Recent news confirms that the Fed’s job of tightening monetary policy has a ways to go. The September employment report conveyed an ongoing tight labor market and the reluctance of idled workers to return to the labor force—with implications for a continuation of inflationary pressure coming from this market.

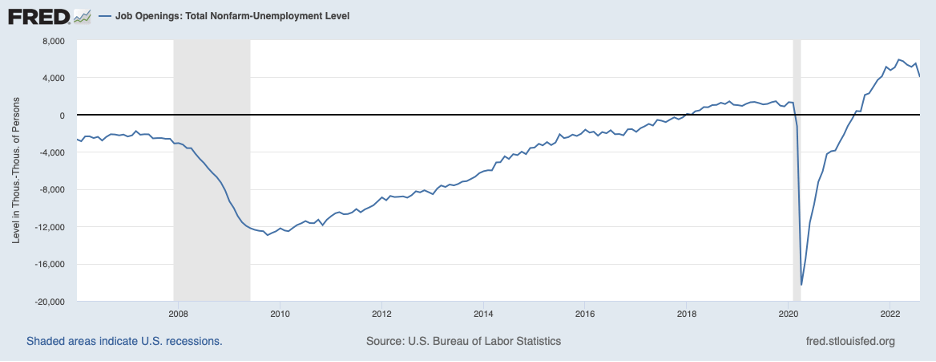

The most recent report on job openings indicates that the overhang of openings in excess of the number of unemployed—shown in the chart below—remains historically large despite a small narrowing in August.

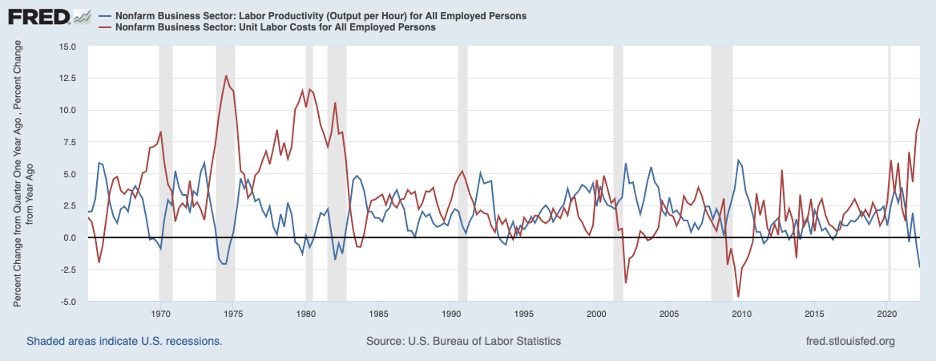

A story that has not gotten a lot of attention is the recent weakness in labor productivity and its implication for pressures on labor costs. The blue line in the chart below shows that growth in labor productivity has been very low or negative in recent quarters. Weakness in productivity has contributed to the surge in unit labor costs, the red line. Sluggish productivity may owe to COVID-related telecommuting and the enlarged rate of job turnover as workers respond to better opportunities resulting from plentiful job openings. These factors affecting productivity would appear to be temporary, but the longer they persist and contribute to inflation, the greater the chance they will contribute to momentum in the inflation process.

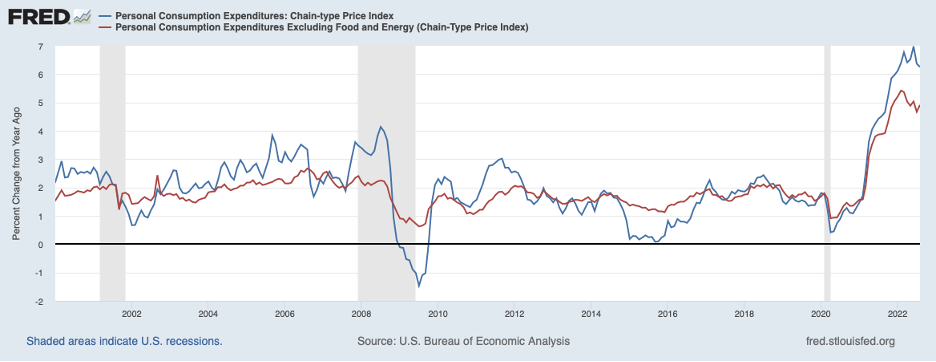

The most recent data on inflation indicates that underlying inflation remains persistently high. Core prices under the Fed’s preferred measure of inflation—the Personal Consumption Expenditures (PCE) Index, the red line in the next chart—show little chance of easing from 5 percent—and remain well above the Fed’s inflation target of 2 percent. The recent upturn in fuel prices will not only boost headline inflation—the blue line—but will indirectly boost other (core) prices through their effects on transportation costs and the costs of plastics and other petroleum derivatives.

