On August 27, Fed Chair Jerome Powell announced an important change to the Fed’s conduct of monetary policy. The announcement followed a lengthy and thorough review of the Fed’s policy framework and its strategy for achieving its statutory goals of maximum employment and stable prices. The review was prompted by significant changes in the economic and financial landscape over recent decades, and, interestingly, by the Fed’s success in holding inflation low. The announcement had a dramatic effect, catching the attention of financial markets and analysts and giving the stock market another boost. Some hailed it as “landmark.”

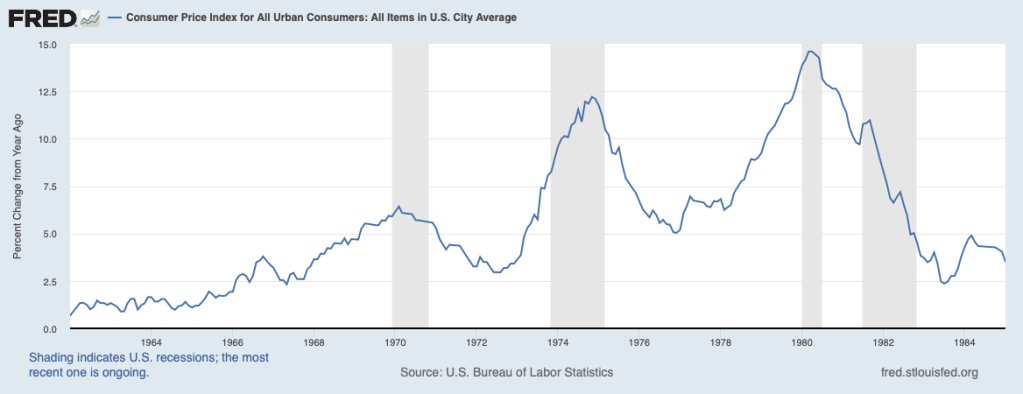

What was that announcement and what does it mean? To appreciate the need for this change, we should go back a half-century. In the early 1970s, the United States dissolved the last link to the gold standard and thereby removed this disciplinary force holding inflation down. The decade of the 1970s that followed was a period in which inflation moved from the 5 percent area to nearly 15 percent, as shown in the chart below. Inflation had started to build in the second half of the 1960s and then intensified, on balance, over the 1970s.

Inflation had pervasive and corrosive effects on the economy, and, by the end of the decade, it was considered by the public to be the most serious problem facing the nation—even eclipsing nuclear confrontation with the Soviet Union. A growing segment of the economics profession came to believe that a stable price level or low inflation was needed for optimal economic performance and that a new way to anchor prices was needed. They (we) also thought that absent an effective method for anchoring prices, there would be an upward bias in inflation—monetary policymakers would have more of an incentive to overstimulate the economy at a time of weakness than to restrain the economy in the face of inflation.

At the end of the decade, the Fed, under the bold leadership of Chairman Paul Volcker, embarked on an aggressive effort to bring inflation down. It succeeded, as shown in the chart above. The economic cost of doing so, though, was substantial—in large part because the public had become highly skeptical that inflation would stay low. Inflation expectations had become stubbornly high and it took time for them to move lower and match the actual drop in inflation. Nonetheless, this policy paved the way for a long period of prosperity. The Fed had relied on its control over the money stock as a new anchor on prices to achieve this result. However, insurmountable problems developed in using the money stock as an anchor, and the Fed began to look for other methods of conducting monetary policy. Despite these challenges, the Fed’s effort to keep inflation low under both Paul Volcker and Alan Greenspan worked.

While the Fed was working on a new framework for conducting monetary policy, a consensus within the Fed emerged for pursuing an “opportunistic” strategy to bring inflation to a desirable level: The Fed would use the tools at its disposal to actively resist an upturn in inflation but would rely on inevitable recessions to bring down inflation and lock in lower inflation rates. There was an underlying sense among policymakers that they needed to be vigilant to avoid overstimulating the economy and build on the credibility that they were garnering in holding inflation low. That meant moving promptly to raise interest rates when indicators were pointing to an overheating economy.

Meanwhile, the Fed, in keeping with other major central banks, adopted and announced publicly a specific target for inflation. This was to become the new anchor on prices. In 2012, it specified a target of a 2 percent annual increase in the Personal Consumption Expenditures Index of Prices. Policymakers thought that, in light of the success that they were having in keeping inflation low, this would firm the public’s expectations of inflation around 2 percent. And, by so doing, that would provide the Fed more scope for countering weakness in the economy without having to fear that the public would misinterpret its actions to be an effort to overstimulate the economy with an accompanying willingness to tolerate more inflation.

