Recent data on the labor market, including the October monthly employment report and weekly initial claims for unemployment insurance, indicate that excess demand for labor persists. The extremely tight labor market was an underlying theme of Fed Chair Powell’s press conference on November 2.

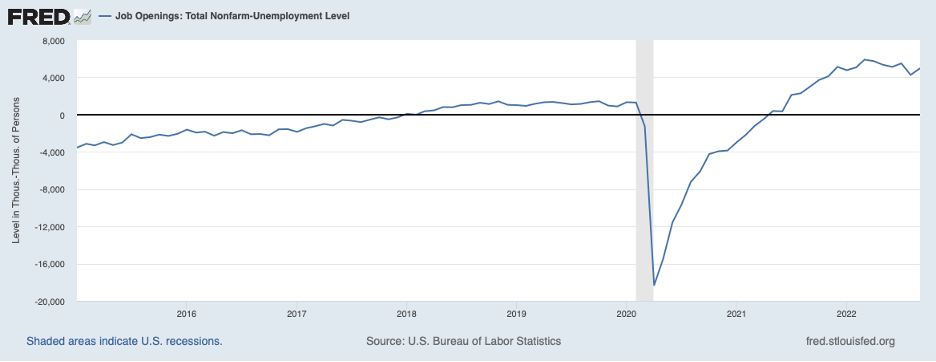

The chart below shows the excess of job openings over the number of unemployed workers, an indicator of the excess demand for labor. That excess remained large through September (latest data).

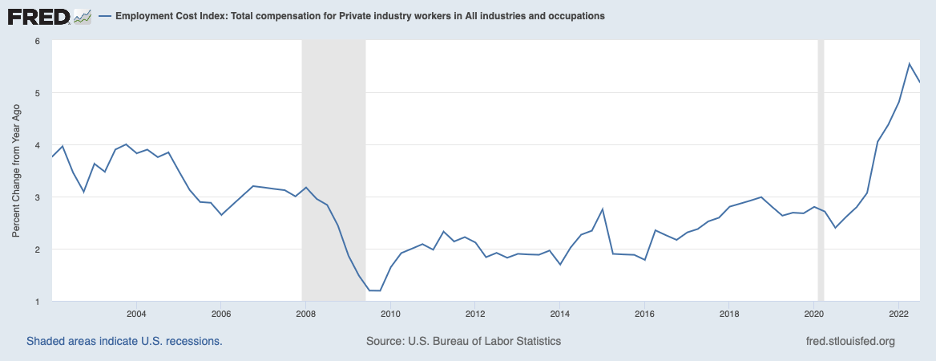

The tight labor market is putting upward pressure on labor compensation, as shown in the next chart. Compensation growth remained above 5 percent in the quarter that ended in September (compensation includes both wages and employer-provided benefits).

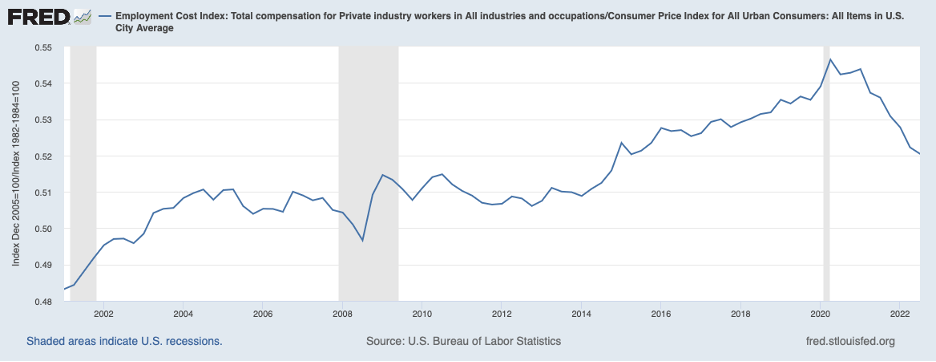

However, the growth in compensation again fell short of consumer prices and real compensation contracted still further, as seen in the following chart.

This measure of real compensation has contracted more than 5 percent since the end of 2020 (note: the units on the vertical axis are simply a ratio of two indexes and have no intrinsic meaning by themselves), after increasing about 1 percent annually over the previous eight years.