The Fed, for its part, has come to realize that underlying inflation is more persistent and will require more monetary restraint. The table below shows Fed projections for core PCE inflation for the year 2023 and the federal funds rate at the end of 2023 as of September 2021, March 2022, and September 2022. The table illustrates that the projection for core inflation has risen from 2.2 percent to 3.1 percent over the year from September 2021 to September 2022. In light of this, the Fed foresees that it will be raising the federal funds rate to 4.6 percent by the end of next year—3.6 percentage points higher than a year previously.

Fed Projections for End 2023 (Percent)

| Projection date | Core PCE inflation | Federal funds rate |

| Sep. 2022 | 3.1 | 4.6 |

| Mar. 2022 | 2.6 | 2.8 |

| Sep. 2021 | 2.2 | 1.0 |

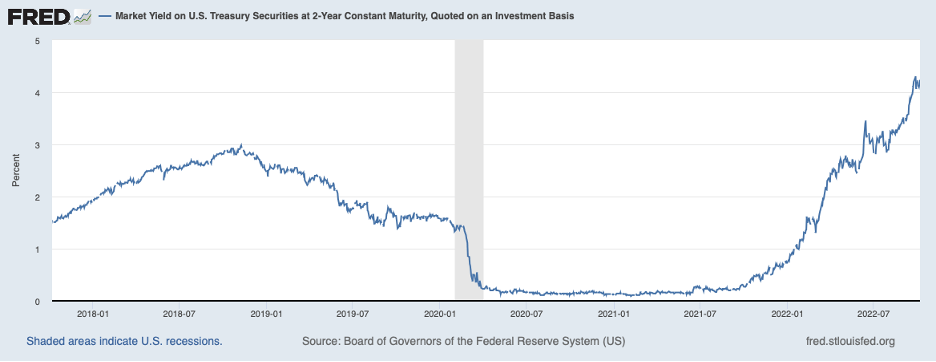

Market participants have come to expect more Fed tightening, too. The next chart shows the yield on the two-year Treasury note, which has risen from around 25 basis points in September 2021 to the 4-1/4 percent area most recently.

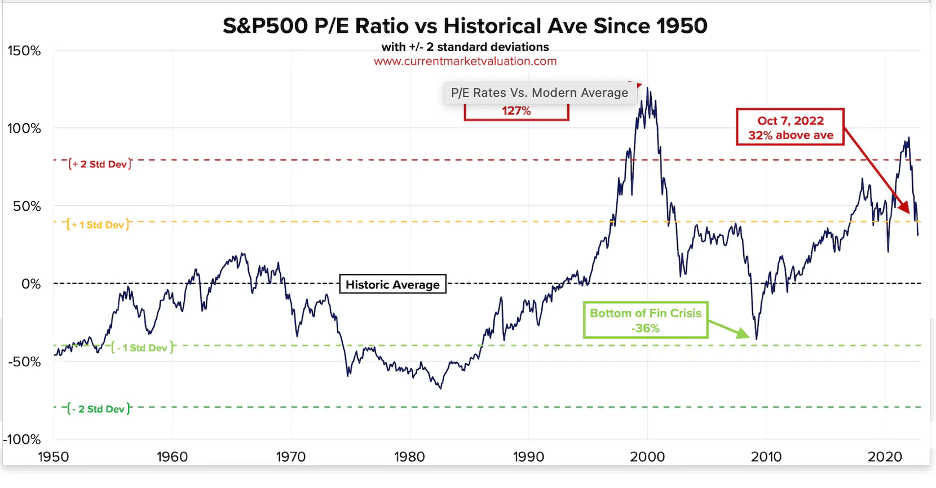

In keeping with this changing outlook for inflation and interest rates, stock prices have fallen nearly 20 percent, dragging down the Price-Earnings (P-E) ratio for stocks—as shown below. The sell-off of stocks is having the expected effects on the economy of curbing household and business demands for goods. Nonetheless, the P-E ratio remains well above—nearly a standard deviation above—its historical average. The still-high P-E ratio suggests further scope for stock price declines, given the current outlook for monetary policy by market participants.

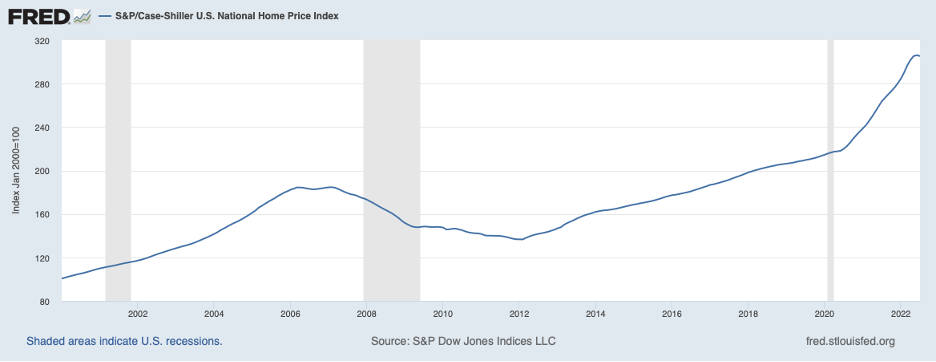

Similarly, the rise in the mortgage interest rate from 3 percent in September 2021 to 6.7 percent is having the intended effects on the housing sector as home construction activity and sales have slowed. The softer housing market is putting downward pressure on home prices. The chart below shows that home prices edged lower in July (latest data) after a substantial two-year run-up.

