The recent news on retail sales and job claims, along with renewed outbreaks of COVID-19, seem to be suggesting that we are in for a long, dark winter. The zip in the economy seems to be gone.

However, it is worth putting recent developments in perspective. The economy still has forward momentum. Recall that the burst of growth of real GDP in the third quarter erased two-thirds of the decline over the first half of the year. Moreover, the evidence for the current quarter points to the gap closing further. Indeed, it appears that the shortfall in real GDP in the fourth quarter will be only about 2 percent from a year earlier.

As shown in the chart below, continued unemployment insurance claims are still dropping, although they remain elevated compared to earlier in the year. This means that more people are coming off unemployment rolls than are going on, and this is giving a lift to output in the fourth quarter. Moreover, other evidence shows that hires in recent months have returned to the pace of earlier in the year and job openings have reached those of a couple of years ago. Thus, the labor market continues to improve, despite the headwinds.

Other evidence of momentum can be seen in the housing sector. Existing home sales have surged in recent months to the fastest rate since the extraordinary housing boom of a decade and a half ago, as seen in the chart below. A similar story is told by housing starts, especially for single-family homes, which keep climbing higher.

It should be noted that not all are sharing in this recovery. Those involved in certain portions of the service sector—restaurants and bars, airlines, entertainment—have been lagging (the “outs”). These tend to be workers at the lower end of the pay spectrum who have less wherewithal to deal with a protracted shutdown.

Retail sales for October tell the story. While total retail sales were 5.7 percent above a year earlier, sales at food and drinking establishments were 14 percent below October 2019 and clothing sales were off 12-1/2 percent. In contrast, motor vehicle, building and garden materials, food and beverage stores, and sporting goods sales in October had all risen by double digits from a year earlier. Moreover, sales by nonstore retailers (Amazon) had increased by nearly 30 percent. These gains, coupled with depleted retail inventories, bodes well for those in the goods-producing sectors of the economy in the coming months (the “ins”).

This uneven performance can also be seen in existing home sales over the past year, as shown below. Sales of homes priced at $1 million or above are up a stunning 100 percent! But the gains tail off quickly as home value shrinks. Indeed, sales actually have fallen at the bottom end.

There will need to be progress in reopening the economy for things to improve for those at the lower rungs of the economic ladder. Hopefully, breakthroughs on the vaccination front will translate into better opportunities for those who have been left behind by the COVID shock. Delays in reopening will continue to hit the most vulnerable workers and small businesses hard.

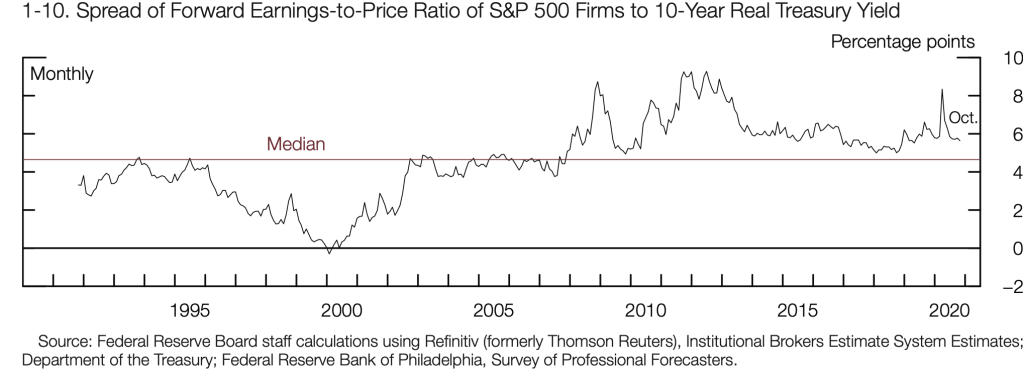

Finally, concern has been raised about whether the stock market is too lofty for an economy that is struggling to get back on its feet. The chart below provides some insight into this question. Shown is the excess of the earnings return on stocks in the S&P 500 over a risk-free (Treasury) interest rate. When this spread is very thin (well below the median), there should be concern about overvaluation. For example, that spread was extremely tiny (even negative at one point) during the stock market bubble of the last half of the 1990s. The market then went through a painful correction.

Looked at in this light, prices do not appear to be out of line with fundamentals. Much of the recent lift to share prices has come from ultra-low interest rates, and low rates are likely to be with us for some time (See July 13 blog, Buoying the Market: An Era of Ultra-Low Interest Rates). Also, it is worth noting that the businesses that have been set back the most by COVID are not well represented in the S&P 500 (See October 12 blog, What’s the Market Telling Us?). The pandemic has hit small businesses disproportionately and they don’t fit into the S&P 500.

One thought on “The Ins and Outs of This Recovery”