Isn’t the stock market supposed to be a barometer of the economy? Yet, while the market climbs, hasn’t news on jobs and the economy been mixed? New claims for unemployment insurance seem stalled at a high level and many businesses are struggling, if not failing. Isn’t there a disconnect? Could the market be headed for a crash?

The chart below shows that the S&P 500 stock price index (the blue line) has recovered all of its spring pandemic-related losses and the tech-laden Nasdaq (red line) has soared above its previous peak. In contrast, total output in the third quarter had not recovered its sharp contraction in the spring and was on the order of 3 percent below its level at the end of last year. Notably lagging in the recovery have been certain services—such as air travel, entertainment, office, and retail properties, hotels, restaurants and bars, hair salons, and gyms—which continue to be held down by COVID-19 restrictions. Demand for goods, in contrast, has been robust since the spring.

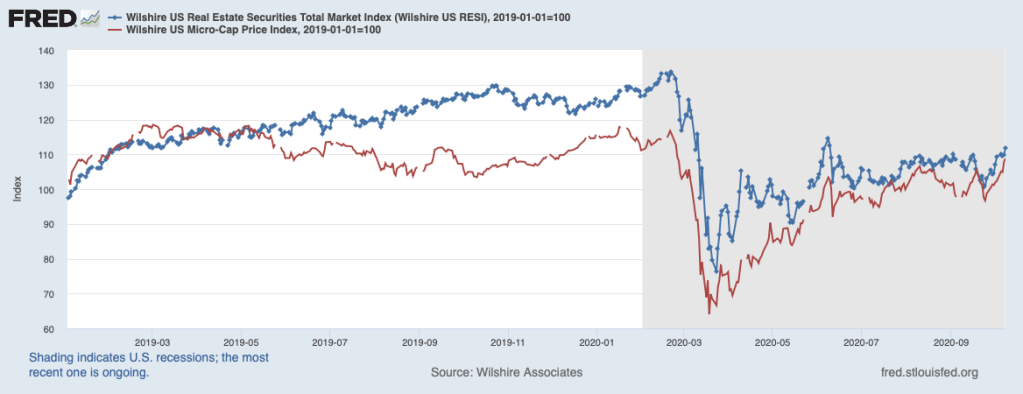

The chart below shows that the value of securities related to commercial rental properties (the blue line) has risen only a bit from lows in the spring. Similarly, publicly-traded very small (micro) businesses (the red line) continue to languish. Smaller businesses are represented disproportionately in the struggling portions of the service sector, the bulk of which are not corporations with publicly traded stock and do not appear in the major stock price indexes. They are commonly sole proprietorships or partnerships. Chances are you know of some small businesses and their employees who continue to strain to make ends meet.

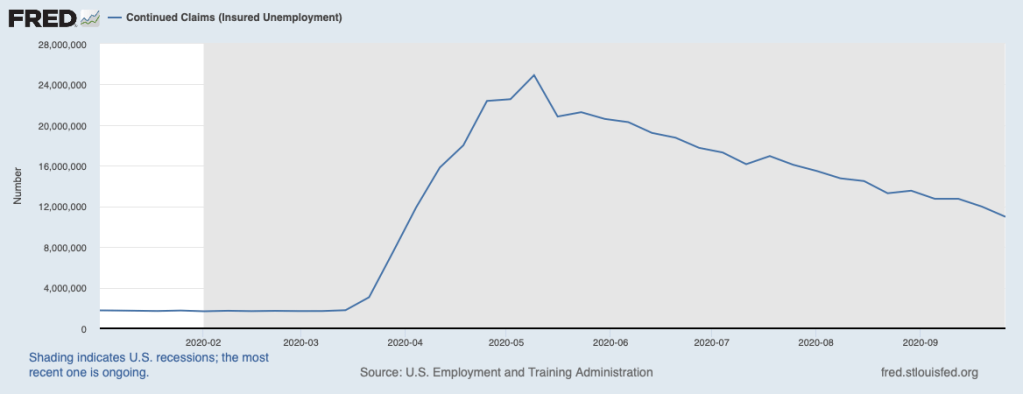

Despite this uneven performance among businesses, the job market, overall, continues to improve. Shown below is the number of persons continuing to collect unemployment benefits. It has been marching steadily downward since May, as more people are returning to jobs than are applying for new benefits.

Continued labor market improvement is also indicated by the broad measure of the unemployment rate (the red line in the chart below). This so-called U-6 measure of unemployment includes discouraged workers who are not classified as being in the labor force and persons who are working part-time involuntarily (they seek full-time work). The U-6 rate rose faster than the standard U-3 measure (shown in blue) during the lockdown in the spring. But it has dropped more sharply over recent months. The gap between them reached 8.2 percent at its peak in April, roughly 5 percentage points above normal, and has shrunk to 4.9 percent in September, only 1-1/2 percentage points above normal.

Putting these pieces together, the expansion is well underway in many parts of the economy, those sectors that produce goods and are well represented in the S&P and Nasdaq indexes. But many segments of the service sector—those heavily represented by small businesses—are being left behind. Some of those will not make it, while others will only partially reach their pre-pandemic business level, at least for some time. Meanwhile, their workers are being redirected to more vibrant sectors of the economy.

The major stock market indexes— S&P and Nasdaq—are reflecting the sectors that have recovered nicely. It is important to keep in mind that corporate earnings are very sensitive to the stage of the business cycle, and the third quarter witnessed a big snapback in the overall economy from the spring plunge. This portends well for the earnings of the bulk of businesses appearing in these indexes. These are companies that have been able to bounce back smartly and, for the most part, are not those continuing to be plagued by the pandemic. Furthermore, interest rates have dropped substantially since earlier in the year, and this is providing a substantial lift to all share prices (See, July 13, 2020 blog, Buoying the Market: An Era of Ultra-Low Interest Rates). