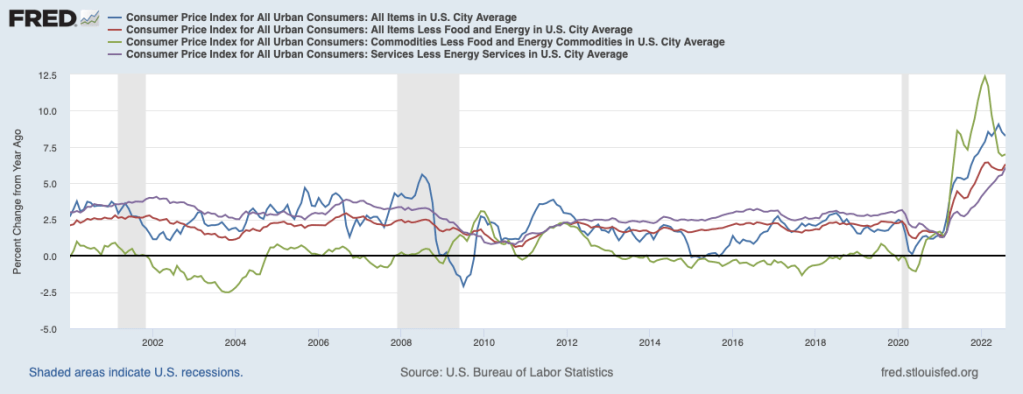

The CPI data for August was not greeted warmly by financial markets, even though there was another drop in headline inflation (measured on a twelve-month basis, the blue line in the chart below). What unnerved market participants was the upturn in core inflation (that removes volatile food and energy prices) after several months of decline (the red line).

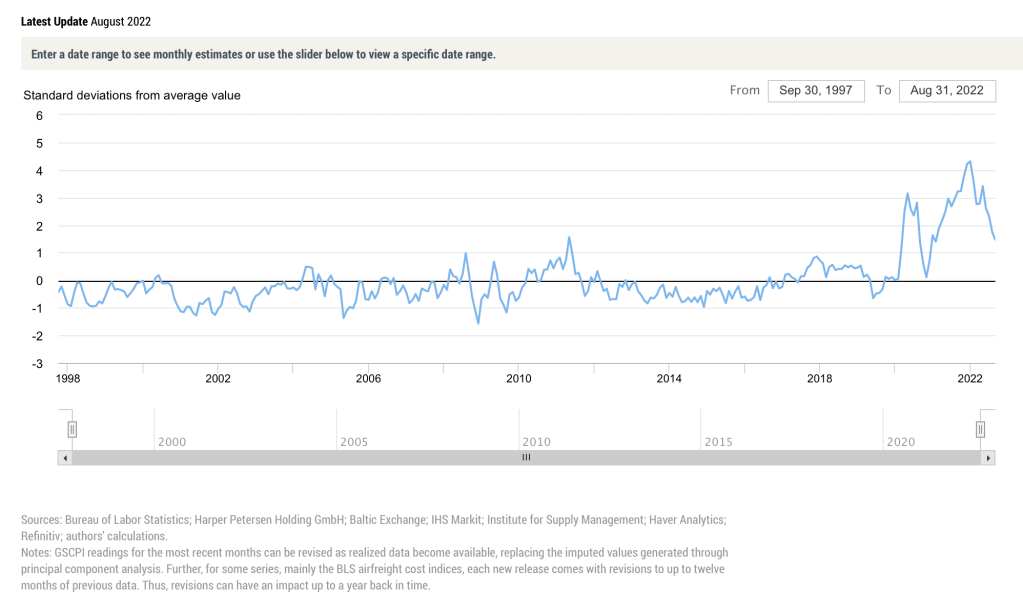

Digging more deeply, the upturn in core inflation owed to a further increase in service price inflation (excluding energy services, the purple line in the chart above) and an uptick in core commodity price inflation (the green line) after several months of moderation. Both service price inflation and core commodity price inflation had been steady and very subdued before the spring of 2021. The increase in core commodity price inflation into early 2022 is owed in part to intensifying supply-chain pressures, shown by the New York Fed’s Global Supply Chain Pressures Index in the next chart. However, the recent uptick in core commodity price inflation occurred despite the easing in supply-chain pressures since earlier this year.

In reading consumer price data, it is important to keep in mind that some factors driving price changes are one-offs (they affect the level of prices, but not the subsequent rate of change). Supply chain pressures fall into this category. But other factors affect the rate of change in prices. Inflation expectations and inflation momentum noted in previous commentaries (See, September 21, 2022, Chair Powell’s Remarks: What Did He Say and Why? and August 11, 2022, Will Slower Inflation Lead to a Slowdown in Fed Tightening?) fall into this category.

The persistence of core commodity price inflation and service price inflation well above rates that characterized the low inflation period before early 2021 and the pervasiveness of prices increases across categories of goods and services over recent months suggests that much of the recent high inflation is embedded in the inflation process and will be hard to reverse—that is, it is causing persistence in large price increases. Some of this persistence can be attributed to higher inflation expectations but much seems to owe to inflation momentum.

The job of reversing inflation falls squarely on the shoulders of the Federal Reserve (the Fed). Chair Powell and other Fed officials have been emphasizing over recent months their determination to return inflation to the Fed’s 2 percent target. And the more embedded the inflation is (the stronger its momentum), the higher will interest rates have to go to break the back of inflation and achieve the Fed’s intended results.

Currently, market participants foresee the Fed raising the target for the federal funds rate from its current 2-1/4 to 2-1/2 percent range to around 4 percent by early 2023 and holding it there until the second half of 2023 when the Fed is foreseen lowering the target gradually.

On September 21, the Fed likely will announce once again that it has raised its projection for the peak federal funds rate as it has over the past year. On that date, the Fed will release its updated projections for not only the federal funds target but key economic variables such as the unemployment rate and headline and core inflation. The table below shows the implied peak in the federal funds rate from Fed projections over the past year. The table illustrates that the Fed has steadily raised its forecast of the peak federal funds rate from 1.8 percent to 3.8 percent from September 2021 to June 2022. Moreover, the table shows that the Fed has moved forward the timing of the peak to 2023 from 2024. Nonetheless, the Fed has continued to be behind the curve over the past year, and, by doing so, has allowed inflation momentum to get stronger.

While it is clear that the Fed will raise its forecast for the peak in the federal funds rate, it is also likely that Fed policymakers will not raise the peak sufficiently and they will continue to be behind the curve in their thinking. The federal funds rate will need to rise above the rate of underlying inflation to get inflation on a downward trajectory. While it is difficult to calibrate the underlying rate of inflation, it is likely to be 5 percent or higher based on core inflation readings. This reasoning implies that the peak federal funds rate will need to be above 5 percent. The faster the Fed announces that it is raising its target for the federal funds rate, the more the Fed will be able to check inflation momentum—and underlying inflation—and the less will the federal funds rate ultimately have to increase to get underlying inflation on a downward trajectory. The sooner the Fed gets to announcing that peak and market participants revise their thinking accordingly the sooner the Fed will get to the point where it can begin easing off.

We can hope that the message delivered by the Fed on September 21 reflects an awareness of the need to be bolder in the months ahead. Also, it is increasingly clear that a soft landing is not in the cards and that a recession cannot be avoided if the Fed is to return inflation to the 2 percent target (See, July 25, 2022, The Coming Recession). If market participants get this message, then they will take actions that will tighten overall financial conditions sooner—higher long-term interest rates, larger credit spreads, reduced credit availability, lower equity prices, and a stronger dollar—and those responses will bring forward the return to low inflation and an economy that will be well positioned for steady and sustainable growth.