At its May 3 meeting, the Federal Reserve (Fed) raised the target for the federal funds rate ¼ percent and signaled that it would be watching incoming data to determine whether any further increases would be needed to place inflation on a downward trajectory toward the Fed’s 2 percent target.

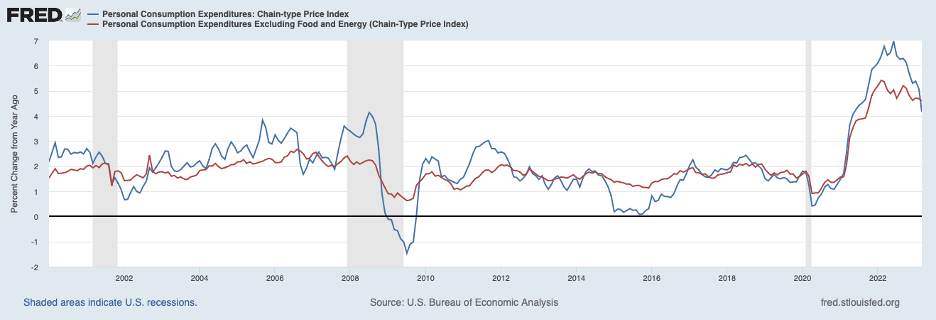

As shown in the chart below, inflation remained elevated through March (most recent data), especially core PCE inflation (the red line). Core inflation, a better indicator of underlying inflation than headline inflation (the blue line), has not slowed much and has stayed above a 4-1/2 percent rate through March — well above the Fed’s 2 percent target.

Chair Powell, in his press conference following the May 3 meeting, mentioned that he expected that the federal funds rate would need to stay high for some time before inflation eased enough for the Fed to be comfortable lowering rates. Nonetheless, financial market participants took Fed commentary to suggest that Fed tightening had come to an end and even priced in an easing of Fed policy by September.

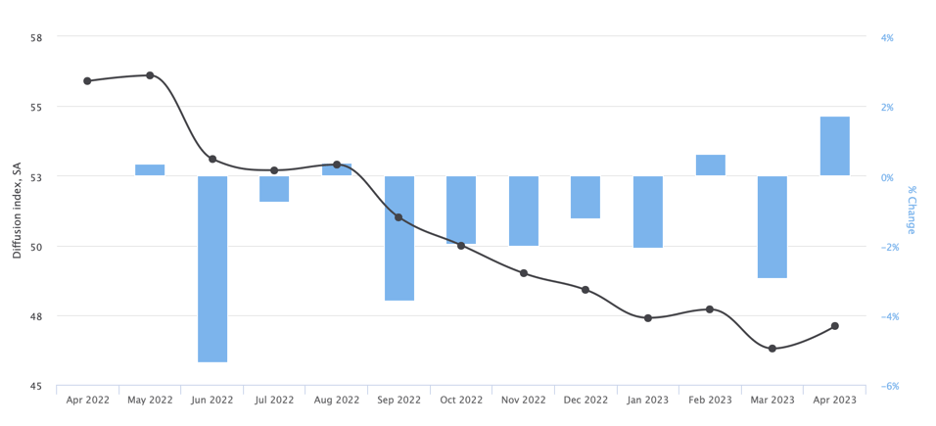

Market participants seem to be basing their outlook for Fed policy on a view that the economy is weakening and that the banking shock that hit in early March would cause further weakness as banks responded by tightening appreciably their provision of credit to businesses and households. The views of market participants were shaped to a degree by ongoing reports of weakening in the manufacturing sector as shown by the PMI index of the Institute of Supply Management, shown below. The index dropped below 50 — the level that represents no expansion or contraction in manufacturing — last September and has remained in contractionary territory since that time.

Purchasing Managers’ Index (PMI)

Source: Institute for Supply Management and Moody’s Analytics.

