Headline inflation (that is, increases in the prices of all goods and services that consumers buy) has begun to slow. In July, the Consumer Price Index (CPI) showed no change from June in the average price that consumers pay for goods and services. Flatness in headline prices owed to a 4.6 percent decline in energy prices that partially erased an 11.4 percent increase over the previous two months. If food and energy prices are excluded (to derive the core CPI), consumer prices rose 0.3 percent last month.

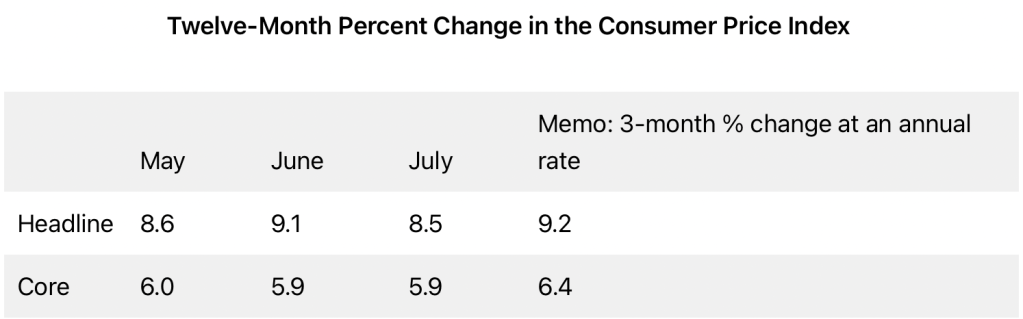

Shown in the table below are twelve-month percent changes in both headline and core CPI inflation. On a twelve-month basis, headline inflation slowed from 9.1 percent to 8.5 percent. However, core inflation was unchanged at 5.9 percent. Moreover, the annualized rate of price change over the three months ending in July was 9.2 percent for the headline CPI and 6.4 percent for the core CPI. Placed in perspective, these data suggest that it might be premature to celebrate the end of inflation.

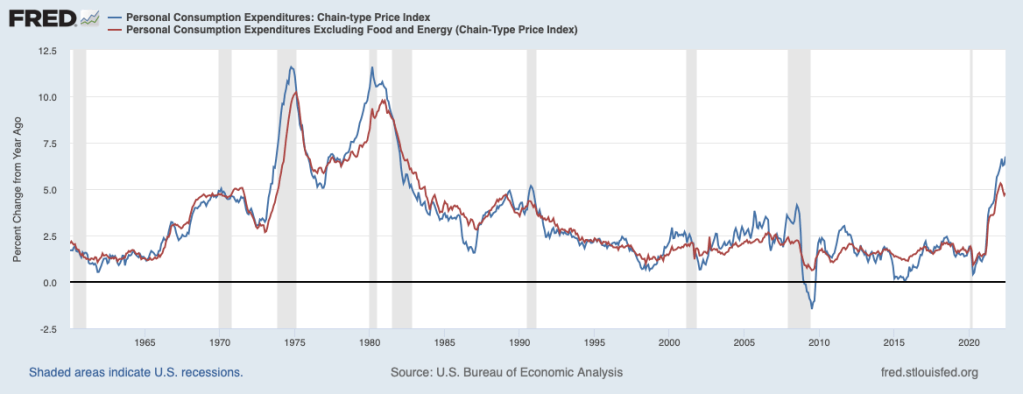

Turning to the Fed’s preferred measure of consumer prices (the Personal Consumption Expenditures Index) shown in blue in the chart below, headline inflation reached 6.8 percent over the twelve months ending in June (most recent data).

The June increase was boosted by fuel prices and was the highest rate in more than forty years. The June increase in PCE prices excluding energy and food prices—core inflation—was 2 percentage points lower, 4.8 percent. With the moderation in fuel prices over recent weeks, headline PCE inflation will be slowing, just as headline CPI inflation has slowed. With inflation slowing in both the CPI and PCE measures, should the Fed be moderating its trajectory for the federal funds rate?

By way of background, the Fed has said repeatedly that it is determined to bring inflation back to its 2 percent target and will do what is necessary to place inflation on a trajectory to that target. Implied is that the Fed will not back off until it is convinced that declining inflation will be sustained. With that in mind, will the slowing of headline inflation be grounds for a policy correction or will the Fed focus more on core inflation? It seems likely that the Fed will be using core inflation as a primary guide for its policy decisions. Also, to be certain that core prices are indeed decelerating, the Fed will need to observe a few more months of slowing to avoid being thrown off by the considerable noise in monthly price data.