This erosion of real compensation is adding to the excess demand in the labor market but cannot be explained by fundamentals: Labor productivity, the key factor affecting real compensation, has essentially been flat since late 2020. No growth in productivity is only a little softer than its usual upward trend of around 1 percent per year. Thus, we can expect the large decline in real compensation to be corrected in the period ahead. The correction should take the form of a pickup in compensation (the other way the correction can occur is by a deceleration in consumer prices, but that is some distance away).

One might ask whether there is a component of income that is benefitting from the erosion of real compensation. As seen in the chart below, the profit share of GDP remained at an all-time high through the second quarter of this year (most recent data, but Q3 corporate earnings reports to date suggest no substantial change in the profit share). Favorable corporate earnings continue to buoy stock prices and underpin household and business spending. The prospective acceleration in compensation can be expected to cut into profits in the future without necessarily adding to inflationary pressure.

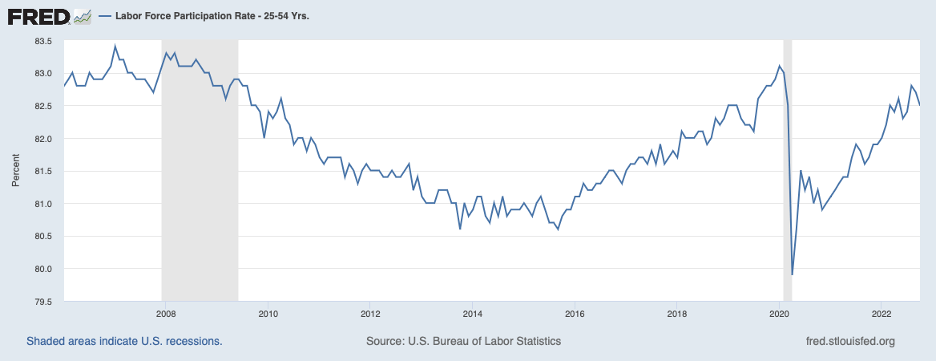

As noted, the Fed recognizes that the labor market remains hot, which is compounding its challenge of bringing inflation down. With the supply of labor not responding much to this disequilibrium, the brunt of the adjustment will likely be in the form of weaker demand. Note in the chart below, showing the labor force participation rate on the part of prime-age workers, that labor supply—the labor force participation rate—has failed to increase over recent months through October.

The necessary weakening of labor demand will occur either from faster growth in compensation than growth in consumer prices, a reversal of the recent decline in real wages and leading to a reduction in the number of workers demanded, or a downward shift in the demand for labor. Labor demand is a derived demand, derived from aggregate demand, and the latter downward shift will come about from a weakening of aggregate demand brought about by a Fed move to restrictive monetary policy.

It is going to take a sizable downward shift in labor demand just to bring the demand for and supply of labor into balance. However, the current momentum in inflation means that there will need to be an excess supply of labor—a recession—to place the underlying inflation rate on a sustainable downward path in line with the Fed’s stated goal of 2 percent inflation. Breaking the back of inflation means that short-term interest rates will need to rise well above the underlying rate of inflation, currently on the order of 5 percent.

Market participants have come closer to this realization over recent weeks, as shown below by the yield on the two-year Treasury note. The yield on the two-year note can be thought of as an average of expected overnight interest rates over the coming two years.

Current expectations are for the Fed to raise its target for the overnight federal funds rate from the present 375 (to 400) basis points to roughly 500 basis points in the first half of 2023. The target is expected to stay around 5 percent until the latter part of 2023 when the Fed is seen to begin backing off.

However, the analysis above suggests that the Fed will not be able to stop at a federal funds rate of 5 percent if it is serious about achieving its 2 percent target for inflation. Moreover, the Fed will need to keep the federal funds rate target high for longer than market participants now contemplate. As the Fed moves to the higher federal funds rate target implied by the analysis above, there will be additional downward pressure on equity and real estate prices and additional upward pressure on the dollar on foreign exchange markets. This tells us that the current era of market volatility still has a ways to go.