8 | 0.2 | -1.0 |

| Services | 0.5 | 0.4 | 0.3 |

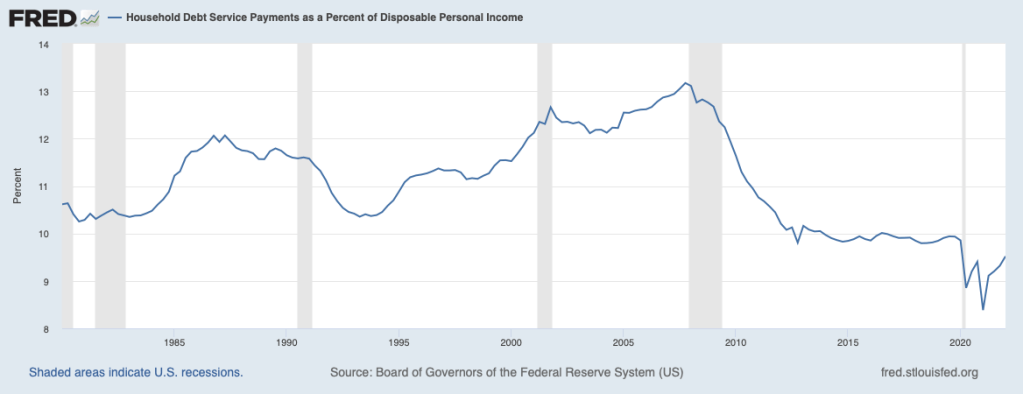

Despite recent weakness, fundamentals point to a resumption in growth in consumer spending. This is because employment remains plentiful, household wealth positions are still high despite lower stock prices, and household debt servicing has not been much of a restraint. The chart below shows that the portion of household disposable income devoted to debt service remains very low by historical standards, implying that households still have considerable borrowing capacity.

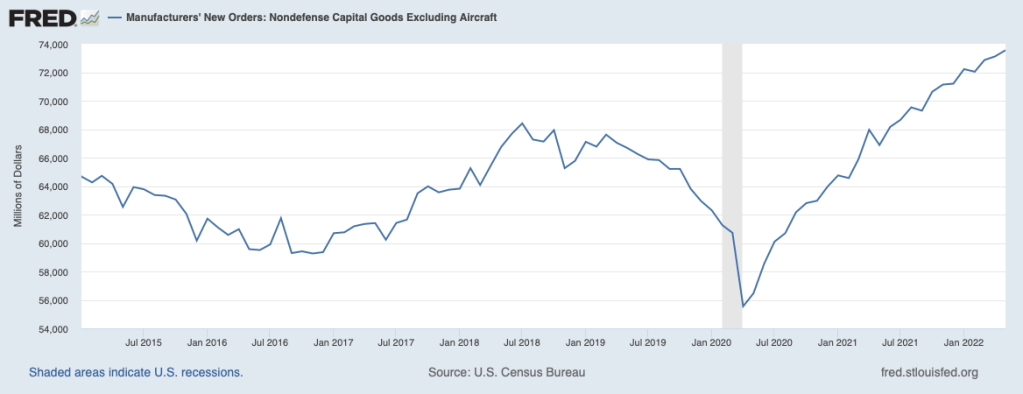

On the business spending side, the next chart, showing business orders for capital goods (excluding defense and aircraft orders), has been rising rather steadily in recent months and will be boosting aggregate demand in the months ahead.

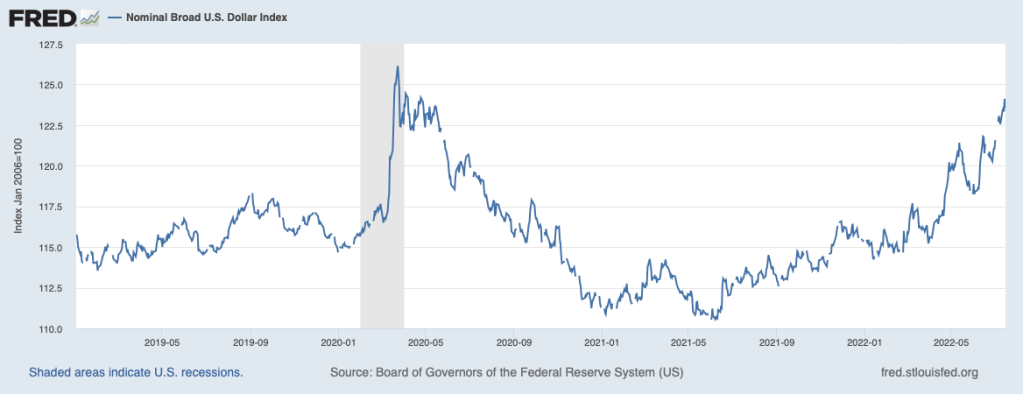

Moreover, the very strong dollar, shown next, has been restraining net exports, and once the dollar stops appreciating, the external sector will no longer be holding down output growth.

