The more than doubling of IRS staff under the “Inflation Reduction Act” has caused a firestorm over who will be the focus (“targets”) of more tax audits and whether tax audits will be used for political purposes (“weaponization” of the IRS). This controversy raises the question of whether the current U.S. income tax system needs to be scrapped and replaced by something much simpler and less burdensome.

Taxes are imposed for purposes of raising revenue to finance government operations, influence behavior, and to transfer income. Excise taxes on alcoholic beverages and tobacco products are intended to discourage drinking and smoking as well as to raise revenue. The progressive tax on individual income is intended to transfer income from those in higher income brackets to those in lower income brackets as well as to raise revenue.

The current income tax system was imposed in 1913, following the passage of the Sixteenth Amendment to the Constitution that specifically authorized a tax on individual income. Before that time, the principal source of federal tax revenue came from duties on imports, and, to a lesser extent, excise taxes on items such as alcoholic beverages and tobacco products. Especially contentious were import duties. These duties were favored by manufacturing states that saw them as protecting their manufacturing industries against foreign competition but were opposed by agricultural states that correctly saw that such taxes were hurting their agricultural exports. The income tax was seen as a substitute for divisive import duties, and it enabled duties on imports to be lowered. For many, lower duties on imports were viewed as promoting international trade and achieving the gains that come with freer trade.

The extension of taxes to income expanded the tax base substantially. The tax base for the individual income tax includes earned (labor) income plus interest, rent, dividends, and capital gains—essentially what is labeled as personal income. In 1921, personal income was nearly five times larger than imports—$14 billion versus $3 billion. Similarly, today’s personal income is $22 trillion, roughly five times imports of $4 trillion. Thus, the personal income tax provided scope for considerably larger tax revenues and made it much easier for Congress to finance an expansion in federal government programs.

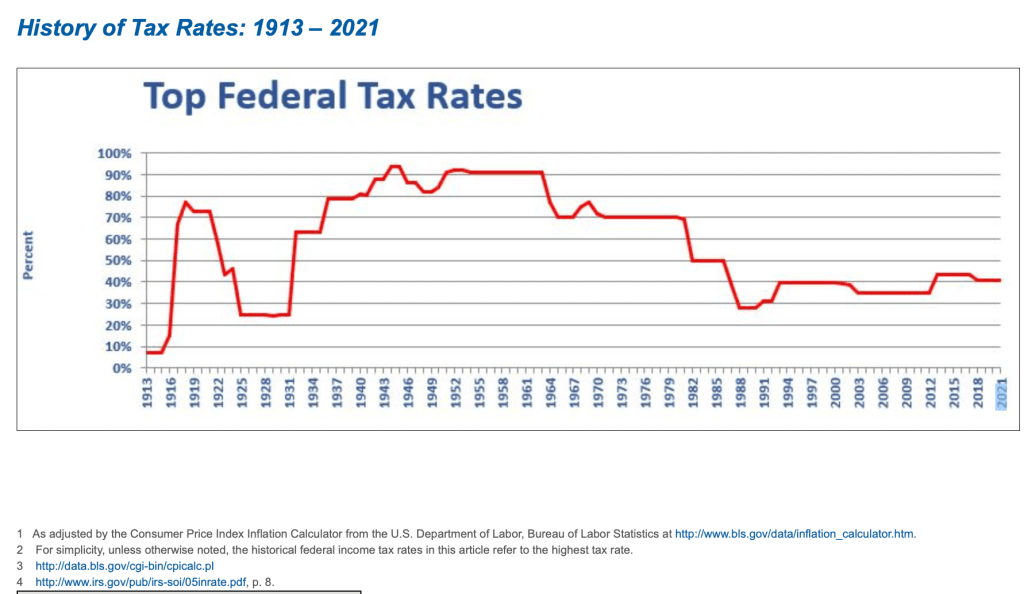

A notable feature of the personal income tax is its progressivity. The initial individual income tax in 1913 imposed tax rates that ranged from 1 percent to 7 percent, with tax rates rising as income increased. This can be seen in the chart below that has the highest marginal tax rate for each year from 1913 to 2021.

