Recent labor market and inflation data and comments from Fed officials have done little to clarify the trajectory of Fed interest rate policy. Indeed, the rift between the views of market participants and Fed officials appears to have widened. Market participants read the consumer price data for November, released at the time of the Fed’s December FOMC meeting, to imply that the Fed’s job of tightening policy to bring inflation under control does not have much farther to go. In contrast, Fed officials have read those consumer price data differently.

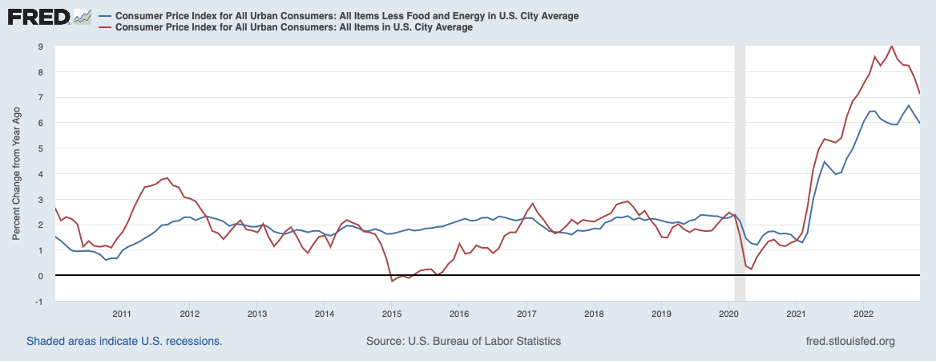

Market participants seemed to focus on further deceleration in the headline CPI to 7.1 percent in November on a twelve-month basis, red line in the chart below, down more than a percentage point since the peak in August. Meanwhile, core inflation, shown by the blue line, slowed to 6.0 percent, down only marginally from the peak in September. The core measure of inflation is thought by the Fed to be a more reliable gauge of underlying inflation, and at 6 percent, is three times faster than the Fed’s target of 2 percent. (The Fed’s target is expressed in terms of the Personal Consumption Expenditures—PCE—index which runs slower than the CPI; the core PCE rose 4.7 percent over the twelve months ending in November.)

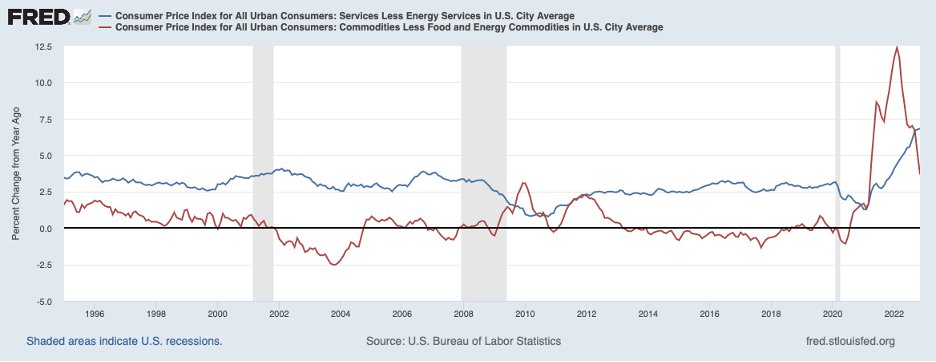

Digging a little deeper, deceleration in the CPI has been most evident in commodity prices. The red line in the chart below shows the twelve-month change in the prices of commodities (excluding volatile food and energy commodity prices), which have slowed from 12.4 percent in February to 3.7 percent in November. Supply chain disruptions had been boosting commodity prices, but these disruptions have been reversed to a great extent since earlier in the year. That reversal of supply chain disruptions has placed temporary downward pressure on commodity prices. How much longer the easing of supply constraints will be putting downward pressure on commodity prices is unknown at this point.

In contrast to prices of goods, service prices have been on an upward march for a time, the blue line in the chart above. Service prices rose 6.8 percent in October and November, up about 3.5 percentage points from a year earlier.