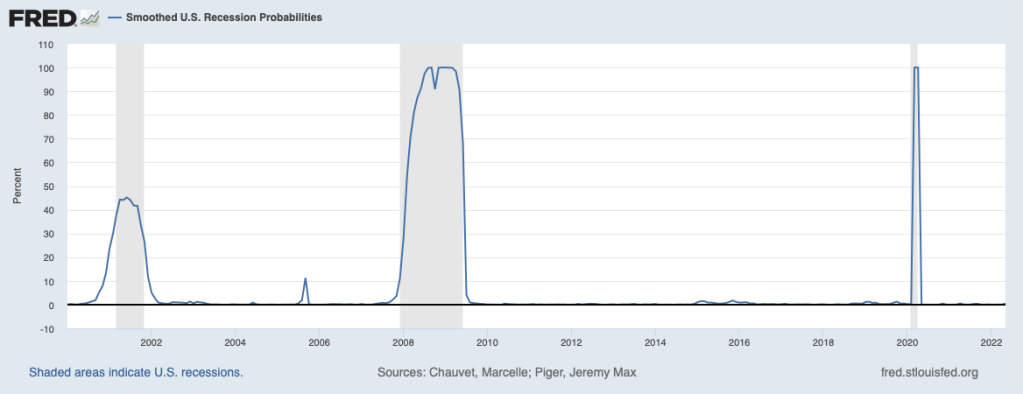

Thus, even though we have experienced a pause recently, output can be expected to pick up somewhat and a recession likely will be avoided. Indeed, a statistical model used for forecasting recessions shows that using data through May, the probability of a recession has been very low—below 1 percent. Most likely, the model will show a somewhat greater likelihood of recession once the forecast has been updated with data for June, but still not a worrisome prospect.

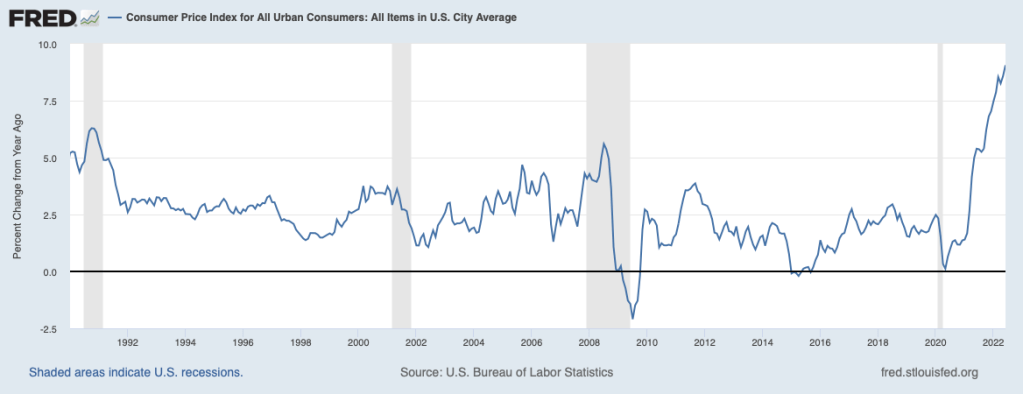

Meanwhile, the 9.1 percent twelve-month increase in the CPI through June—shown next—has added to angst over the inflation outlook.

