On September 23, the new prime minister of the United Kingdom, Liz Truss, surprised financial markets by announcing a deficit-expanding fiscal package that included large tax cuts and energy subsidies. This announcement triggered concerns by market participants that Britain may be moving onto a path that would result in it being unable to service its national debt. Turmoil ensued. The stock market plunged nearly 10 percent, as seen in the chart below.

Source: Yahoo Finance

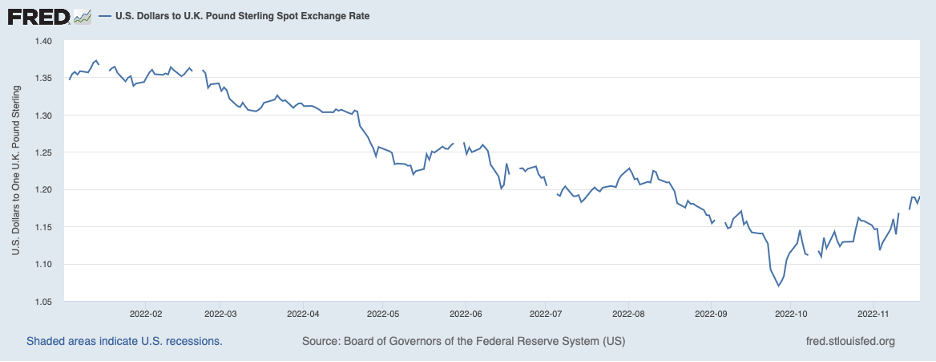

The British pound, which had been sliding since the spring, swooned on the foreign exchange market—shown next.

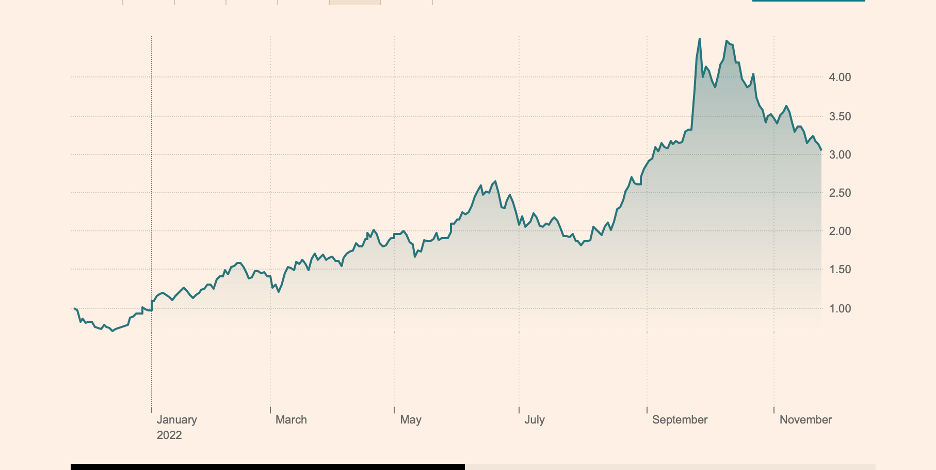

In the market for British gilts (bonds), prices fell and yields soared. The next chart shows that yields rose from around 3 percent to 4-1/2 percent in short order.

Source: Financial Times

Moreover, the increase would have been greater if it had not been for large emergency intervention purchases by the Bank of England. The Bank stepped in to curb the drop in prices and restore stability to that market. Turmoil in the market for gilts was seen to be a threat to financial stability more broadly and to inflict large losses on pension funds.

