The Fed’s fight against inflation proceeded through 2022. During the year, the Fed raised its target for the federal funds rate seven times, lifting the target from 0 percent to 4.25 percent (these interest rates are at the lower ends of a ¼ percent range). In its most recent projections in mid-December, the Fed projected that it will boost the federal funds rate target by another ¾ percent over 2023 to 5 percent. At the same time, the Fed reaffirmed that it would be letting its holdings of Treasury and mortgage-backed securities run off its balance sheet, implying that the supply of these assets that must be absorbed by the public will continue to grow.

To place the current situation in context, with the onset of COVID in March 2020, aggregate demand and aggregate supply collapsed. Households and businesses slashed their spending amid exceptional uncertainty about the job market and business sales—depressing demand—while the lockdown and COVID fears led to a sharp reduction in hours worked and production—depressing supply. In response, the Fed cut its target for the federal funds rate to 0 percent. The Fed also embarked on a massive asset purchase program that boosted its holdings of assets from $4 trillion in early 2020 to $9 trillion two years later. As the Fed swung to an unprecedented expansionary policy, outsized fiscal measures were enacted to cushion the effects of COVID on households and businesses. These fiscal actions were followed by additional massive spending measures, including for so-called infrastructure.

In short order, aggregate demand snapped back, aided by the highly expansionary monetary and fiscal measures. However, aggregate supply recovered more sluggishly. COVID fears, coupled with generous federal and state transfer payments, contributed to a muted recovery in labor force participation and supply-chain disruptions further limited the rebound in supply. The end result was a considerable excess of demand over supply and an upturn in inflation.

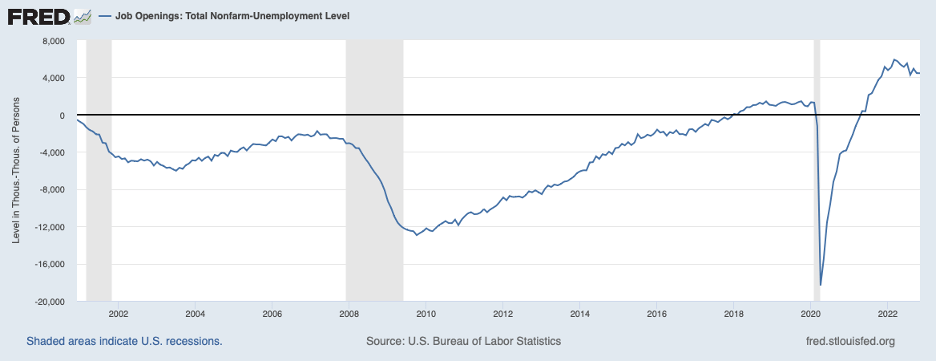

This excess of demand over supply was also reflected in the labor market. The chart below shows the excess of job openings over the number of unemployed persons, which became pronounced in early 2022 and remained so over the remainder of the year (up to November, most recent job openings data).

Excess demand for labor is putting upward pressure on wages. Shown next are the average hourly earnings of goods-producing workers (red line) and service-producing workers (blue line) relative to their pre-pandemic levels (through December 2022). Wages for both groups are up appreciably, with service worker wages outpacing wages of workers in the goods sector reflecting more pronounced tautness in the service sector.

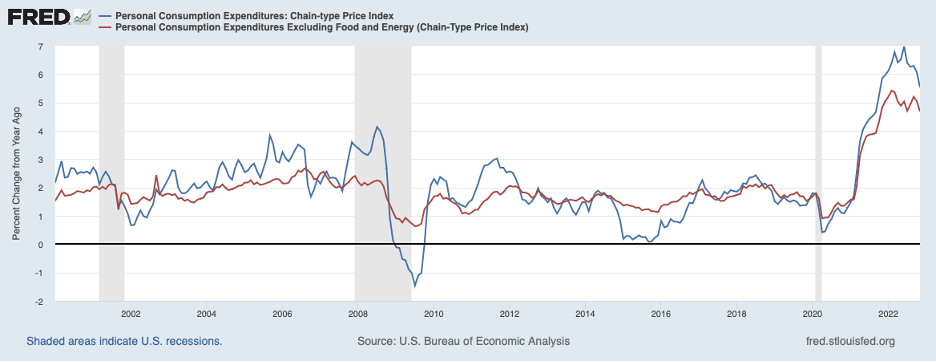

Turning to consumer prices, the chart below shows the Personal Consumption Expenditures (PCE) index for headline inflation (blue line) and core inflation (headline inflation excluding volatile food and energy prices, red line). Core inflation has slowed much less than headline inflation since the peak last spring, staying around 5 percent.