Moreover, GDP data for the first quarter of this year, showing that output expanded at only a 1.1 percent annual rate following a nearly 3 percent rate of expansion in the second half of 2022, were viewed as confirming that economic activity was softening. Notably, business investment flattened out in the first quarter, which was viewed to be an indication that Fed tightening measures over the past year were clearly taking hold.

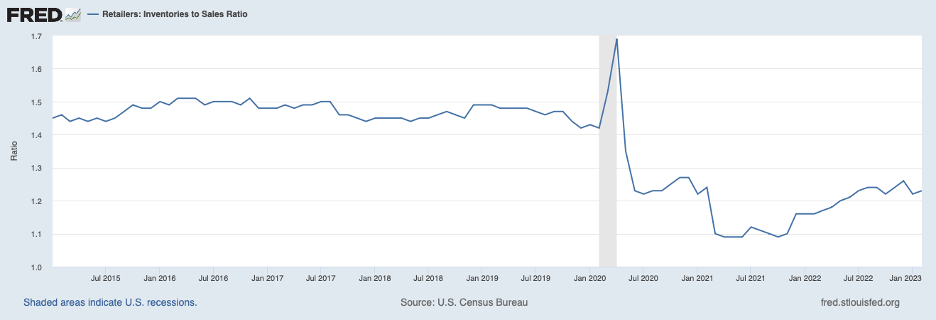

To assess the underlying strength of the economy going forward, it is noteworthy that growth in consumer spending and federal outlays for goods and services were robust in the first quarter. Contributing to the slowdown in real GDP growth was a drawdown of business inventories that shaved more than 2 percentage points off output growth. Looking ahead, inventories remain low in relation to sales at the retail level, shown in the next chart. Also, manufacturers of capital goods still have a sizable backlog of unfilled orders to keep their production levels up. As a consequence, it seems unlikely that the drag on GDP growth coming from inventories will persist while consumer and federal spending continues to propel the economy forward.

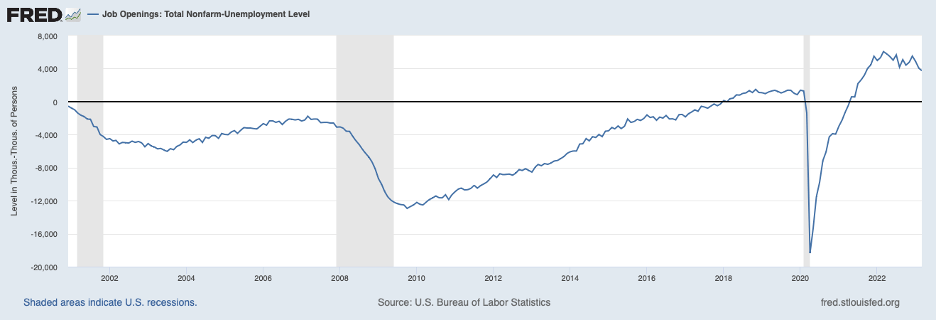

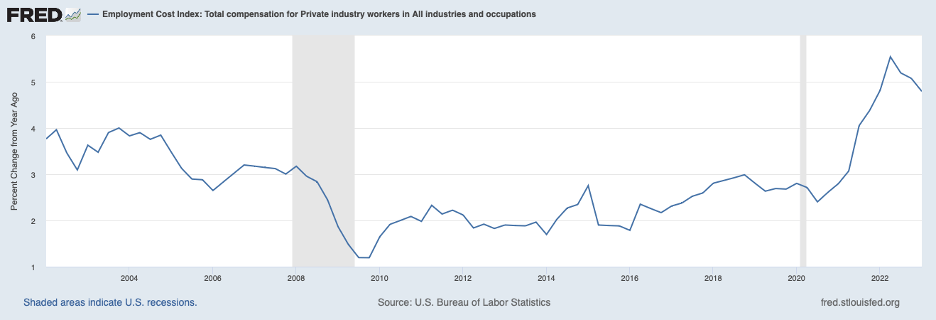

Turning to the labor market, the excess of labor demand over supply remained substantial through March (most recent data), as suggested by the chart below showing job openings less the number of unemployed persons. While the excess of job openings has shrunk a bit this year, the margin remains very large and is placing upward pressure on labor costs as illustrated in the next chart showing the growth of labor compensation for private sector workers. Growth in compensation remains roughly 2 percentage points above the pace before the COVID shock — a time when inflation was under control. Moreover, labor market data for April indicate that conditions in the labor market have not cooled much recently.