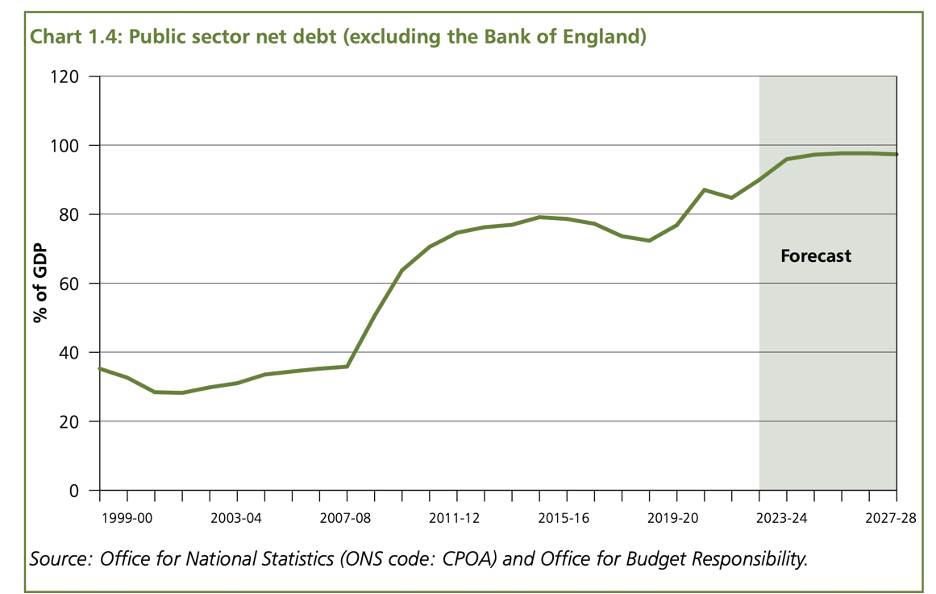

The next chart shows that national government debt in relation to GDP had climbed to about 90 percent around the time of the fiscal announcement, more than double what it had been two decades earlier. Market participants evidently feared that this ratio would continue to rise unchecked and prove to be unsustainable. As a result, servicing this debt (the interest cost) would pose such strains on the government’s budget that default may prove unavoidable—pushing large losses onto bondholders.

In early October, turmoil in financial markets pushed the Truss government into reversing course and rescinding the proposed fiscal package. In other words, the discipline imposed by financial markets forced the British government to return to a more fiscally sustainable policy. Moreover, the political toll of the financial crisis led Prime Minister Truss to resign less than two months after taking office.

After the announcement of a policy reversal, markets recovered, as the charts above illustrate. Under the new government’s budget, the debt-to-GDP is projected to stabilize in the years ahead at nearly 100 percent of GDP, as shown in the chart above. (Note that the ratio of national government debt-to-GDP excludes government debt held by the Bank of England. Including the Bank’s holdings would boost the ratio from 90 to 95 percent.)

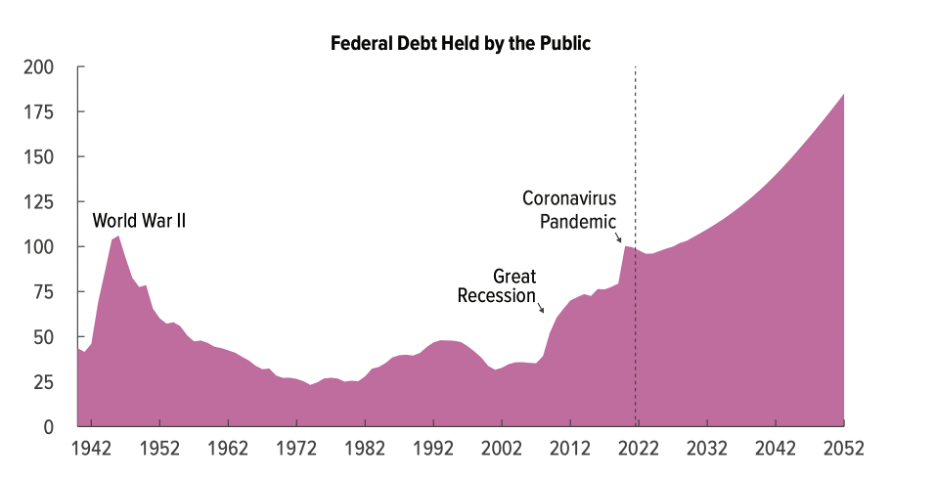

An obvious question coming from the self-inflicted crisis in the United Kingdom is: Are there implications for the United States? The next chart shows the ratio of marketable federal debt to GDP for the United States. (Marketable debt excludes federal debt held by federal trust funds, such as social security, but includes debt held by the Federal Reserve. The Federal Reserve holds about 20 percent of all Treasury debt and the ratio of total debt excluding Federal Reserve holdings is about 97 percent.) At 97 percent, the debt ratio for the United States already exceeds its counterpart for the United Kingdom at 90 percent. Moreover, the Congressional Budget Office (CBO) projects that the debt ratio will nearly double over the next three decades under current laws. Also worth noting is that in a decade this debt ratio will surpass the peak in World War II. Historically, debt-to-GDP has spiked during war times and reversed during times of peace.

Source: Congressional Budget Office

To date, projections of the debt ratio, such as the CBO’s projection shown above, have not led to investor sell-offs as happened when Prime Minister Truss announced her ill-fated fiscal package in September. The lack of market response could owe to skepticism on the part of market participants about whether the path for the debt ratio will be so steep or perhaps investors may not have focused on the issue of debt sustainability yet. However, the UK experience suggests that we may be much closer to an investor revolt than previously had been thought. Any new fiscal initiatives in the United States, such as another large spending program or a big tax cut, may trigger an outsized market reaction, as happened in Britain.