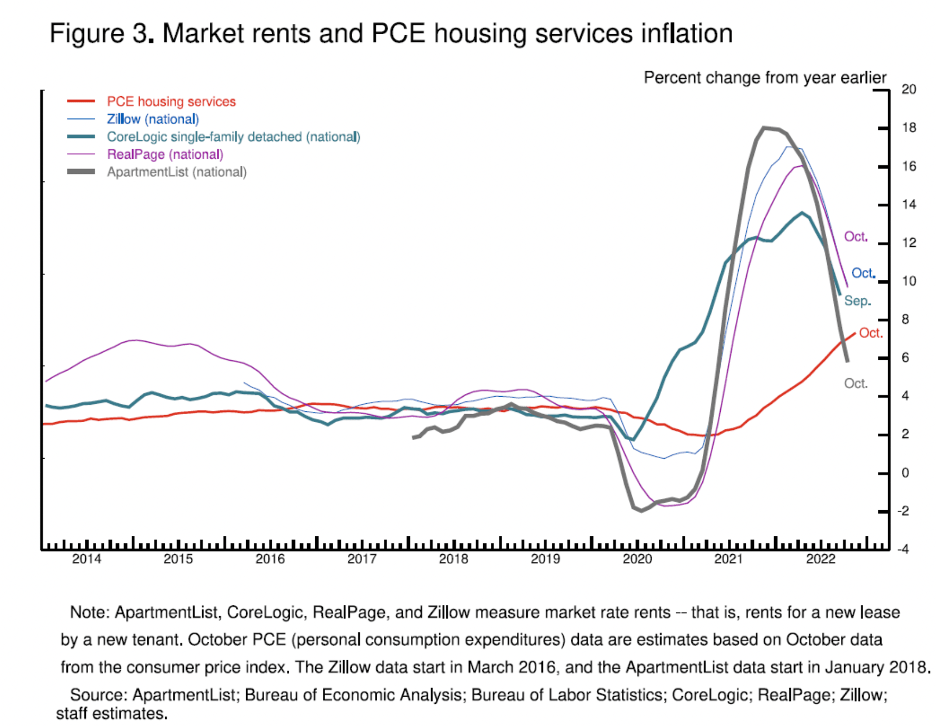

Contributing to the acceleration in service prices has been a run-up in its component that measures rental of housing. Rental of housing represents more than 30 percent of the CPI and consists of actual rents paid on properties rented and an estimate of what homeowners pay when they rent to themselves—called owners-equivalent rent (OER). Actual rent and OER tend to move closely together. Based on the methodology used in constructing the rent component of the CPI, there is a built-in lag between actual rent changes and their appearance in the CPI. The entries for rent are based on a survey of rents that is conducted semiannually. The readings for the months between surveys are interpolated. Thus, a change in the trend of rents will be captured with a lag.

This lag in rents can be seen in the chart below which contains various estimates of the monthly percent change in actual rental rates—lines colored other than red—and the housing services component of the PCE index, shown in red. The various measures of rents peaked earlier this year from a surge in 2021, but the rental component of the PCE index continued accelerating over this time because of the lag. This chart suggests that the rental component of the PCE and CPI will be decelerating in a few months and this deceleration will hold down increases in overall CPI and PCE price indexes.

- Source, speech by Jerome H. Powell, “Inflation and the Labor Market,” speech given on November 30, 2022. Board of Governors of the Federal Reserve System.

Prices of services other than housing have also picked up recently, rising at an elevated 4-1/2 to 5 percent pace over recent months, and have not shown signs of slowing. Services other than housing account for roughly the same portion of household budgets as housing, and thus recent persistence of outsized increases in this component raises concerns about imminent prospects for slowing.

The Fed has taken a somewhat skeptical view on whether the recent news on consumer prices suggests that it can start taking its foot off the brakes. Indeed, the Fed foresees that the target for the federal funds rate will be raised to 5.1 percent by the end of 2023, from roughly 4.4 percent currently, and then will be lowered to 4.1 percent by the end of 2024 and 3.1 percent by the end of 2025. Judging from federal funds futures, market participants foresee the federal funds rate peaking at 4.9 percent before mid-2023 and the Fed beginning to ease rates by the end of next year.

