On August 26, Fed Chair Powell sent a jolt through financial markets with his remarks delivered to the Federal Reserve Bank of Kansas City’s annual central banking conference in Jackson Hole, Wyoming. What did he say and why did he say it—and is there anything more to be said?

The Powell speech was focused on inflation and the Fed’s determination to bring it down to the 2 percent target. Chair Powell was attempting to convince businesses and households that the Fed would bring inflation back to 2 percent so that households and businesses would come to expect 2 percent inflation and their actions in the marketplace would be aligned with that target. As part of this effort, he acknowledged that a period of softer economic conditions would be needed by saying, “they (higher interest rates) will also bring some pain to households and businesses.” He went on to say, “These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

To a large extent, Chair Powell was trying to convince the public that the Fed fully understood that its policy of bringing demand into better balance with supply by raising interest rates to restrain aggregate demand would inflict hardship. But, despite the hardship, the Fed was committed to getting inflation back to 2 percent and was not delaying its application of tough medicine, “We are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2 percent.”

As noted, Chair Powell in his remarks was attempting to avoid any further deterioration of inflation expectations, especially longer-run expectations. If expectations of inflation move higher, inflation can be expected to pick up accordingly as businesses raise their prices faster and workers seek larger wage gains. The Fed would like to have long-term inflation expectations anchored around the 2 percent target. Instead, should expectations of inflation move above the target, it likely would take a period of lower inflation readings before businesses and workers become convinced that inflation will remain lower and revise downward their expectations of future inflation.

The Fed understands that it likely will take a period of monetary restraint and a slow economy before the Fed can be assured that it has completed its task, “Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy.” Chair Powell also cautioned that favorable news on inflation will be read carefully by the Fed, as “…a single month’s improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down”. (For more on this issue, see the August 11, 2022 posting, Will Slower Inflation Lead to a Slowdown in Fed Tightening?)

Delaying measures to bring inflation under control will only add to the cost: “History shows that the employment costs of bringing down inflation are likely to increase with delay, as high inflation becomes more entrenched in wage and price setting.”

At this point, to place underlying inflation on a downward path on a sustained basis will require that the Fed use its policy tools to bring aggregate demand below aggregate supply. Chair Powell envisions that the Fed’s moves toward monetary restraint will bring growth in aggregate demand below growth in aggregate supply (around 2 percent per year) until the level of aggregate demand no longer exceeds the level of aggregate supply. But, bringing aggregate demand to merely align with aggregate supply (this could be characterized as a semi-soft landing), the apparent objective of Chair Powell, will only preserve the underlying rate of inflation, not bring it down. Nonetheless, even bringing aggregate demand in line with aggregate supply will mean that the unemployment rate will need to move up from its current 3-1/2 percent rate to the 4 to 5 percent area. Thus, placing inflation on a downward trajectory will require that the unemployment rate rises to at least 5 percent—most likely in association with a recession.

The stronger aggregate demand the higher will interest rates need to rise to bring demand below supply. Chair Powell mentioned that he saw strength in the period ahead when he said, “While the latest economic data have been mixed, in my view our economy continues to show strong underlying momentum.” Strong underlying momentum means that interest rates must increase a good bit to counter that momentum and restrain aggregate demand enough to bring it closer to aggregate supply. Some of the strength that Chair Powell observes no doubt is coming from the massive fiscal measures over the past year or so, including the most recent cancellation of student debt.

As has been emphasized, the public’s expectations of inflation play a key role in the effort to bring inflation in line with the 2 percent target. If expectations of inflation rise above the target, something must happen to bring those expectations back to 2 percent. That likely will require actual inflation to decline to the 2 percent area—and stay there.