A considerable slowing in economic activity will be needed to erase the imbalance between labor demand and supply and slow growth in labor costs enough to return inflation to a 2 percent rate. Indeed, a recession likely will be necessary to create enough slack in the economy and the labor market for underlying inflation to be moved onto a downward path to 2 percent.

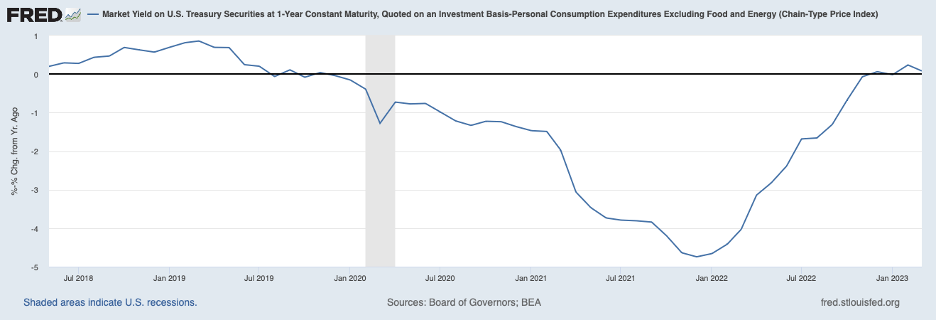

The Fed’s May 3 action raised the federal funds rate to 5 percent (actually, to a 5 to 5-1/4 percent range), 5 percentage points above the level fourteen months ago. Nonetheless, real short-term interest rates are barely positive, shown next, and remain below the level that will be required to break the back of inflation. The chart is based on the one-year Treasury yield less the twelve-month percent change in core PCE inflation through March. (The one-year Treasury yield in March reflected the expectation that the Fed would raise its target ¼ percent in early May —which the Fed did — but not anymore after that move and thus the March reading of the real short-term rate is reasonably reflective of the current level.) To restrain the economy sufficiently to turn underlying inflation lower will require further increases in the federal funds rate — likely a full percentage point or even more.

The recent disturbance in the banking system is expected to lead to more caution on the part of banks in providing credit to businesses and households. Restraint by banks will take the form of being more selective in whom they are willing to lend; cutting back on the amounts that they are willing to lend (including credit lines); and raising the rate that they charge (relative to the federal funds rate). The Fed sees these reactions by banks to be reducing the extent to which it will need to tighten to bring inflation under control. In other words, the more restrictive credit stance by banks is doing some of the Fed’s tightening work.

At issue is the extent to which banks are restricting the availability of credit in response to the banking disturbances. Banks typically become more cautious lenders during the tightening phase of an interest rate cycle. As noted in a recent posting (Recent Banking Disturbances and Implications for Fed Policy: What You Need to Know, April 15, 2023), the Fed’s quarterly survey of large banks showed that these banks had become more restrictive lenders before the onset of the banking disturbance in March, in keeping with previous periods of monetary restraint and captured by standard rules of thumb for monetary policy. In judging the extent to which the recent disturbance is affecting credit, the Fed has had the benefit of an update to that survey in early May and no doubt has touched base with regional banks which have been the epicenter of recent banking disturbances.

