The October CPI data released on November 10 were greeted enthusiastically by financial market participants. Not only were the headline and core price increases the smallest in months, but both measures came in well below expectations. Does this mean that the back of consumer price inflation has finally been broken and that the Fed can soon bring its policy tightening to an end?

A closer look at these data points indicates that it is too early to break out the champagne. There are sound reasons to be skeptical at this point. First, monthly CPI data—both headline and core—are inherently very noisy. That is, there is a lot of noise relative to signal in these data, and it takes a few months of data before an underlying change in trend becomes clear. This inherent noise means that we will need to see slower CPI increases for November and December before we can be confident that underlying inflation has slowed.

Contributing to the underlying noise in CPI data is the tendency for many prices in the CPI to change at different frequencies. Some prices, such as fuel prices, change by the day reflecting changes in market fundamentals. Other prices, such as the posted price of a visit to the doctor, change much less frequently and, when they do change, they change by large amounts. Thus, there will be months when there is a disproportionately large number of price increases—a bunching of price increases—that will be followed by a month with a disproportionately small number of price increases. This bunching of price changes compounds the volatility of monthly CPI data.

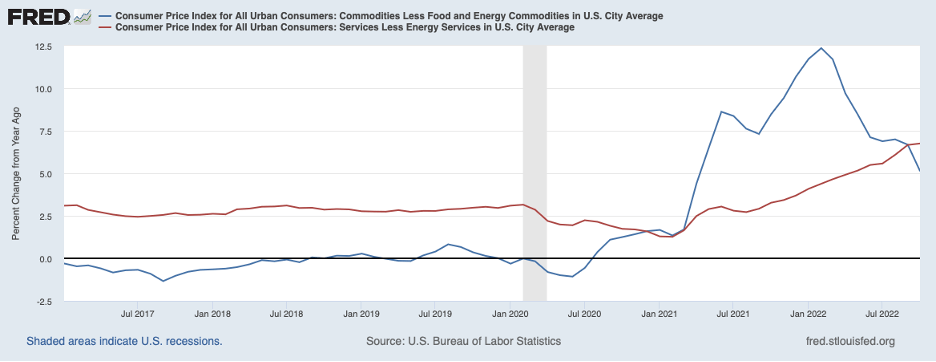

Second, the moderation in the October CPI data occurred in the goods component—as opposed to the services component. This moderation is shown by the blue line in the chart below.

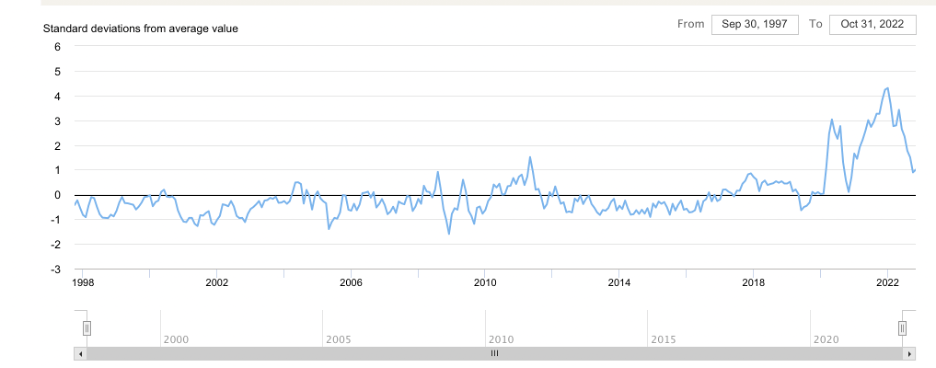

For some time, commodity prices had been boosted by supply-chain disruptions that limited the supply of many goods to consumers, especially those with microchip components. But supply chain pressures have eased a great deal over recent months, as shown by the next chart, and this easing has led to an unwinding of many price increases. These are one-off price changes that are unlikely to persist.

In contrast, service prices have been accelerating, as seen by the red line in the first chart above. The twelve-month change in service prices (excluding energy) reached 6.7 percent, the fastest pace in forty years. Moreover, prices of services increased at a faster pace over the most recent three months than over the previous nine months as seen in the table below. While much of the acceleration in service prices are accounted for by housing costs, the acceleration has been fairly widespread among other service prices.

| CPI Components | ||

| Component | 12-month percent change | 3-month percent change (annualized) |

| Services (less energy) | 6.7 | 7.6 |

| Commodities (less food and energy) | 5.1 | 0.4 |

The pickup in service prices suggests that an underlying momentum is at work in the setting of these prices. A similar underlying momentum in commodity prices may reemerge once the one-off factors that recently have been holding down commodity prices fade.

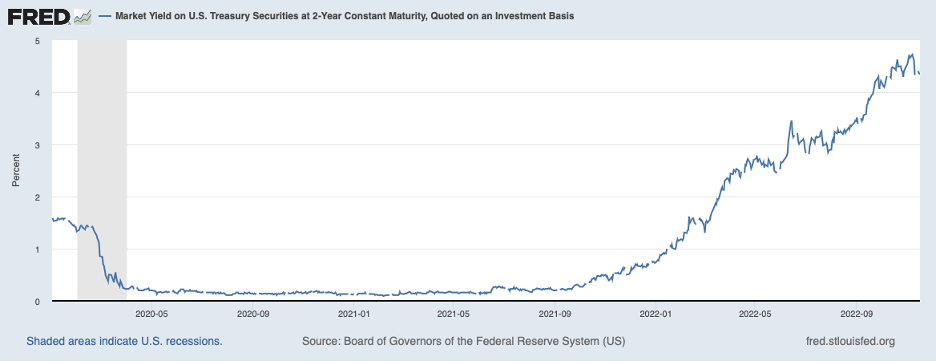

A reemergence of larger increases in commodity prices would call for more aggressive tightening by the Fed than market participants are currently contemplating. The next chart shows the yield on the two-year Treasury note which embodies the expectations of market participants for the average of the Fed’s target for the federal funds rate over the next two years. The chart shows that this rate fell more than 25 basis points after the November 10 release of the CPI to around 4.35 percent. Federal funds futures contracts imply that market participants envision a 50-basis point increase in the Fed’s target for the federal funds rate at its mid-December meeting to 4.25 (to 4.50) percent. This hike is foreseen to be followed by further increases in the target over the first half of 2023 until it reaches the 5 percent area by midyear. By late 2023, the process of lowering the federal funds target is seen to begin.

In sum, recent news on consumer price inflation may be telling us that inflation has topped out and the Fed can slow its pace of tightening. However, a sober interpretation of those data suggests that the deceleration could be a head fake and that stubborn inflation momentum may be revealed in upcoming monthly consumer price reports. If so, market participants will need to revise upwards their expected path for the federal funds rate which will deal another jolt to the stock market and other asset prices.