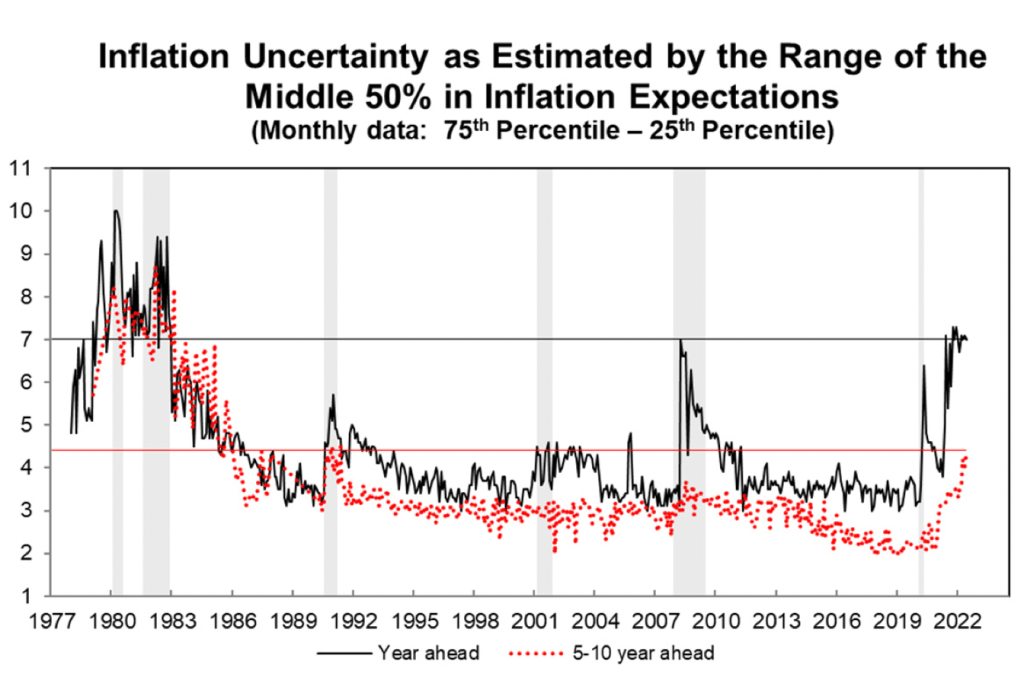

Worries caused by the spike in inflation have been a key contributor to the sharp deterioration in consumer sentiment, discussed above. Consumer confusion about inflation, drawn from the Michigan survey, has climbed to the range of the Great Inflation of the late 1970s and early 1980s. This is shown in the next chart containing uncertainty about inflation in the year ahead (black line) and the next five years (dotted red line).

To some degree, recent price increases can be attributed to extraordinary supply chain disruptions which are also constraining the supply of goods. Shown below is the Global Supply Chain Pressure Index prepared by staff at the Federal Reserve Bank of New York. The index shows that supply chain pressures have eased a bit in recent months but remain intense, continuing to limit goods available for sale and compounding inflationary pressures.

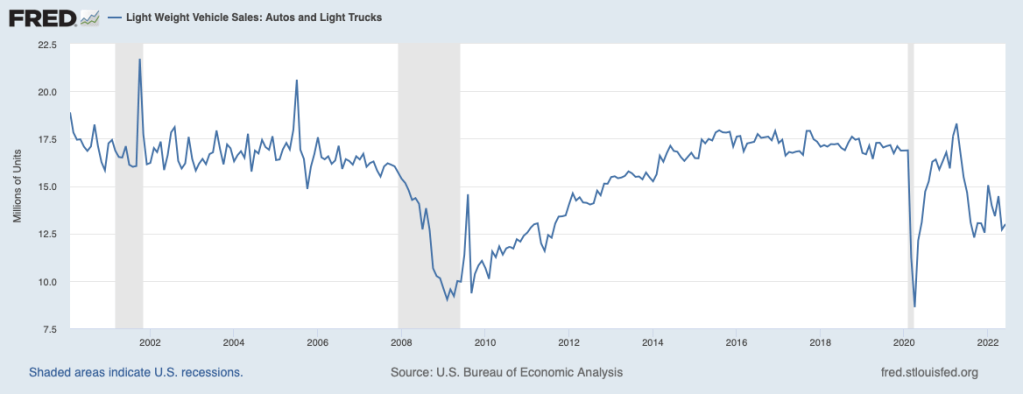

Supply chain disruptions have hit the motor vehicle sector hard. The next chart shows that auto and light truck sales are well below pre-COVID levels and have been largely flat over the past year, held down by lack of availability. Auto dealers have been struggling to get vehicles to meet demand and rebuild depleted inventories.