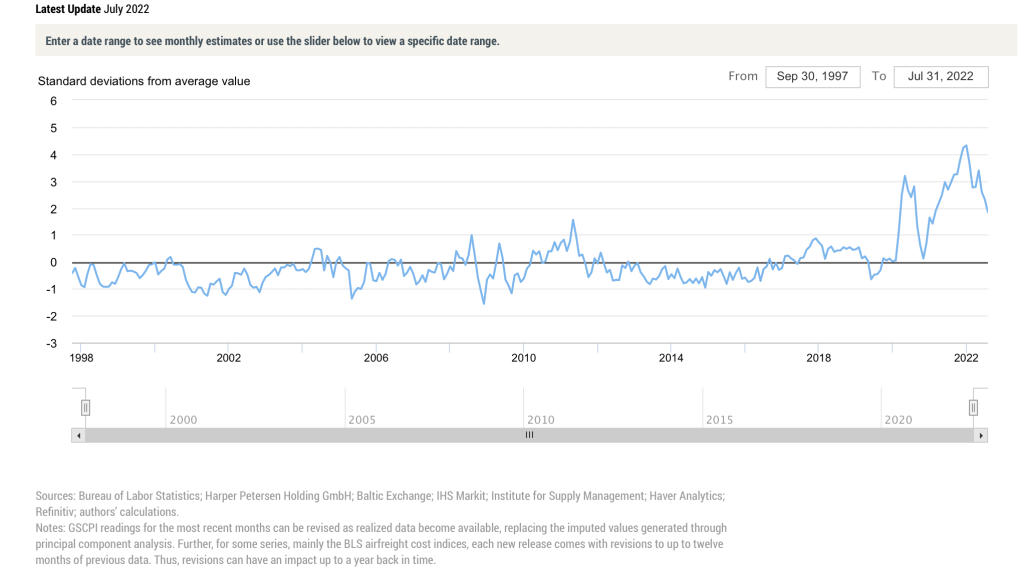

Supply chain pressures have contributed to price increases over the past couple of years and will be complicating the interpretation of monthly consumer price data. The New York Fed’s Global Supply Chain Pressure Index, shown below, has been heading downward over recent months. To the degree that this moderation is causing smaller price increases, there is a risk that smaller increases in core prices will be misread as a slowing in underlying inflation instead of one-off declines.

Global Supply Chain Pressure Index

As noted in previous commentaries (see July 25, 2022, The Coming Recession and June 21, 2022, What’s Ahead for the Fed’s Inflation Fight?) aggregate demand remaining in excess of aggregate supply has been contributing to underlying inflation. The most recent employment report—for July—suggests that the gap is sizable. The 3.5 percent unemployment rate for July is ½ to 1-1/2 percentage points below the level at which aggregate demand would be in line with aggregate supply. To bring aggregate demand below aggregate supply and begin to curb underlying inflation will require that short-term interest rates rise above the underlying rate of inflation. If recent readings on core inflation provide a good indication of underlying inflation, then the federal funds rate will need to rise to the 5 percent area or beyond to bring demand below supply. Previous commentaries have noted, too, that there is an inertia or persistence factor to the inflation process once inflation gets to the point it has been recently. This persistence factor needs to be unwound if inflation is to be placed on a sustainable downward trajectory. Meanwhile, inflation persistence adds to the amount by which interest rates must rise to bring inflation under control.

