Many analysts are worried about the recovery losing steam, especially in the face of renewed outbreaks of COVID-19 and the absence of more fiscal stimulus. Yet the unemployment rate fell to 6.9 percent in October, down nearly 8 percentage points from its peak six months earlier in April. To put this information in perspective, it took four years for the unemployment rate to drop to 6.9 percent in November 2013 from its peak of 10.0 percent in October 2019. Moreover, the surge in GDP in the third quarter erased two-thirds of the plunge over the first half of the year.

Yet, not all sectors of the economy have shared in the turnaround. The service sector—notably restaurants and bars, hotels, airlines, and theaters—has lagged a good bit. This can be seen in the table below, showing the percent change in employment since the peak in February. Private employment was down 6.8 percent in October from February. Within the total, the goods-producing sector (mining, construction, and manufacturing) declined 4.7 percent and the private service sector declined 7.2 percent. Within the service sector, there was a lot of variation. Employment in financial services had recovered nearly all the earlier loss, and the bulk of the loss of health care jobs had been restored—except for nursing home workers. However, employment in leisure and hospitality (hotels, entertainment, and restaurants and bars) was down more than 20 percent in October, as was airlines.

| Sector | % Change: February to October |

| Total non-farm private | -6.8 |

| Goods producing | -4.7 |

| Private service producing | -7.2 |

| Financial activities | -1.5 |

| Health care | -3.6 |

| Leisure & hospitality | -20.7 |

| Airline transportation | -24.4 |

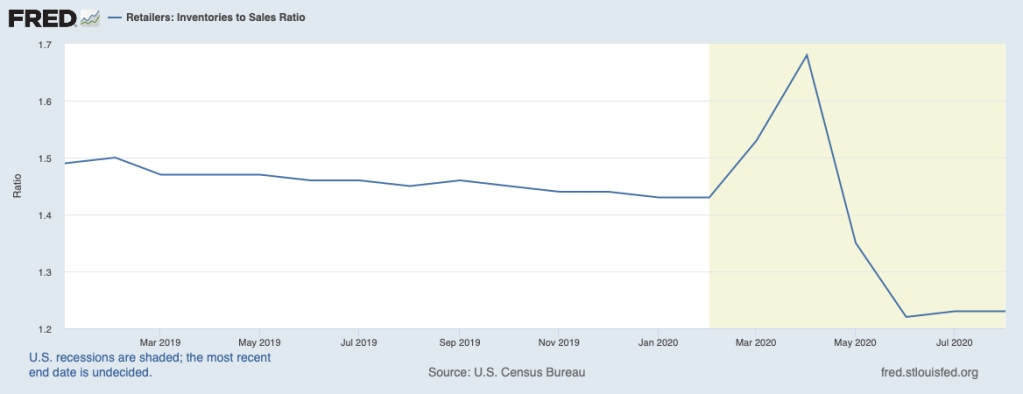

In the months ahead, employment in the goods-producing sectors will be getting a boost from the lean inventory situation. The chart below illustrates retail inventories relative to sales are very low (the spike in April reflected a collapse in sales rather than a buildup in inventories). Manufacturers have been reporting growing order books for some months as retailers are taking measures to restock their shelves.

Taking all of this into consideration, what direction will the economy be taking beyond the near term? In virtually all areas of the economy, things will get back to levels they were at before the pandemic. But that may in many cases take a very long time. Airplanes, theaters, and stadiums will be filled again. Restaurants and bars will again have high-density seating, but the time path for getting back will not be the same for airlines as for bars and restaurants or for other impaired sectors. Moreover, many businesses will not be able to survive that long. To a degree, the time that it will take will depend on how long it will take to contain the virus.

Once this point is reached, there, nonetheless, will be more office workers working from home, more students taking online classes, and more conferences and meetings taking place virtually instead of in-person. But that was the trend before COVID-19.

Meanwhile, resources need to be moving from these trailing sectors to the sectors that are expanding. Job openings have picked up in the more robust industries and, the sooner people move from idleness to these sectors, the smoother will be the transition. Inducements to stand in place will only lead to delays in getting to the inevitable.

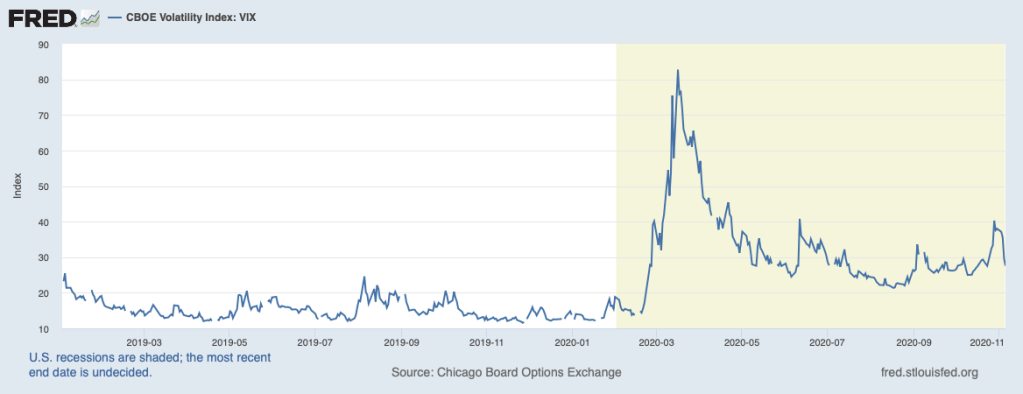

The markets appear to be sanguine about the implications of the election on the economy. Stock prices rose over election week and prospective volatility of stock prices, constructed from options on the S&P 500, ended the week where it started (chart below). The market went up because the investors seem to have factored in the political gridlock in the coming years, and the market typically likes gridlock.