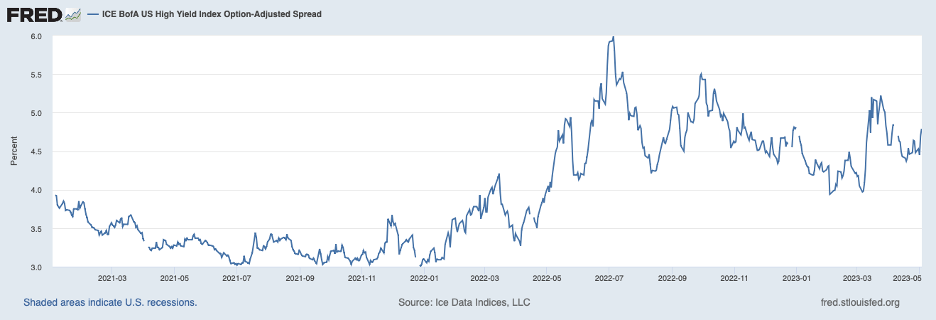

At this point, it is not clear that the banking disturbances have had a substantial separate impact on credit conditions. One rough indicator is the spread on below-investment-grade bonds, shown below. This measure of credit risk jumped higher when the banking disturbance hit in early March of this year but not to levels that emerged once the Fed began tightening in the spring of 2022. Moreover, it has since retraced much of the recent increase.

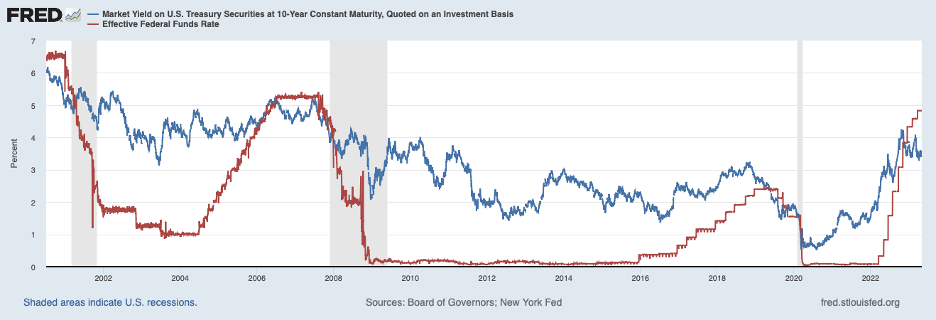

Any assessment of the impact of the banking disturbance should be balanced by the extent to which interest rates on longer-term benchmark securities that serve as a basis for pricing many types of credit to businesses and households are being held down by ongoing perceptions by market participants that the Fed is closer to the end of policy tightening than has been the case. The result has been less restraint coming from longer-term credit markets than would be occurring if market participants had throughout the past year understood the amount of monetary restraint needed to return inflation to the Fed’s 2 percent target. Shown below is the yield on the Treasury ten-year note (blue line). This yield currently is above pre-COVID levels but not as much as the current battle against inflation would suggest.

The increase in longer-term interest rates over the past year as the Fed has been raising the target for the federal funds rate (red line) has been affecting asset values on the balance sheets of banks. This is especially true for banks—such as Silicon Valley Bank—that loaded up on longer-term securities (Treasury and mortgage-backed securities) when short-term rates were at rock bottom in an attempt to get better near-term earnings (exploiting the difference between the blue and red lines in the chart above). However, the risks of such a strategy were exposed when the value of longer-term securities fell as rates rose and these banks had to realize losses when depositors with large uninsured balances fled. Going forward, other banks with heavy concentrations of uninsured deposits and longer-term assets are going to be facing strains that will be restricting their lending. However, the vacuum caused by these banks will provide opportunities for other banks with more comfortably positioned balance sheets. Moreover, it appears that there are not enough remaining vulnerable banks to prompt a serious widespread banking crisis in the period ahead.

In sum, despite the wake-up call prompted by the problems of some large regional banks, the Fed still has more tightening to do to put inflation on a distinct downward path toward 2 percent. Pausing rate hikes at this time would send the wrong message to market participants and likely would lead to a rally in financial markets that would offset some of the restraints currently in place. The reality is that inflation is more stubborn than many want to believe and bringing inflation steadily down will require more tightening and continued resolve by the Fed.

Thanks for this blog. Sounds like recession will be necessary to lower inflation to 2%.

LikeLike