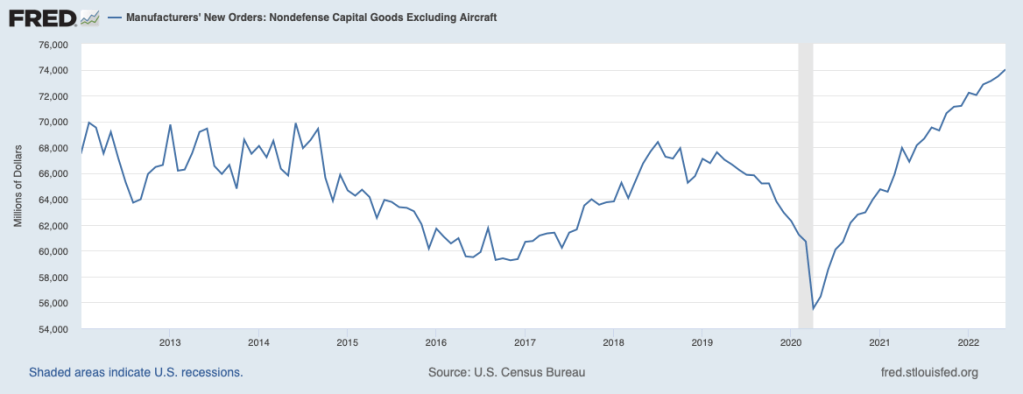

Thus, just how high the federal funds rate will need to go before inflation is indeed on a clear downward path to 2 percent will depend on the underlying strength in both aggregate demand and the persistence factor. Aggregate demand has decelerated in 2022, owing to a cooling of the housing sector and moderation in the growth of consumer spending. However, business capital outlays are likely to be rising in the period ahead, as implied by business orders for capital goods—shown below.

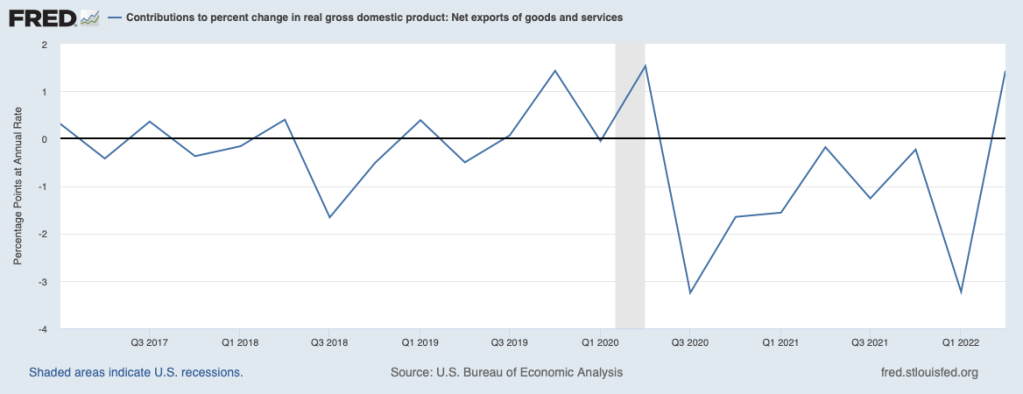

Some of the stronger demand for capital goods is coming from supply-chain disruptions that are causing many U.S. firms to diversify sources of supply and increase their reliance on U.S. suppliers; those domestic suppliers are increasingly finding it worthwhile to invest in more capacity to meet the rising demand. Also favoring the demand for U.S. goods and services should be the external sector. Shown below are contributions to growth in real GDP from net exports.

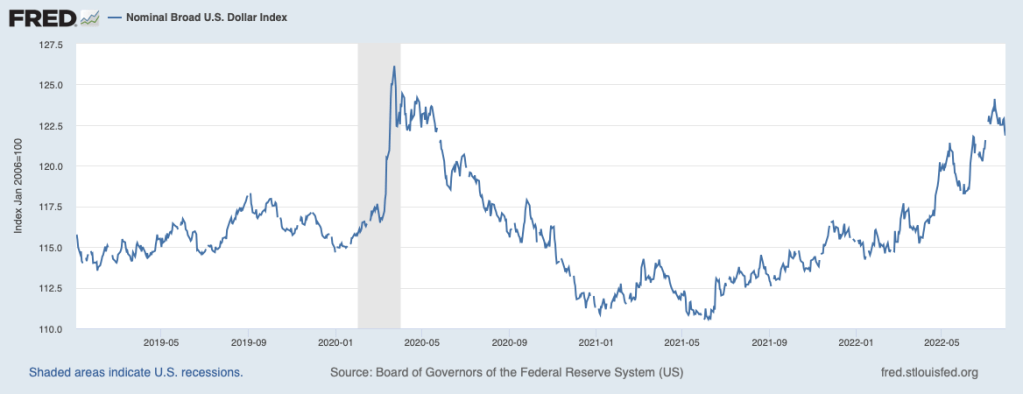

Net exports had been a drag on growth for nearly two years at a time when the dollar was strengthening, shown next, and the stronger dollar was worsening the competitiveness of U.S. exporters. With the dollar no longer rising, the drag coming from net exports should largely be coming to an end, and, indeed, net exports made a positive contribution to growth last quarter.