The Fed sees more persistence in the inflation process that will require that the federal funds rate rise above 5 percent in 2023 and remain there for longer than market participants envision. Evidently, the Fed is giving more emphasis in its thinking to the momentum in non-rent service prices and foresees some pickup in commodity prices once the easing of supply chain pressures comes to an end. Moreover, the Fed seems to attach significance to recent labor market data that point to a still large overhang of demand over supply. This imbalance will need to be corrected, presumably by labor demand falling sharply as a result of the effects of the Fed’s restrictive monetary policy on household and business spending, before a foundation is re-established for price stability. Already, the housing sector has weakened considerably from higher interest rates, and it appears that consumer spending is in the process of slowing, too. Also, the Fed has expressed its intention to err on the side of restraint to better ensure that it has placed inflation on a firm downward path to 2 percent. The Fed is of the view that easing prematurely would require a messy reversal of policy direction and undermine its credibility.

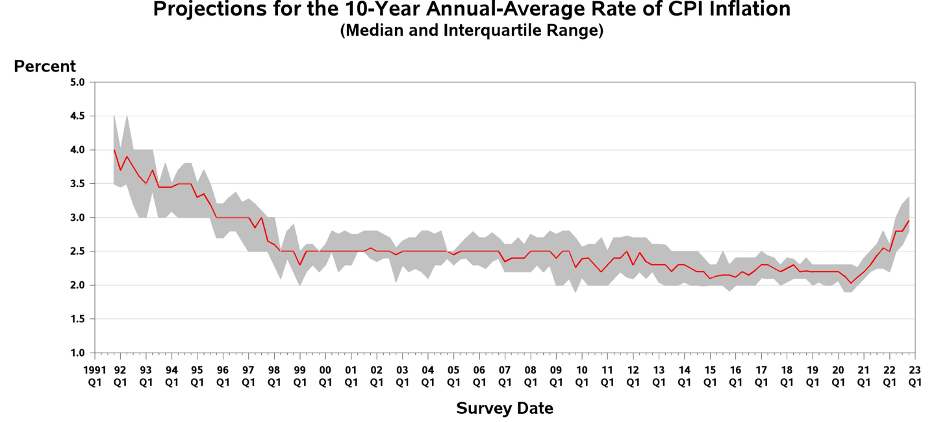

Previous experience with efforts to bring down high inflation clearly indicates that there is a persistence factor in the inflation process once inflation has passed a threshold and that momentum factor is hard to overcome. Breaking that momentum will require that interest rates rise above the underlying rate of inflation and stay there for a time. Looking at present circumstances, this reasoning implies that the federal funds rate will need to be raised to a good bit above 5 percent and remain there for a while before we will see inflation on a distinctly downward trajectory. Professional forecasters point to a tough battle ahead for the Fed regarding long-run inflation expectations, shown in the chart below. These forecasters have been raising long-term inflation forecasts for more than a year and now see the long-run inflation outlook to be higher than any period since the late 1990s.

To sum up, a division continues between market participants and the Fed regarding how much additional tightening by the Fed will be required to bring inflation down. Market participants have read recent inflation data to mean that the peak in interest rates is near. The Fed, on the other hand, has taken the view that recent inflation numbers have been held down to a degree by temporary one-off factors. The Fed also sees that the labor market remains hot and there will need to be more distinct signs of cooling before the labor market is consistent with the 2 percent target for inflation. However, the momentum factor built into the current inflation process and the need for slack to develop in the labor market is not being fully captured by either group. Achieving the Fed’s goal for inflation will require that the federal funds target be raised well above 5 percent, beyond what both market participants and the Fed currently envision. Once this path for the federal funds rate becomes clearer to market participants, mortgage interest rates will resume increasing and the stock market will drop further. The additional rise in mortgage rates and decline in stock prices is all part of the adjustment required for the Fed to achieve its 2 percent inflation target.