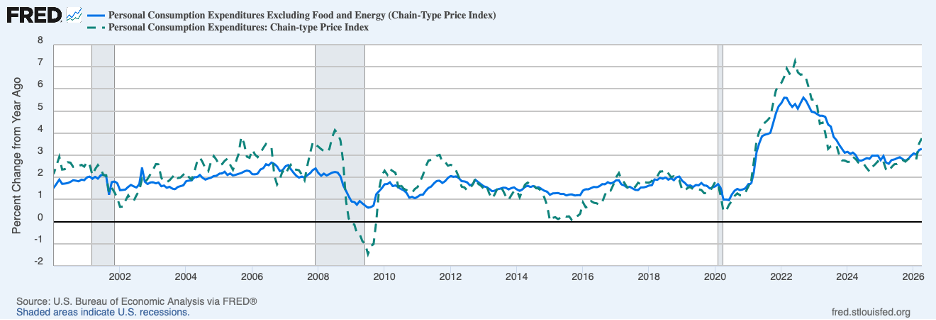

Financial markets have been rattled in recent weeks by disappointing news on inflation. A surge in energy prices, resulting from the conflict with Iran, pushed up the twelve-month increase in headline PCE prices 3.8 percent in April (the dotted green line in the chart below), up appreciably from 3.5 percent in March. Moreover, the twelve-month increase in the core PCE, which excludes energy and food prices (the blue line), rose to 3.3 percent last month, up considerably from 2.6 percent a year ago.

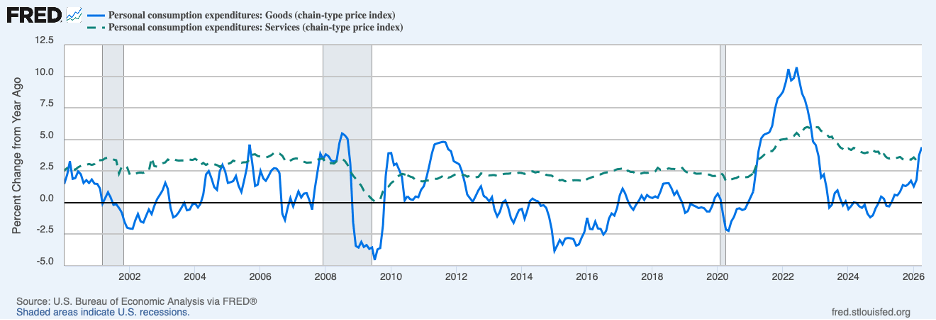

It has been convenient to attribute disappointing inflation news on (presumably) one-off shocks—the recent spike in energy prices and the April 2025 hike in tariffs (as well as the 2022 Russian invasion of Ukraine). These shocks have their primary impact on the price of commodities and the solid blue line in the chart below shows a sharp upturn in PCE commodity-price inflation.

Service prices have not been affected as much by these shocks and give a better reading of underlying inflation. The solid broken green line in the chart above shows that the twelve-month increase in PCE service prices was 3.5 percent in April, the same as a year earlier and well above the Fed’s 2 percent target; moreover, it exceeds considerably the 2.2 percent annual increase over the tranquil inflation period of 2010 through 2019.

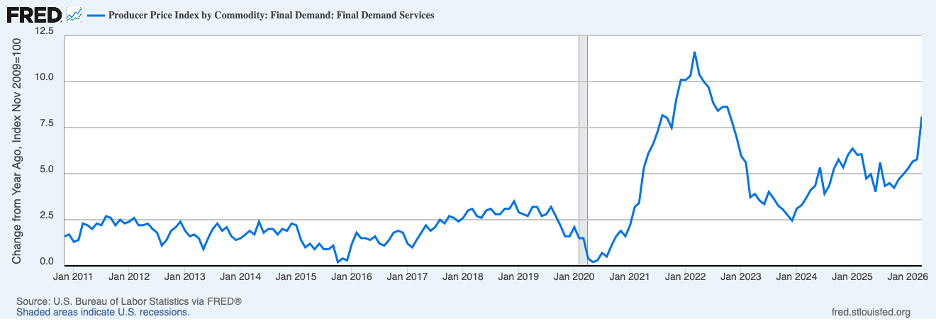

Stubborn service prices are evident not only in PCE (and CPI) prices but in other measures of prices as well. The chart below shows that service-price inflation in the producer price index has not only been high by the standards of the past one-and-a-half decades but has moved much higher in the past couple months.