In sum, growth in aggregate demand has slowed, but not a whole lot. And this growth implies that interest rates will have to rise a good bit further to bring aggregate demand below aggregate supply to create enough slack so that underlying inflation moves distinctly in a downward direction. The more basic strength in aggregate demand, the more housing, and other interest-sensitive sectors will need to be displaced in the process. Furthermore, the persistence factor will add to the extent to which interest rates will have to increase to break the back of inflation.

Currently, financial market participants are of the view that aggregate demand is faltering, and they have not allowed for the inflation-persistence factor. As a consequence, market participants envision that the Fed will hike the federal funds rate to the 350 basis points area by the end of this year from the current range of 225 to 250 basis points and hold it there for a year. The Fed in mid-June foresaw that the target for the federal funds rate would be raised to the 325-to-350 basis point range by the end of this year and another 50 basis points in 2023. Neither market participants nor the Fed appears to have allowed for the persistence factor noted above, and, ironically, Chair Powell has emphasized that he believes that there remains some strength in demand.

Chair Powell also mentioned that the federal funds rate was likely to end this year above the so-called neutral rate, and when it gets there, it will be applying restraint on the economy. He mentioned that the (nominal) neutral rate is somewhere between 200 and 300 basis points. The nominal neutral rate is derived by adding underlying inflation to a neutral real interest rate of what is believed to be somewhere between 0 and 100 basis points. However, underlying inflation currently is not 2 percent points as implied by Chair Powell’s comment, but as noted above, on the order of 5 percent. In these circumstances, the neutral federal funds rate is 5 to 6 percent.

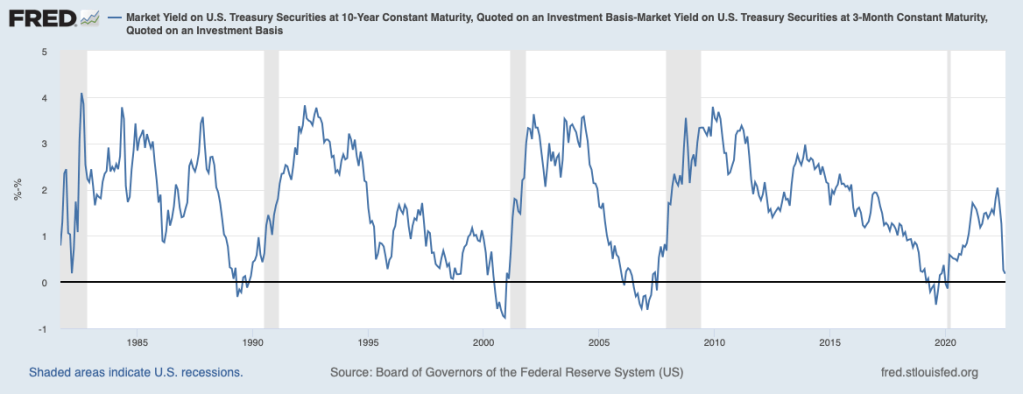

As the funds rate increases, it is likely that the yield curve shown below—the yield on a ten-year Treasury note less that on a three-month Treasury bill—will invert. In the past, inverted yield curves have preceded recessions, shown by the shaded area in the chart.

A concern being raised by some is that the Fed’s determination to get inflation down to its 2 percent target will lead to the Fed overdoing it and cause a deeper recession. These commentators are harkening back to the experience of the 1960s and 1970s—a period of so-called boom-bust policy cycles. During that time, the Fed would act to curb rising inflation by pushing the federal funds rate above what was sufficient to do the job and thereby compound the recession. In response to the recession, the Fed would reverse course and overstimulate the economy. The discussion above suggests that a recession is all but inevitable at this point for creating enough economic slack to get inflation under control, and achieving this will require continued large increases in the Fed’s target for the federal funds rate. The Fed is still far removed from a neutral policy stance, and, to get inflation on a sustained downward path will require that the federal funds rate be raised above neutral. Once it’s clear that the economy is in recession and inflation is clearly on a downward trajectory, the Fed will need to apply sound judgment in deciding when to begin removing policy restraints. If they begin easing policy too soon, then the hard-fought gains on the inflation front could well be thrown out.

One thought on “Will Slower Inflation Lead to a Slowdown in Fed Tightening?”