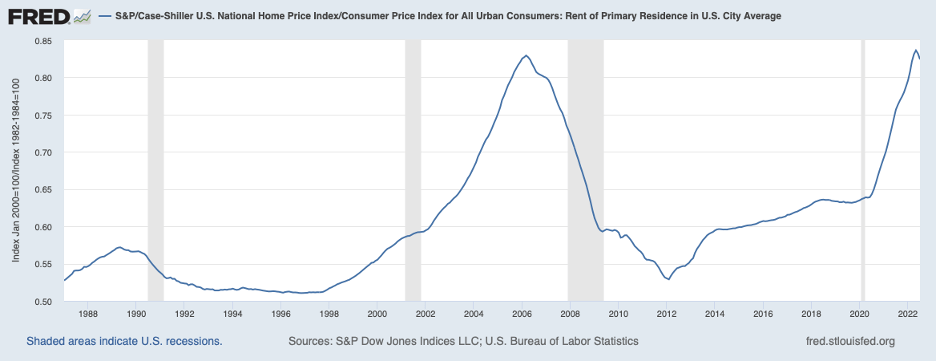

This run-up lifted the ratio of home prices to rents—the next chart—to the territory last reached during the home price bubble of the first half of the decade of the 2000s.

The high ratio of home prices to rents implies—as with the P-E ratio for stocks—that there is scope for further declines in home prices. (However, home prices are likely to adjust more slowly than stock prices because homeowners tend to be reluctant to accept the lower prices for their homes required by new market realities).

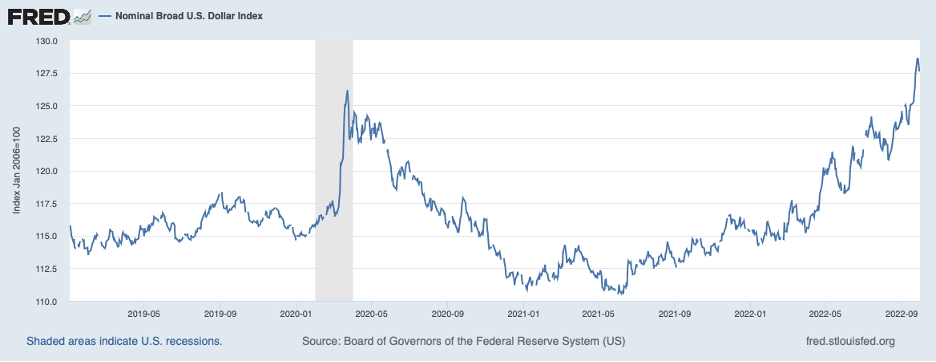

Turning to the external sector, expectations for Fed tightening are placing upward pressure on the dollar which is acting to reduce the price-competitiveness of U.S. producers and acting to lower prices of imported items. This can be seen in the chart below, showing an index of the purchasing power of the dollar.

The run-up in the dollar over recent months will be acting to curb U.S. exports and encourage U.S. consumers to shift to buying more items from abroad. The stronger dollar will also act to hold down consumer prices for a while but not on a sustained basis.

Although the Fed has come to realize that there is more persistence to the current bout of inflation than previously acknowledged, the Fed appears to continue to be overly optimistic about prospects for disinflation. In its most recent set of projections, the Fed foresees core inflation dropping from 4.5 percent in 2022 to 3.1 percent in 2024. However, it even seems unlikely that inflation over the final months will slow sufficiently to register a 4.5 percent increase for the full year—given that inflation for the year through August was a robust 5.0 percent. Moreover, the persistence factor suggests that the underlying rate of inflation in 2023 will not slow 1-1/2 percentage points in one year, especially given that the Fed’s projected nominal federal funds rate of 4.6 percent by the end of 2023 would surely still be below the underlying inflation rate. The resulting negative real interest rates would continue to be imparting monetary stimulus—and not restraint—to the economy.

As a consequence, the Fed will need to boost the federal funds rate above 5 percent and hold it there for a while to break the back of inflation and place inflation on a distinctly downward trajectory to 2 percent. Such an outlook means that interest rates and the dollar will need to move higher and stock and home prices will need to move lower than currently envisioned by the Fed and market participants.

In sum, the Fed’s tightening measures to date and projections for more are having the intended effects of raising benchmark interest rates and lowering asset prices, and strengthening the dollar which, in turn, are acting to curb aggregate demand. However, it is going to take more monetary restraint than either the Fed or market participants are contemplating to return inflation to 2 percent. This assessment implies that even more loss will be inflicted on wealth positions and pain on producers of goods and services and their workers than currently being expected if the Fed is serious about returning inflation to 2 percent.