At the end of the day, what will determine the sustainability of the federal debt situation will be prospective fiscal deficits and debt-servicing costs; debt-servicing costs are calibrated as annual interest payments relative to GDP (GDP determines the capacity of the economy to make those payments).

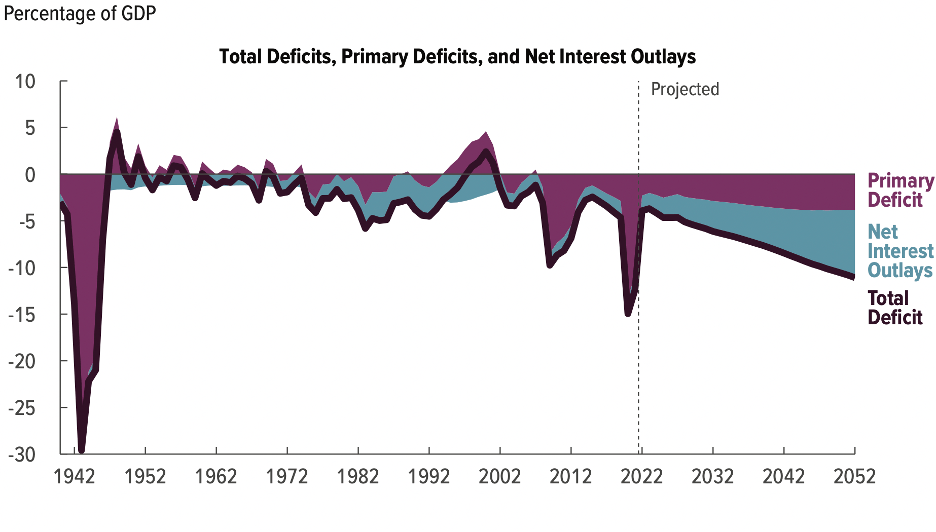

The next chart shows the CBO forecast for the deficit relative to GDP over the next three decades. The total deficit relative to GDP is shown by the black line. The deficit increases from 4 percent of GDP currently to more than 10 percent after three decades (and will continue to increase beyond that point). This increase in the deficit relative to GDP is being driven primarily by rising interest costs, the gray-shaded portion of the chart. The deficit excluding interest payments—the so-called primary deficit, shown by the red shaded area—also increases in relation to GDP, but by less than debt servicing. The primary contributors to the rising primary deficit are health care costs, principally Medicare and Medicaid, which increase at a faster pace than GDP.

Source: Congressional Budget Office

The above chart shows that interest outlays increase from the current 2 percent of GDP to 7 percent over this three-decade forecast period (and continue increasing beyond the forecast period). The increase in interest payments owes to the expanding debt from ongoing (and growing) deficits and also from projected higher interest rates. Currently, annual interest servicing costs are being held down by the extraordinarily low interest rates that have prevailed over the past decade or so. As low-interest debt matures, it is being replaced by higher-interest debt that reflects prevailing (higher) market interest rates. (The Treasury issues new debt to raise the proceeds to pay off maturing debt.) Moreover, CBO forecasts that the level of prevailing market interest rates will be higher over the next three decades than currently—4 percent versus 3.5 percent currently.

The above budget forecast of ever-increasing borrowing to cover ever-increasing deficits is going to be unsustainable. Once market participants come to this conclusion, then interest rates likely will surge higher—as they did in Britain—to compensate creditors for the risk that they are taking on board. Any such surge in interest rates will raise the deficit even more. With deficits increasing from higher interest outlays, a squeeze will be placed on other types of government spending.

The growing fiscal crisis and ensuing widespread financial turbulence will prompt politicians to address the unsustainable budget situation, as took place in the United Kingdom this fall. That is, it will take harsh discipline from financial markets to get the attention of politicians and convince them to respond. In responding to the crisis, politicians will fashion a legislative fix quickly, with little careful deliberation, and the fix will include some abrupt and painful draconian measures. The measures taken will no doubt include a large increase in taxes and curbs on entitlement spending, such as health care and social security. There will also be pressure to cut defense and other federal operating expenses.

To summarize, the British budget crisis of September and early October has important implications for the United States. The British experience tells us that investors in U.S. Treasury debt will at some point become frightened by the U.S. fiscal outlook and will pull back from buying Treasury debt. That point could come sooner than later. When this tipping point is reached, financial turbulence across markets in the United States will be triggered. The turbulence will serve as a wake-up call for politicians to address the budget in a way that satisfies skeptical investors. Absent such a crisis, it is unlikely politicians will address this mounting problem. The sooner investors make that decision to withdraw, the less will be the dislocation imposed on taxpayers, entitlement recipients, and asset holders. The British canary in the coal mine episode of this past fall tells us that we can only hope that our day of reckoning in the United States will come sooner rather than later.