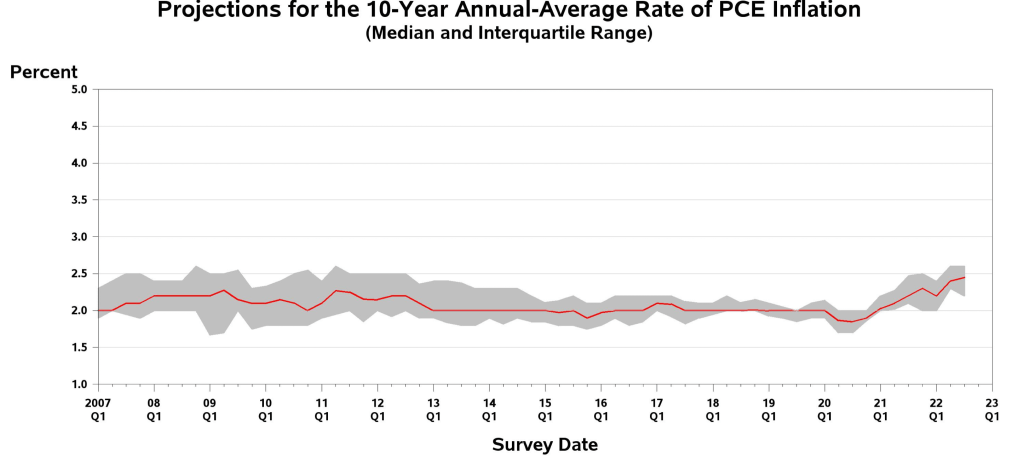

The next chart presents the long-term inflation expectations of professional forecasters. Over the past year, those expectations have moved further above the range that characterized the low inflation period that preceded 2021.

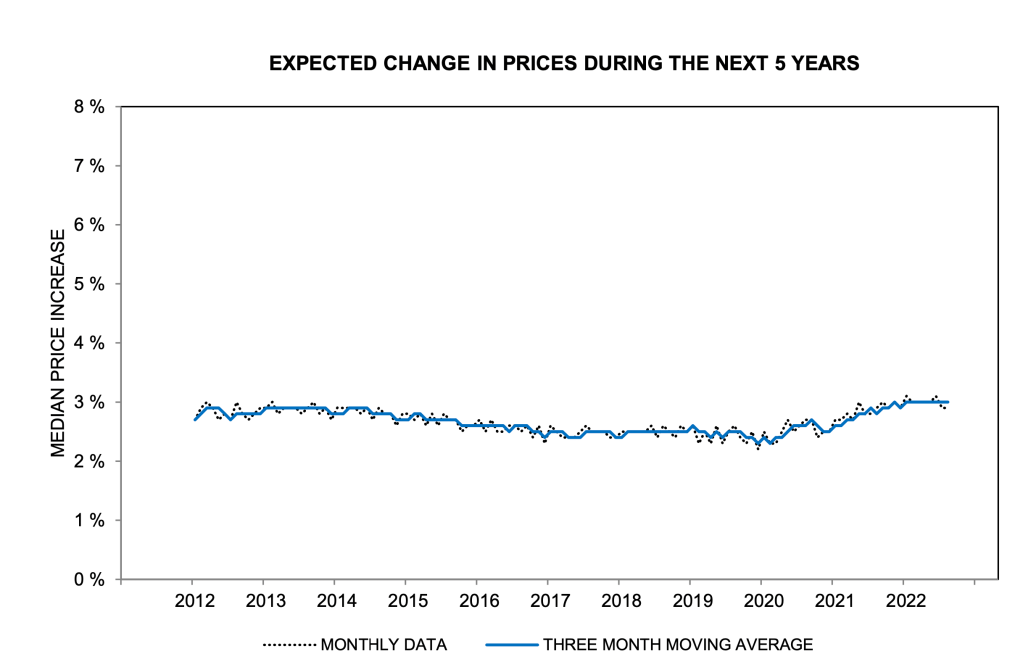

Much the same can be said of consumer expectations of longer-term inflation expectations, shown in the following chart. The extent to which consumer expectations of inflation have moved outside the earlier range is smaller than for professional forecasters.

