The economic news of late—retail sales, labor market data—and the COVID-19 outbreaks and tighter restrictions has been somewhat discouraging. Many have concluded that the recovery has come to an end, and more fiscal stimulus is needed. The incoming president is proposing nearly $2 trillion in new stimulus—on top of the $0.9 trillion recently enacted.

Such a fiscal package will help many businesses and workers who are barely hanging on. But it will also delay transitioning to new lines of activity that are being occasioned by the pandemic. As noted in previous commentaries, once the effects of the pandemic are over and the economy has fully recovered, many businesses and jobs—primarily in the service sector—will not return (see The Ins and Outs of This Recovery, November 21, 2020, and What’s the Market Telling Us? October 12, 2020). They will be replaced by others. This means that workers and other resources will need to transition to the expanding sectors. Assistance now will delay this transition.

Moreover, the additional borrowing needed to cover stimulus outlays will add to the already massive burden being passed on to younger generations. An additional $1.9 trillion added to the deficit for the current fiscal year would mean that the national debt would increase nearly $5 trillion this fiscal year—nearly a 25 percent increase. The chart below shows that, before the recent fiscal package, debt owed to the public in relation to GDP was expected to reach nearly 200 percent at mid-century—roughly double the current level and the level during the World War II national emergency.

This would be well in excess of the debt burden faced by Greece at the time of its stifling crisis of a decade ago.

Looked at differently, currently, debt owed per person in the United States is $61,000. If we assume that the debt burden in 2050 will fall on those currently 50 years old and younger, the amount owed per person in 2050 will be a staggering $185,000. The interest on this amount of debt will require massively higher taxes or sharp cutbacks in other government outlays—including entitlements social security and health care. It’s going to be a substantial load.

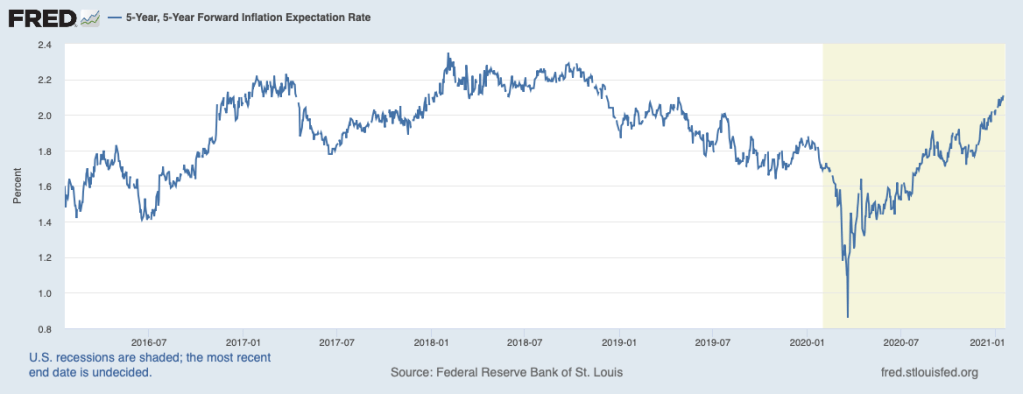

Already, markets are anticipating more inflation down the road. The chart below shows that expectations of inflation five years ahead have risen markedly over recent months and currently exceed the Fed’s target of 2 percent. If more stimulus is passed, this likely will keep moving higher as the Fed is likely to be slow in responding.

Furthermore, the recent slowdown is likely only a pause. As noted in other commentaries, the fundamentals are very favorable for ongoing expansion (see Taking Stock of the Recovery, January 4, 2021). Consumers have been saving a lot of their income and have room to step up their spending, especially given their strong wealth positions. Additionally, businesses have delayed investment projects that will be getting the green light as uncertainty about the direction of the economy continues to recede. Also, lean retail inventories have led to more orders and production at suppliers.

To be sure, many are still struggling to hang on and will not be participating much in the near-term expansion. But opening up these sectors will do much to help those capable of surviving in the post-COVID economy.