Notable from the chart is the sharp rise in the top income tax rate in both World War I and World War II. Wars require huge transfers of resources to the federal government from the private sector. Higher tax receipts provide the government with funds to procure war goods and personnel while, at the same time, higher tax payments by individuals curb the ability of individuals to compete with the government in buying goods and services. Tax rates were lowered after World War I, but not after World War II. After World War II, it was thought that lowering taxes would only add to inflationary pressure resulting from a huge overhang of pent-up private demand that developed during the war. (Political support for a progressive income tax can be better understood by relating the distribution of voters across income groups to the distribution of income. See October 27, 2020 commentary, Redistribution: Votes Versus Income Shares).

It took the Kennedy tax cut of 1964 to lower tax rates, especially the top rates. The rationale for lowering tax rates was to stimulate the economy—not only by boosting private sector demand for goods and services, but also by boosting supply. Lower tax rates were seen as encouraging more work effort by individuals and more risk-taking by entrepreneurs, each acting to boost supply. Stated differently, the higher the tax rate that a person faces, the less that person will want to work and the less will an individual want to take on risk. Also, lower individual tax rates translate into higher returns on income saved as future interest returns after the tax increase. A similar rationale was used for the Reagan tax cut of the early 1980s and the Trump tax cut of 2017.

Meanwhile, the individual income tax has become increasingly complex. Some of this complexity has resulted from efforts to change behavior. The deductions for charitable contributions and mortgage interest are intended to encourage charitable giving and home ownership. The exemption for employer contributions to pension plans and health insurance is intended to encourage saving for retirement and participation in health care plans. Child tax credits are intended to reduce the burden of providing for families, and the earned income tax credit is intended to give lower-income persons more of an incentive to work. The lower tax rate on capital gains is intended to encourage more risk-taking. Beyond these, some provisions satisfy special interests. Included among these are certain deductions allowed for purchases of yachts, private planes, and swimming pools. The individual tax provisions of the recently enacted “Inflation Reduction Act” will be adding even more complexity to the individual income tax code and the burden of our tax system on the economy.

It should be noted that there is also the so-called payroll tax that taxes earned labor income—wages and salaries. It is a flat tax that is 6.2 percent for Social Security (on labor income up to $142,800) and 1.45 percent for Medicare (plus 0.9 percent on earnings above $200 thousand). Employers are required to pay the same tax rates on each employee’s earnings, but a lot of evidence shows that the employer’s contribution is borne by employees in the form of lower wages and salaries. Thus, the payroll tax is a flat tax with an effective tax rate of 14.3 percent for most employees. The payroll tax and the individual income tax account for the vast bulk of federal tax revenues—85 percent.

As noted, the individual income tax has grown greatly in complexity. Indeed, the tax code today is roughly 700,000 pages. And the costs of complying with the tax code are enormous. Compliance costs include the time it takes for individuals to work on and complete their tax returns, costs of tax software, costs of accountants and other tax preparers, and the costs incurred by the Internal Revenue Service (IRS) in administering the system. The IRS does the tedious job of examining tax returns of individuals and reviews applications of charitable organizations for tax deductibility status and monitors them to ensure that donations to them meet the purpose of providing tax deductions, among other things.

It is estimated that the full cost of tax compliance ranges from $200 billion to $300 billion per year. Not included in those estimates are the distortions that the income tax causes to the allocation of resources. Included among distortions is the double taxation of earnings that are saved—when the income is earned that is saved and when earnings are received from those savings. Double taxation discourages personal savings by lowering the net return on saving. And lower saving leads to less capital accumulation. Capital accumulation fosters economic growth and boosts wages.

The recently enacted “Inflation Reduction Act” will only be adding to the costs of compliance. Moreover, the greater the size of the IRS, the greater the scope for government abuse—the potential for targeting certain individuals and members of certain groups.