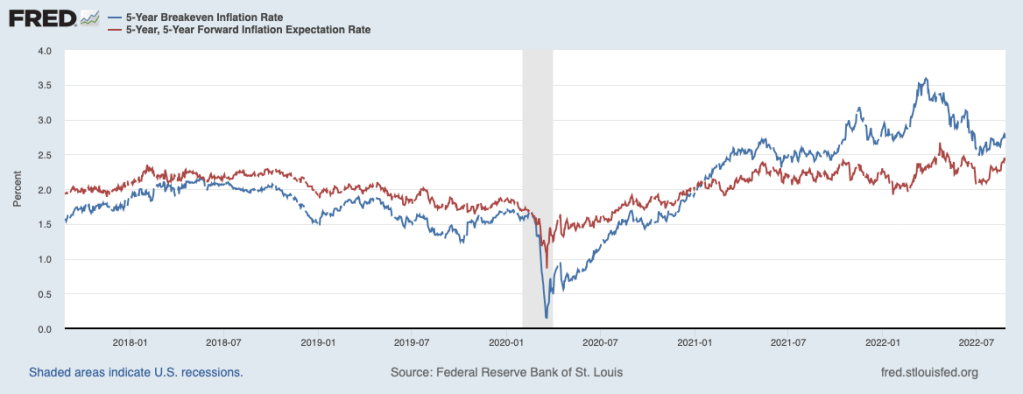

Still another measure of longer-term inflation expectations can be derived from the Treasury securities market. Shown next are five-year ahead expectations of CPI inflation (blue line) and five-year expectations of CPI inflation for the period starting five years from now (red line). These charts show that Treasury market measures of longer-run expectations, too, have moved a little above the pre-2021 period associated with low inflation. Chair Powell had a different take on this evidence when he said, “Today, by many measures, longer-term inflation expectations appear to remain well anchored.”

These exhibits suggest that the Fed’s job of returning inflation to a 2 percent rate has become more difficult because of some deterioration of inflation expectations over the past one and one-half years.

However, these measures of longer-run inflation expectations have not increased nearly as much as underlying inflation has moved higher. The relatively small increase may owe to the steady message over the past year of Chair Powell and other Fed officials that they are determined to return inflation to 2 percent.

The experience of the late 1970s and early 1980s tells us that there is a momentum factor that appears to affect inflation dynamics once inflation has risen above a threshold. This contributes to the inflation process along with inflation expectations and the amount of slack in the economy. The momentum factor may reflect public awareness of inflation (the extent to which it appears on the public’s radar screen), the actions that individuals and businesses take to protect themselves from the losses caused by inflation, and the degree of conviction (likelihood) that high inflation will persist. Chair Powell acknowledged that inflation has come to affect behavior widely when he said, “When inflation is persistently high, households and businesses must pay close attention and incorporate inflation into their economic decisions.” This momentum factor is adding to the extent that the Fed must apply restraint on the economy.

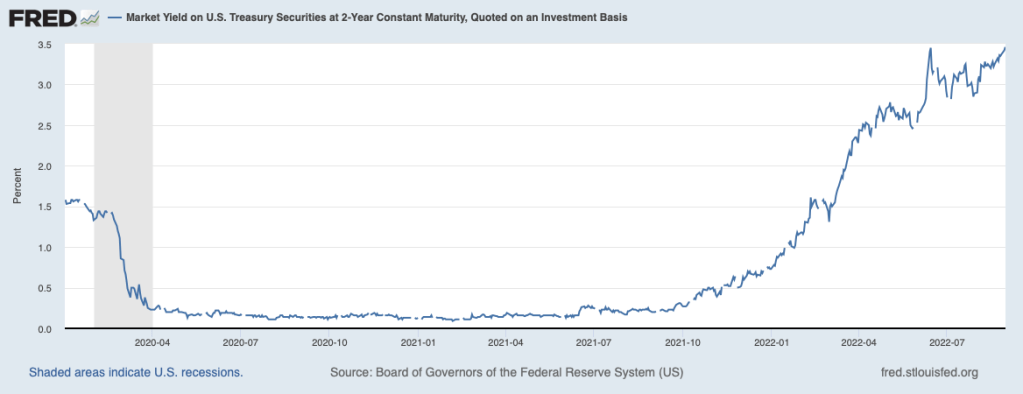

All of the above points to a big job ahead for the Fed in the period ahead—bigger than what the Fed and financial markets have come to foresee. The current situation implies that the Fed must bring aggregate demand below aggregate supply for a while to get underlying inflation on a downward path. Once the back of inflation has clearly been broken, inflation expectations and inflation momentum will diminish. To get to this point, short-term interest rates will need to rise above underlying inflation (around 5 percent currently) for a time. Market participants have slowly come to appreciate that interest rates need to be higher—as shown in the next chart showing the interest rate on the two-year Treasury note. But, at 3-1/2 percent, rates still have a ways to go before they will be applying sufficient restraint on the economy to successfully return inflation to the 2 percent target.

The bottom line is that, if the Fed is truly serious about bringing inflation under control, it will take more than a brief period of restraining growth in aggregate demand to be below growth in aggregate supply—and a mild increase in unemployment. It likely will require that interest rates rise a good bit above what is currently being contemplated and that demand is restrained enough to bring on a recession. In other words, the unfortunate costs of getting inflation back to 2 percent are going to be even greater.