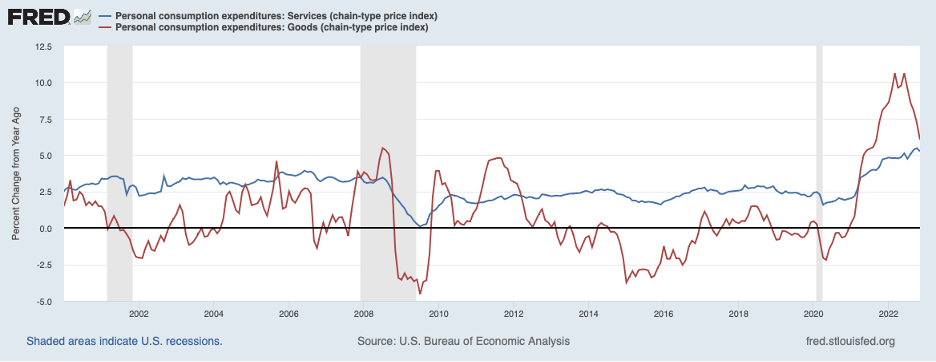

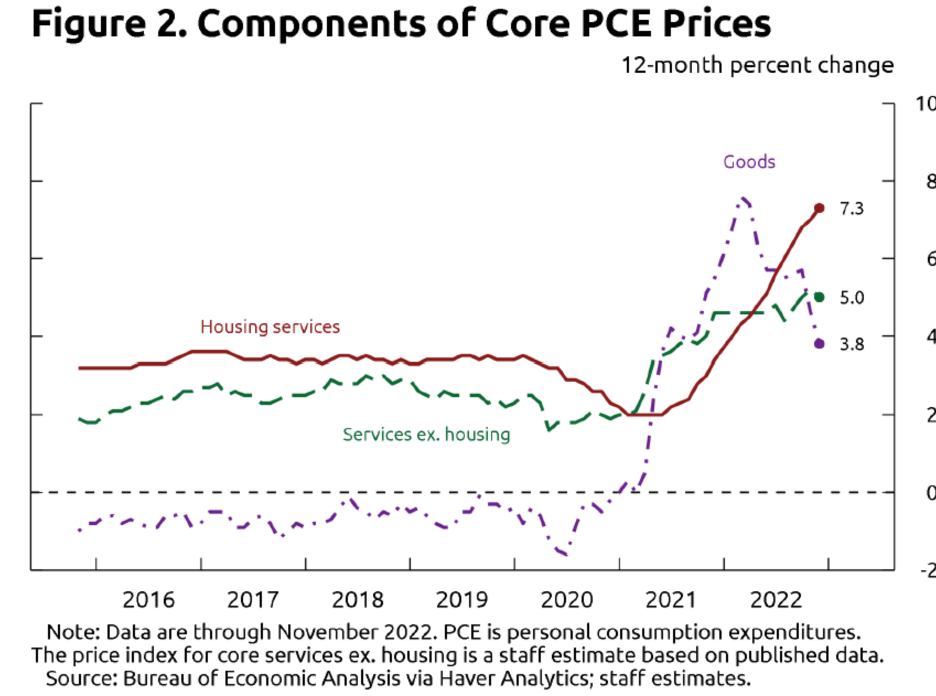

Digging more deeply, goods price inflation, the red line in the next chart, has moderated considerably while service price inflation, the blue line, appears to have stabilized in recent months around an elevated 5 percent rate.

A good portion of the deceleration of goods prices owes to an easing of supply chain disruptions, shown in the next chart. The Global Supply Chain Pressure Index has in recent months retraced the bulk of its run-up over 2020 and 2021. This is a one-off impact on goods prices, unlikely to persist much longer. Once supply chain pressures return fully to normal levels, goods price inflation can be expected to firm up.

Source: Global Supply Chain Pressure Index, Federal Reserve Bank of New York.

Contributing to the increase in service prices have been both housing costs (rent and owners’ equivalent rent), shown by the red line in the next chart, and prices of other services, shown by the green line. There are good reasons to expect that the housing cost component of service prices will slow in the months ahead (see December 24, 2022 post, “The Inflation Battle: Is the Fed Close to the Finish Line?“). But there is less reason to expect a moderation in the prices of services other than housing.

Source: Speech by Governor Lisa Cook, “Thoughts on Inflation in a Supply-Constrained Economy,” January 6, 2023, Board of Governors of the Federal Reserve System.

Indeed, the increase in prices of services other than housing appears to be representative of the underlying rate of inflation—roughly 5 percent. This rate of inflation is likely to persist while some of the temporary forces affecting the prices of goods and housing services are working themselves out. Previous experience with high inflation indicates that inflation becomes stubborn in these circumstances and is hard to bring down.

