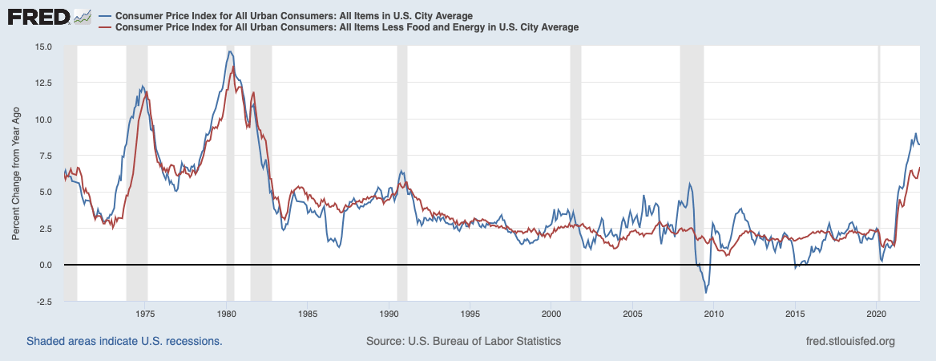

The Consumer Price Index (CPI) for September all but guaranteed that the Fed on November 2 will hike the federal funds rate another 75 basis points to 3-3/4 to 4 percent from its current 3 to 3-1/4 percent. As shown in the chart below, headline inflation—the blue line—stayed above 8 percent in September while core inflation (excluding food and energy prices)—the red line— rose to 6.7 percent, the fastest pace in forty years.

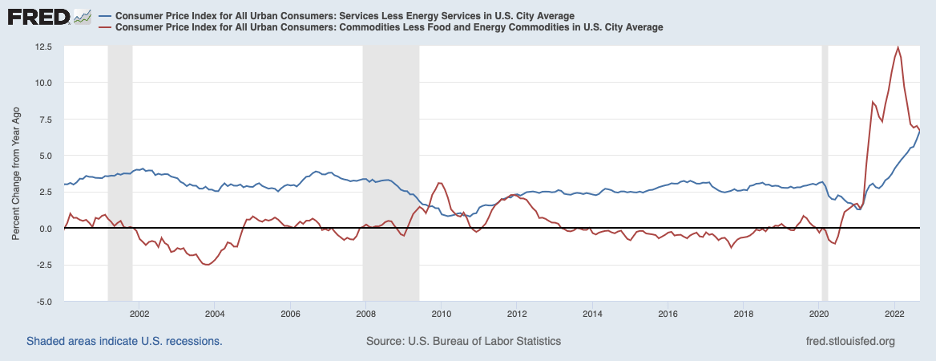

The September CPI data further confirmed that high consumer price inflation has developed a momentum that will be hard to reverse. Price increases were widespread and service prices, the blue line in the chart below, continued to accelerate in September even as commodity-price inflation moderated further.

Commodity prices in recent months have benefited from an easing of supply chain disruptions and a very strong dollar. Once supply chain pressures and the dollar stabilize, these factors holding down commodity price inflation will fade.

Once the inflation process has gotten to this point, it takes tough medicine from the Federal Reserve to curb it and place it on a downward trajectory. Market participants have gradually come to this realization. Shown in the next chart is the yield on the two-year Treasury note which captures market expectations for the federal funds rate over the next two years. This yield has risen nearly 4 percentage points since the beginning of 2022. Embedded in the current two-year yield is the expectation that the Fed will raise the federal funds rate to the 4-3/4 to 5 percent region by early 2023 and hold it there much of next year before easing off somewhat toward the end of 2023.

Corresponding to current expectations for the path of the federal funds rate are long-term real interest rates—interest rates after removing inflation—that have also risen sharply this year, moving from negative to positive territory. This can be seen in the next chart showing the yield on the ten-year Treasury inflation-protected security which recently has climbed above 1-1/2 percent.

At issue is whether a real long-term interest rate in the 1-1/2 percent range is applying restraint on the economy. Note that the ten-year real yield recently is still well below the level that prevailed before the financial crisis in 2008. The comparison between the recent real yield on the ten-year Treasury benchmark security and its yield nearly twenty years ago is complicated by changing fundamentals affecting real interest rates. In other words, there is a great deal of uncertainty about the current neutral level of this interest rate—the level of this yield associated with neither monetary stimulus nor restraint.

There are reasons to believe that the neutral interest rate is lower today than it was a couple of decades ago. Thus, a 1-1/2 percent real yield today is providing less stimulus than it did a couple of decades ago. Still, to break the back of inflation, the real ten-year yield will need to increase further, implying that the Fed will need to boost the federal funds rate well above 5 percent. (Note that underlying inflation currently is on the order of 5 percent or higher and short-term real interest rates will need to be distinctly in positive territory—that is, the nominal federal funds rate will need to exceed the underlying rate of inflation—for monetary policy to be restrictive.) That is, market participants will need to revise further upward their expectations for the Fed’s policy interest rate if the Fed follows through on its pledge to bring inflation down to its 2 percent target.

It should be noted that the current momentum in inflation will require that restraint be applied for a longer period than currently thought. As noted, market participants foresee the Fed starting to reverse interest rate increases toward the end of 2023. The momentum factor suggests that reversing policy that soon would not break the back of inflation and would risk raising doubts about the Fed’s commitment to its 2 percent inflation target.

Going forward, there will be a lot of debate within and outside the Fed about when the Fed needs to slow and then stop its policy tightening. This debate will reflect uncertainties about the relationship between the Fed’s primary policy instrument—the federal funds rate—and inflation outcomes, compounded by considerable lags between changes in the policy instrument and its effect on inflation and also by perceived risks. Because of the inherent lags, an optimal policy under which there are no such uncertainties would have the Fed start to take its foot off the monetary brake before inflation actually turns downward. Easing monetary restraint too soon risks undoing the sacrifices made to bring inflation down and likely compounds the difficulty of any subsequent attempt to get inflation under control. On the other hand, staying restrictive too long risks an unnecessary loss of employment and output and possibly undershooting the 2 percent inflation target. The sides on the part of policymakers and analysts regarding which risks are most serious are being revealed with each passing day.

In sum, market participants have come a long way in revising their outlook for Fed policy in light of the persistence of inflation. And these revisions are bringing forward in time the effects of monetary restraint on interest rates and asset prices and ultimately their effects on the economy and inflation. However, the stubbornness of the current inflation situation means that it will take even more monetary restraint and for even longer than currently contemplated if inflation is indeed to be turned around. We are entering a period when the debate about when the Fed needs to slow its pace of policy tightening and bring it to an end is going to intensify. The momentum in the current inflation process cautions against slowing and stopping too soon.