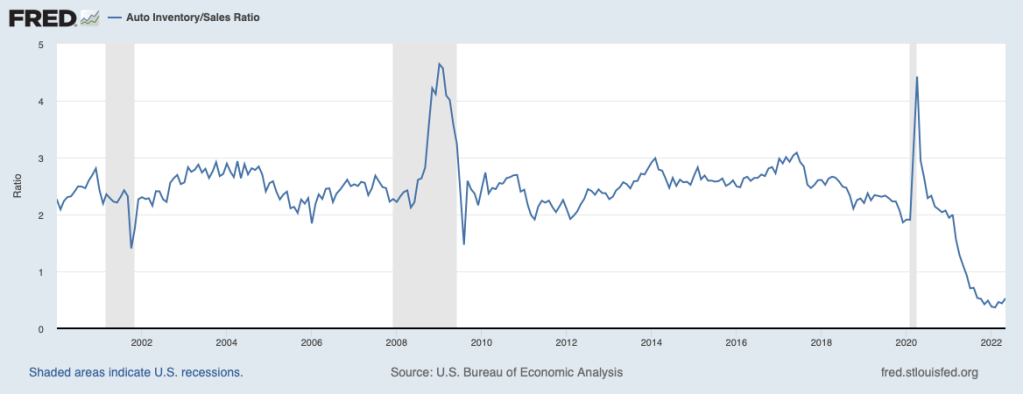

The following chart shows that the inventory-sales ratio for autos has barely moved up from its pandemic plunge. Motor vehicle assemblies will need to pick up a good bit for this important sector of the economy to recover fully.

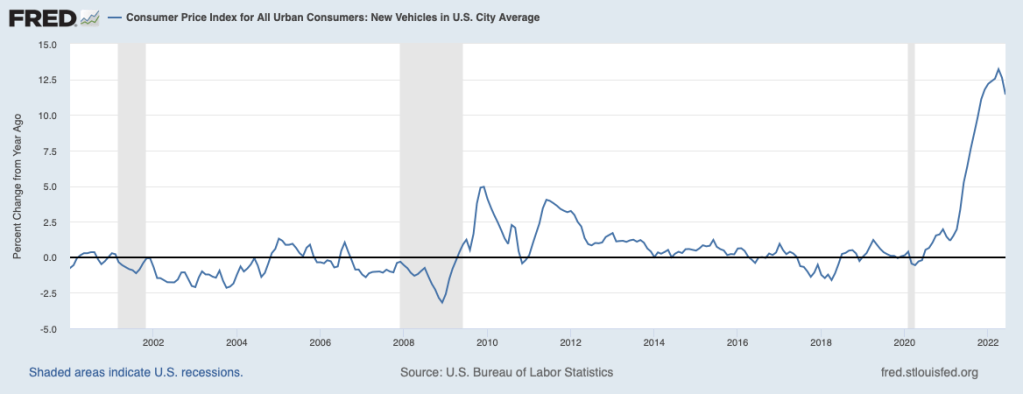

Meanwhile, we will continue to see outsized price increases, as shown in the following chart. Prices of autos have been increasing at roughly a 12 percent rate over recent months after nearly a decade of very subdued price changes. This discussion implies that car and truck prices are going to continue to rise briskly for the foreseeable future.

Producer prices for all goods at the final demand level, the blue line in the next chart, suggest that upward pressure on goods prices will continue in the months ahead.

More large price increases in the coming months are indicated by small business owners in the monthly survey of small businesses by the National Federation of Independent Businesses (NFIB). The chart below shows that the percentage of small businesses that plan to raise their prices in the next three months remains near its recent peak.

The above discussion suggests that inflation has taken on considerable momentum that will be difficult to reverse, short of pushing the economy into recession. As noted in recent commentaries (see June 21, 2022, What’s Ahead for the Fed’s Inflation Fight? and June 14, 2022, The Economy: More Hard Times Ahead) economic slack will need to develop and persist for a time to break the back of inflation, a lesson from the Great Inflation.

There are clearly some signs of slowing in the economy, such as in the previously red-hot housing sector, but the above discussion suggests that we can still expect aggregate demand to grow sufficiently to prevent much slack from developing—unless the Fed pursues a much more restrictive monetary policy than it has to date. Currently, the level of short-term interest rates is well below underlying inflation. Short-term interest rates will need to rise above inflation to create sufficient slack to turn the trajectory for inflation downward. The Fed’s anticipated path of short-term interest rates over the next couple of years—as well as those of market participants—will not be sufficient to curb inflation and place it on a downward path toward the Fed’s 2 percent target. In mid-June, the Fed predicted that the target for the federal funds rate will rise to the area of 3-3/4 percent at the end of 2023 and then drop to 3-1/2 percent at the end of 2024. That path will prove to be highly insufficient. The sooner the Fed acknowledges the need for and enacts more restrictive policy than currently contemplated, the sooner we will be able to get to the point at which we can reap the rewards of low inflation—notably sustainable economic growth and high levels of employment. When the recession arrives—sooner or later—is up to the Fed.