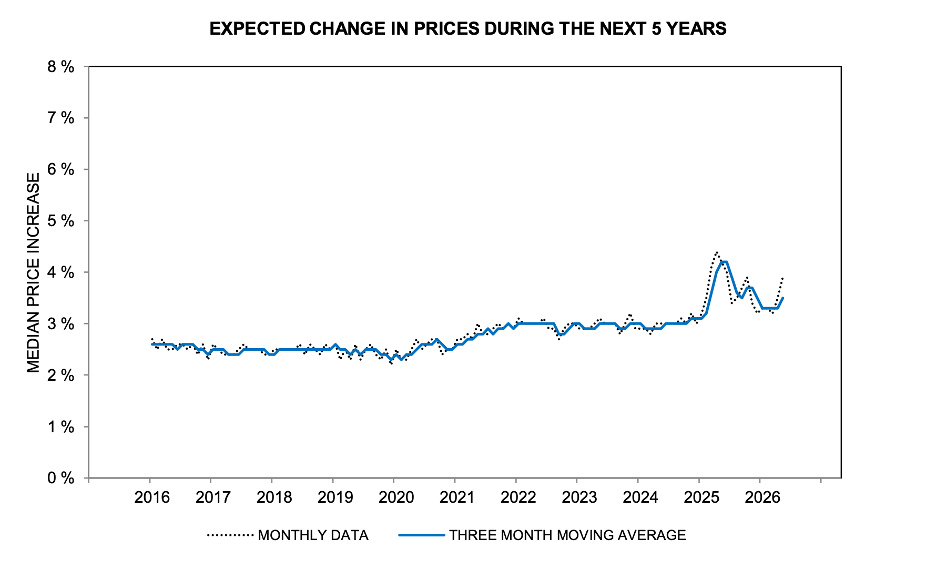

Discouraging inflation news is affecting expectations of inflation. The next chart shows consumer expectations of inflation over the coming five years from the Michigan Survey of Consumers. Those expectations have been increasing in recent months and are well above the decade prior to the pandemic.

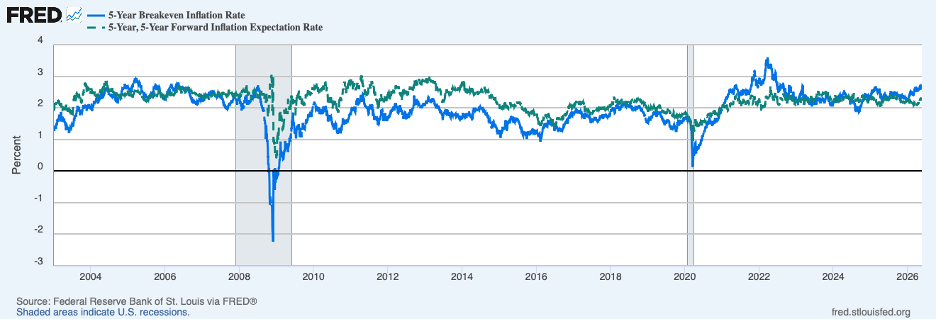

Evidence on expectations from the market for Treasury inflation protected securities (TIPS) is telling a similar story, as shown in the next chart. Expectations of inflation over the coming five years from the market for TIPS (the blue line) have decidedly turned upward recently and are well above the decade prior to COVID.

