Initial claims for unemployment insurance jump and universities shut down campuses and return to all on-line classes—news pointing to a setback for the economy. In contrast, existing home sales surge and the stock market moves into record territory—news pointing to an ongoing rebound from one of the sharpest declines in history. What does it all mean?

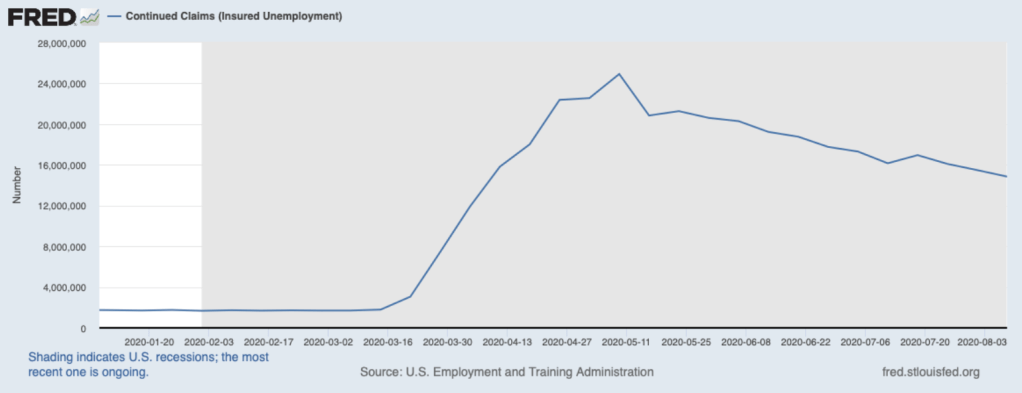

While new unemployment insurance claims have, on balance, been unchanged over recent weeks, continuing claims (all who are collecting unemployment benefits) have been on a fairly steady downward march, as shown below. This means that more persons are coming off unemployment rolls than going on. Indeed, the number continuing to collect unemployment benefits has fallen 10 million since early May, from nearly 25 million to nearly 15 million. To be sure, the drop still has a long way to go to get back to pre-COVID levels of around 2 million. (At the pace that it has been declining since the early May peak, the pre-COVID level would be reached in early December.)

Additionally, total retail sales in July recovered all of their COVID losses. However, the composition of those sales has changed a good bit. Sales at food and beverage stores, sporting goods stores (that includes bicycle sellers), building materials and garden supplies stores, and nonstore retailers (such as Amazon) were all stronger while restaurants and bars and clothing sales were off a lot. No big surprise there.

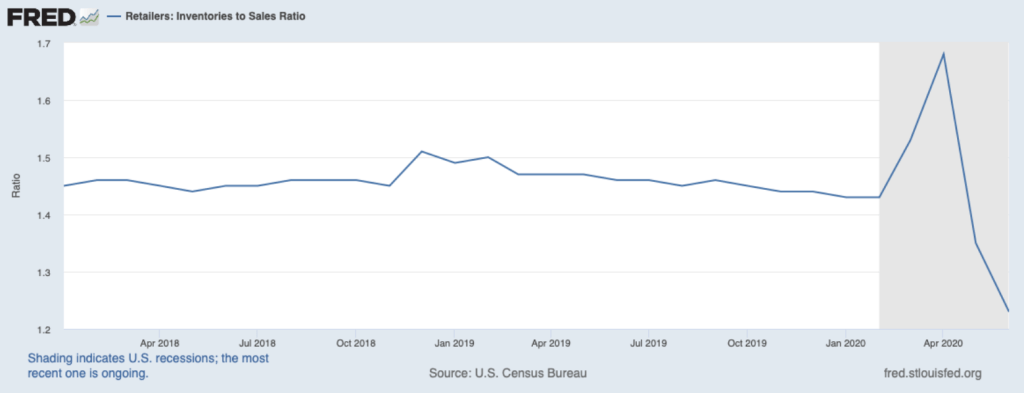

With retail sales outpacing production in recent months, retail inventories have plunged. This can be seen in the chart below, showing the inventory-sales ratio for the retail sector through June. In June, it dropped to the lowest level in more than a quarter-century. Perhaps you have been annoyed by frequent empty shelves and the need to backorder an item you want. Nonetheless, this bodes well for production going forward, as retailers have been stepping up their orders to replenish bare shelves and meet brisker demand.

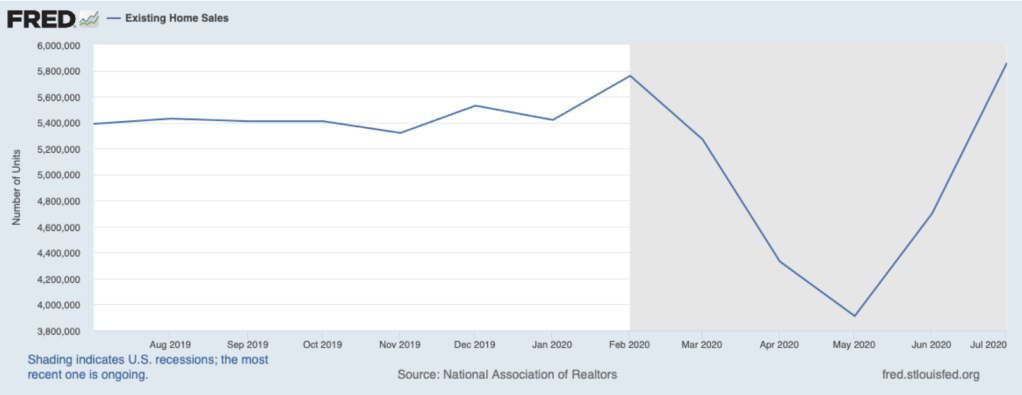

Notable, too, has been the rebound in home sales. The chart below illustrates that existing home sales in July rose above the pace on the eve of the COVID crisis. A similar story can be told for new home sales. Ultra-low mortgage rates have been helping to boost home sales (see July 13, 2020 blog, Buoying the Market: Ultra-Low Interest Rates), but buyers would not be sticking their necks out to make these big-ticket commitments unless they were confident that the road ahead has a green light.

Helping to support the recovery in retail and home sales has been the stock market (shown below for the S&P 500). In addition to low-interest rates, the earnings picture has contributed to the bull market in stocks. Corporate earnings are very sensitive to the state of the economy. Accordingly, in the second quarter, they fell sharply, but not as much as had been expected. Moreover, expectations for coming quarters have been marked up steadily as the recovery has gotten legs and uncertainty has been receding. Within the corporate sector, technology and health care firms have been pacing the improvement, while real estate (especially the office sector), energy, and utilities have been laggards. No great surprise there, either.

Putting it all together, the economic recovery from the COVID plunge continues, and prospects look favorable going forward. In general, this recovery continues to outshine the expectations of experts. It appears that the renewed spread of COVID in July did not put a big dent in this recovery. Pent-up demand and the need to restock shelves will be fueling growth in the months ahead. Looking ahead, the huge bounce that we have experienced since April’s bottom will necessarily moderate over the rest of this year (trees don’t grow to the sky). But growth will remain impressive. Market economies have remarkable resilience, as discussed in Chapter 2 of my book, Capitalism Versus Socialism: What Does the Bible Have to Say?