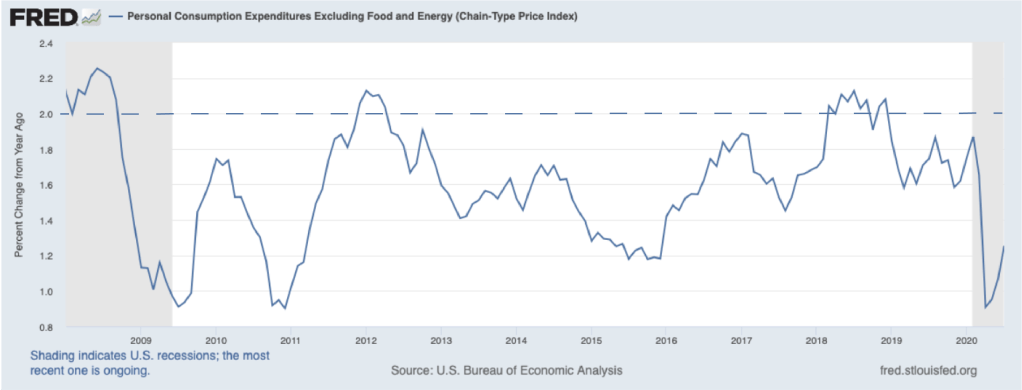

In practice, inflation has, with few exceptions, run below the Fed’s 2 percent target over the past decade, as shown in the next chart. Indeed, it dropped sharply recently in response to the COVID shock (see June 13, 2020 post, Any Signs of Inflation Yet?). As a result of the shortfalls from 2 percent, it appears that the public’s expectations of inflation have been edging lower. In essence, the public seems to have come to the view that shortfalls in inflation will be forgiven by the Fed and not made up later. As expectations of inflation have moved lower, the Fed’s task of stabilizing the economy and maintaining high levels of employment has been complicated.

To appreciate why this has become a serious concern of the Fed, keep in mind that inflation expectations are an important component of the underlying level of interest rates. And, as inflation expectations decline, the underlying level of interest rates declines one-for-one. This decline reduces the room for the Fed to lower its policy interest rate (the federal funds rate) to counteract a negative shock to the economy, such as COVID.

Also limiting the scope to lower interest rates in response to a negative shock has been the other component of the underlying level of interest rates—the real interest rate (see July 13, 2020 post, Buoying the Market: An Era of Ultra-Low Interest Rates). The next chart has three different approaches to estimating the so-called neutral real federal funds rate and all three illustrate that the underlying real interest rate has fallen markedly over the past two decades, from the 3 percent area to 1 percent or below.

All of this means that the Fed has lost a lot of headroom to lower interest rates when it faces weakness in the economy. As a consequence, it sees a greater need to move quickly and aggressively to lower its policy rate when the risk of economic weakness (and employment shortfalls) grows than the need to raise that rate when the risk of an unsustainably strong economy grows. Furthermore, the Fed has had considerable experience over recent years with employment surpassing maximum sustainable levels and no outbreak of inflation (a so-called flatter Phillips curve). Consequently, the Fed has now become comfortable stating that it is willing to tolerate sustained periods of the U.S. economy running strong. And it no longer fears that efforts to stimulate the economy when there are shortfalls in employment will trigger self-fulling expectations of accelerating prices. The current anchor on prices seems to be pretty strong as other anchors had been in much earlier times.

This brings us to the Fed’s announcement of August 27. The new statement says that the Fed is seeking 2 percent inflation over time. This means that future shortfalls of inflation from 2 percent will be made up and no longer forgiven. The make-up will likely require that the economy and employment run unsustainably strong for a period to allow inflation to rise above 2 percent until the make-up has been accomplished. It is hoped that inflation expectations will become more firmly entrenched around 2 percent—and not drift below. This, in turn, will give the Fed a higher starting point for interest rates and more room to lower the policy interest rate when weakness in the economy and shortfalls in employment emerge. And when they hit bottom at zero, they will utilize large scale asset purchases and forward guidance commitments to keep interest rates low to augment their low interest -rate policy (see May 5, 2020 post, Are We Drowning in Fed Liquidity?). From public statements in recent years, the Fed’s August 27 statement codifies the evolution of thinking within the Fed in response to the new era of low inflation and low interest rates and seeks to convince the public that it has the tools and determination to keep inflation close to 2 percent—not at all times, but on average over time. For more on the role of public policy in a market economy, see Chapter 2 of my new book, Capitalism Versus Socialism: What Does the Bible Have to Say?