Less worrisome are expectations of inflation for the five-year period starting in five years (the broken green line in the chart above). They are not unusually high by the standards of recent decades. Some analysts tend to focus on such longer-term expectations and downplay shorter-term expectations as a contributor to underlying inflation (statements by Fed officials emphasizing their commitment to restoring inflation to the 2 percent target have no doubt helped to hold down longer-term expectations). However, expectations of inflation over shorter periods cannot be dismissed as a contributor to inflation dynamics.

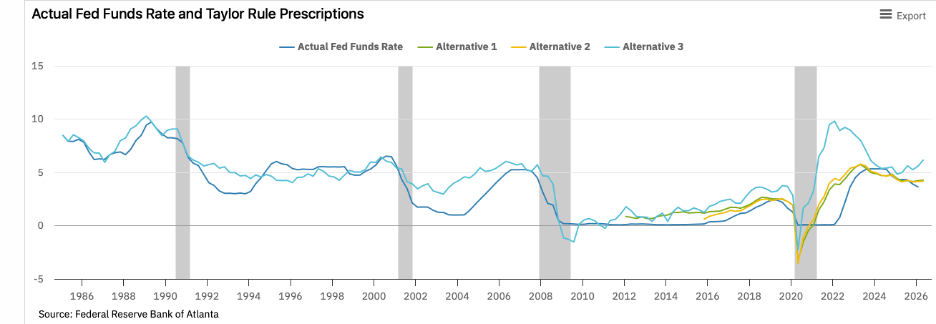

Thus, the evidence on underlying inflation clearly suggests that, even after the recent shocks contributing to inflation have worn off (that is, they prove to be one-off), there will still be a worrisome inflation problem for the Fed. In other words, the Fed’s current setting of the policy interest rate is too low. The next chart shows the range for the policy rate prescribed by a Taylor Rule that can serve as a rough indicator for the appropriate setting for achieving price stability. The range for the policy rate based on the Taylor Rule is 4.2 to 6.2 percent, well above the current policy rate of 3.63 percent. Moreover, this range may understate the true range because it is based on an estimate of the neutral interest rate (the rate at which policy is neither stimulative nor restrictive) that likely is too low.

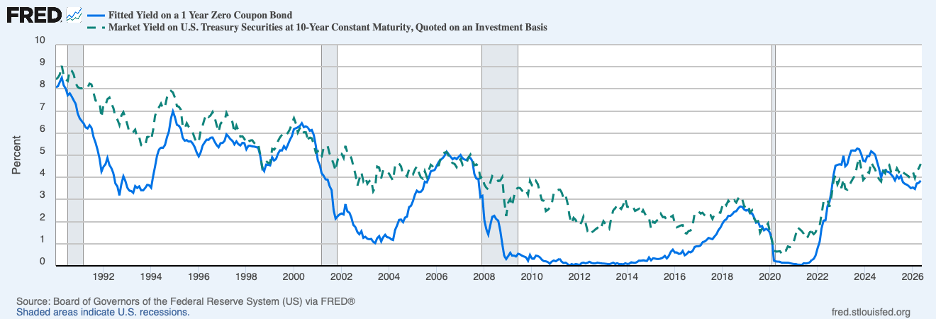

Market participants in recent days have come to expect no further rate cuts and are raising their odds of a rate hike. The broken-green line in the next chart shows the yield on a one-year Treasury security. This yield has risen as the disturbing inflation news has streamed out and now market participants see some odds that the Fed will raise rates by the end of 2026. Longer-term yields (the blue line) have also turned up recently. However, market participants have not priced in the full extent to which the policy rate will need to be raised to place underlying inflation on a clear trajectory toward price stability. Nonetheless, the recent upturn in rates is applying some restraint, although not enough.

Compounding the challenge facing the Fed, considerable pressure will come from the White House even if it only signals that higher policy rates are coming. If the Fed continues to postpone necessary rate hikes, perhaps by dismissing high inflation readings as one-off (transitory), the news on inflation will continue to be disappointing and high underlying inflation will become even more entrenched.

Header image: Andy He / Unsplash