The time for an overhaul of the individual income tax is long overdue. It is time to simplify the tax system and lower the burden it imposes. It is time for a flat tax on income. A flat tax would tax labor income and would not permit any deductions or exemptions. Step one would be for the taxpayer to sum annual labor income. Step two would be to multiply this income figure by the flat tax rate. The result would be the annual amount of tax owed to the U.S. Treasury. A flat moderate tax rate would encourage more labor input, more risk-taking, and more saving. The result would be more output and a higher overall standard of living. Under a flat tax, it would still be the case that those with higher incomes will pay more taxes. A person who earns 10 percent more than another person would pay 10 percent more in federal taxes. With a progressive tax, a person with 10 percent more income pays more than 10 percent in additional taxes.

It is important to keep in mind that achieving the kind of outcome just mentioned would require stiff resistance to pressures for preserving certain cherished exemptions and deductions—such as personal (family) exemptions and charitable deductions. Giving in to such pressures would open the door for other special exclusions, erode the tax base, and require a higher flat tax rate to garner the same revenue.

With a much-simplified tax system, the IRS could be scaled down sharply and professional tax preparers would be freed from tax preparation to produce output in other sectors of the economy. The main job of the IRS would only be to ensure that the labor income reported by taxpayers matched the amounts supplied by employers and that other forms of labor compensation, such as employee stock options, are included.

So, what kind of flat tax would be needed to bring in the same tax revenue as currently raised? A tax rate of around 16 percent would generate the same revenues as currently, once the economy adjusts to this new regime. As noted, a flat-tax regime would lead to more work effort, more risk-taking, and more saving and capital formation (fostering higher wages and salaries). In other words, the flat tax would expand the tax base, thereby enabling a lower tax rate to get those same revenues (16 percent versus 19 percent). While the economy is adjusting, however, revenues would fall short of current tax receipts with a 16 percent tax rate. (What is being proposed here is very similar to the tax proposal of Dr. Ben Carson when he was running for president in 2015. For full disclosure, I was a member of Dr. Carson’s economic advisory team. For more details about the effects of Dr. Carson’s proposal, see this link).

Keep in mind that the above discussion presumes that the payroll tax that supports social security and Medicare remains intact at current rates. The end result would be that workers would be facing a combined federal tax rate of 30 percent on labor income. Currently, some pay more than 30 percent while others pay less.

A criticism of the flat tax is that such a tax system would no longer be progressive in that higher-income persons pay a larger share of their income in taxes. Persons in higher income brackets would get a lower tax bill. However, it should be kept in mind that we have lived with a flat payroll tax system for quite some time and this has not been seen as objectionable. Moreover, many of those who are currently in the higher income groups were once in the lower income groups (ask folks over fifty how their income has changed over their lives). Additionally, all income groups would benefit from the greater risk-taking and capital formation that come about from a flat tax—a rising tide lifts all boats.

For a flat tax to be most effective, there should be tight constraints on the ability of Congress to modify the tax base and to raise the flat tax rate—such as setting a 15 to 20 percent range for the tax rate. These constraints would best be achieved through an amendment to the Constitution. With the greater certainty about future tax liabilities that the constraints would introduce, there will be less uncertainty about the returns from career choices and other longer-term decisions that would lead to better planning by individuals. Also, limits on the extent to which taxes can be raised would pressure Congress to be more careful about federal spending and force better prioritization of spending.

In closing, unless something dramatic is done to overhaul our personal tax system, it will only get more complex, will be more difficult to navigate, and will become a greater drag on the economy. Moreover, the scope for IRS audits and harassment will grow. Market-based economies have demonstrated over and over again that they are powerhouses when they are not shackled by ill-designed tax systems and over-regulation. Market systems have lifted huge numbers out of poverty and have provided rising standards of living for their overall populations (See Chapter 2 in my book, Capitalism Versus Socialism: What Does the Bible Have to Say? (Kindle, 2020)). The time has come to remove the shackles that not only are currently holding down our economy but promise to impose an even bigger drag in the years ahead.