The Fed’s new chairman, Kevin Warsh, has expressed skepticism about the value of the practice of forward guidance — Fed policymakers making public their expectations of future settings of the policy interest rate, the federal funds rate. Chairman Warsh underscored his skepticism at his first meeting of the FOMC as chair by not submitting a forecast. For some time, Reserve Bank presidents and members of the Board of Governors four times each year provide their expectations of where the federal funds rate will be at the end of the current year and the following two or three years (based on their judgment of what level of that rate is most consistent with achieving the dual mandate of maximum employment and stable prices). Policymakers have been giving federal funds rate projections since early 2012. Also published are Fed policymaker projections of growth in output, unemployment, and inflation.

The purpose of forward guidance is to get interest rates and their impact on business and household spending decisions aligned with achieving the dual mandate. The dilemma for the Fed is that a large share of interest-sensitive spending — business investment, home purchases, and consumer spending on big ticket items, such as cars — is based on longer-term interest rates while the Fed exercises direct control only over the overnight federal funds rate.

Nonetheless, a sizable portion of business loans — amounting to about a third of business debt — gets priced off of the prime rate or other rates that key off the federal funds rate. Forward guidance is intended to give the Fed greater influence over longer-term rates.

For a period of time in the wake of the financial crisis when the federal funds target was set at rock bottom — 0 to 25 basis points — the FOMC in its published statements following a meeting attempted to put further downward pressure on longer-term benchmark rates by convincing market participants that this target would remain in place “for some time,” “for an extended period,” and at one point even over a specified a minimum time interval; many market participants viewed these statements as commitments to hold the policy interest rate at this so-called zero lower bound, not just a forecast.

To better understand the reasoning behind forward guidance, it is helpful to look at the linkage between long-term benchmark rates (Treasury yields) and the federal funds rate. The long-term benchmark rate is believed to have two components: the average of short-term (federal funds) rates over the entire term of the security and a term (risk) premium that compensates investors for the risk of greater price movements of a security as its maturity increases. In other words, the yield on a ten-year Treasury note (a reference rate for pricing a lot of private debt such as mortgages and corporate bonds) equals the average expected federal funds rate over the next ten years plus a premium to compensate investors for the risk of price movements that they perceive when holding a ten-year instrument.

The Fed sets the current level of the federal funds rate (typically until the next FOMC meeting, around a six-week interval) and market participants form expectations of where they believe the Fed will be setting that rate beyond that point based on the outlook of market participants for the economy (output growth, the labor market, and inflation). If those expectations are in keeping with the most likely path of the economy and the Fed’s response, there is little need for forward guidance. Benchmark rates would be near those associated with achieving the dual mandate (with forward guidance, the Fed would only be affirming market expectations). However, if expectations in the market are at variance with the path associated with achieving the dual mandate, benchmark rates will depart from required levels. In these circumstances, forward guidance would be beneficial if the Fed had a more accurate forecast of the economy and how they will respond in setting the federal funds rate. Long-term benchmark rates would adjust more promptly to levels associated with achieving the dual mandate with the Fed’s forward guidance.