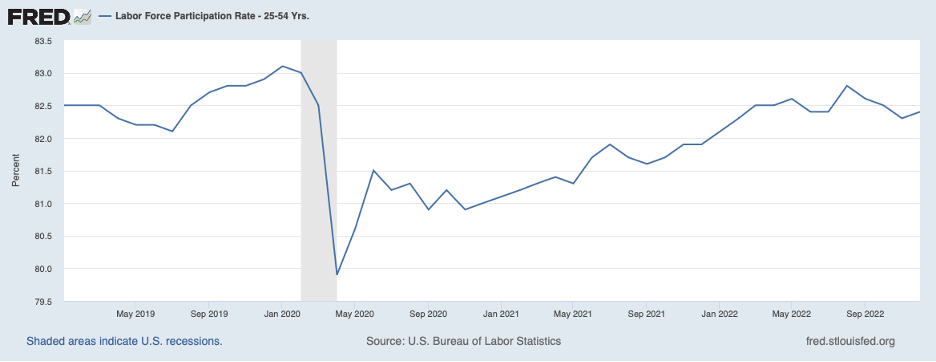

Looking ahead, it is unlikely that inflation relief will come from the supply side. Notably, many workers have decided to sit on the sidelines and not return to the workforce. The next chart shows that the participation rate on the part of prime-age workers recovered partially in the first two years of the pandemic but has since leveled off at a rate well below the pre-pandemic level.

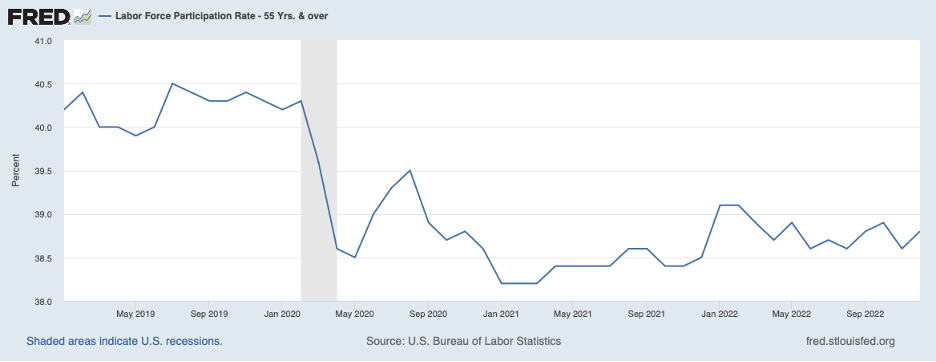

Moreover, participation on the part of older workers, next chart, has shown few signs of recovery at all in the wake of the pandemic. No doubt the provision of more generous transfer payments since the onset of COVID has discouraged job-seeking on the part of workers across the age spectrum.

With aggregate supply constrained, the task of removing excess demand in the market for goods and services—and, also in the labor market—will fall on aggregate demand. In other words, more monetary restraint will be needed. While the monetary restraint put in place already has weakened interest-sensitive sectors of the economy, most notably housing, demand overall appears to have forged ahead through the end of 2022.

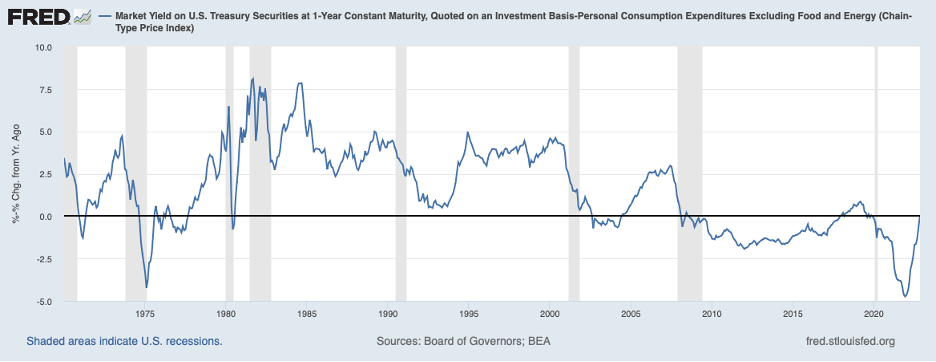

The next chart shows the real one-year Treasury yield—the nominal one-year yield less the underlying rate of inflation (core PCE inflation). The real yield over the past year has gone from being deeply negative to zero, meaning that the amount of monetary stimulus coming from the Fed has been reduced substantially. (Note that the one-year Treasury yield embodies market expectations for the federal funds rate over the next year; currently, market participants envision that the Fed will raise the federal funds rate by ½ percent or so over the first half of 2023 and then begin to reverse these increases later in the year.) Nonetheless, at a real interest rate of zero, the Fed is still providing monetary stimulus. The level of the real interest rate that is associated with neither monetary stimulus nor restraint—the so-called neutral rate—is on the order of ½ to 1 percent.

Thus, short-term interest rates will need to increase more than ½ percent to be stimulative no longer. But an increase of this amount will not be sufficient to place underlying inflation on a downward path. Because of the momentum in current underlying inflation, the real interest rate will need to be sufficiently restrictive—well above the neutral rate—to create slack in the economy. In other words, short-term interest rates will need to rise appreciably from current levels to cause a shift from excess demand to excess supply (and, with it, a recession). And the stronger is inflation momentum, the higher short-term rates will need to rise or the longer rates will need to remain high. (Note that this measure of the real rate was 5 percent or higher during the fight against inflation in the late 1970s and early 1990s, a time when the inflation problem was more severe than now.) In these circumstances, longer-term interest rates will need to increase from current levels, the stock market will need to fall further, and the dollar will need to remain firm.