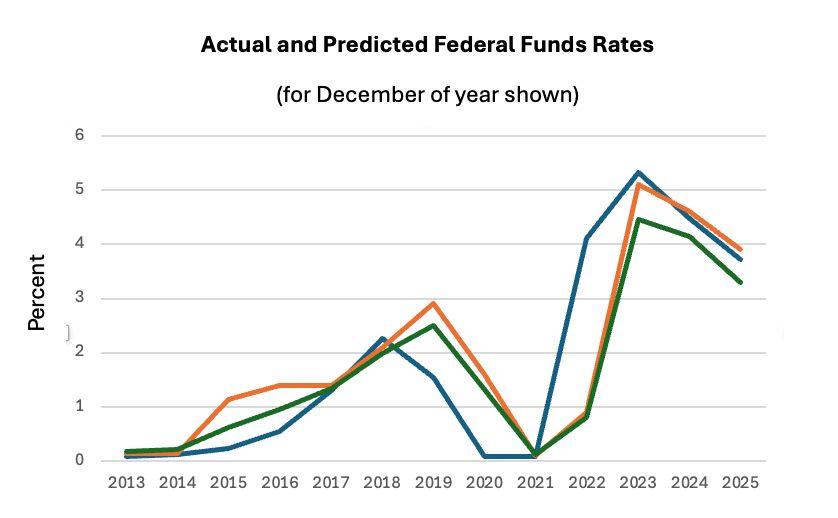

Thus, the usefulness of forward guidance boils down to whether the outlook expressed by Fed policymakers for the economy and the policy rate is more accurate than that of participants in the securities markets. Shown below is the actual federal funds rate in December of each year shown (blue line), the median federal funds rate forecast for that December made by FOMC members one year earlier (orange line), and the federal funds rate predicted for that December by federal funds futures one year earlier (green line). The period shown is 2013 (one year following the first published December FOMC forecast) to 2025.

The chart suggests that the Fed’s forecast of the actual federal funds rate is not any more accurate than the futures market. Indeed, for this time period, the forecast error of the median FOMC forecast is a bit larger than for the federal funds futures forecast (RMSE of 1.11 percent versus 1.06 percent). Thus, one might conclude that Fed forecasts of the policy rate are not beneficial and could be dropped. Moreover, one might argue that not only are Fed forecasts not beneficial, but, since they do not seem to be any better than market participants, they might undermine the credibility of the Fed; in undermining credibility, the forecasts could weaken the effectiveness of Fed monetary and perhaps other policies.

However, the issue is more complex than it might appear. Market participants benefit from knowing the thinking of policymakers, including quantitative forecasts. Fed quantitative forecasts of the policy rate and key economic variables, such as growth in output, unemployment, and inflation, constitute important information to market participants in making their decisions. Market participants do not ignore this information but rather process it along with other information in making those decisions. (Indeed, statistical analysis indicates that over the period shown in the chart the January forecast of the federal funds rate for the December of that year was significantly affected by the median year-ahead forecast of FOMC members published the previous month; however, market participants extrapolated only 83 percent of that forecast — not a full one-to-one — implying that they took other factors into consideration, also.) Market participants know that the Federal Reserve System has a large staff of professionals whose primary task is to perform in-depth analysis of incoming information and to utilize a well-informed understanding of how the economy works to prepare forecasts for policymakers who can then draw on this work to inform their own forecasts which they publish four times each year. Market participants can then make market decisions based on those forecasts as well as those of private-sector forecasters.

Research has suggested that an average of forecasts of the Fed and private Blue Chip forecasters generally does better than either alone; for example, see Alexander Chudnik and Enrique Martinez Garcia, Fed’s Forecasting Edge Ebbed Prepandemic, Persisted in Downside Inflation Surprises, FRB Dallas, May 21, 2026.

On balance, the arguments and evidence presented above come down on the side of the Fed continuing to provide forward guidance. Those forecasts contain information helpful to market participants and do not seem to have had any adverse effects on markets. Actually, daily volatility of the yield on the ten-year Treasury note declined appreciably in the year following the initial publication of FOMC member forecasts in January 2012 from the year leading up to the publication (the standard deviation declined from 0.64 to 0.20 from the year prior to the year following). In addition, longer-term inflation expectations derived from the market for Treasury securities — the monthly five-year, five-year forward expected rate of inflation — also were less volatile in the year following the initial publication than in the year prior (standard deviation of 0.15 percent in the year following versus 0.21 percent in the year before). Moreover, this evidence on longer-term inflation expectations, along with relative stability in longer-term inflation expectations over recent years when actual inflation picked up, suggests that Fed credibility has not been eroded as consequence of the Fed’s forward guidance.

Header image: Jaykumar Bherwani / Unsplash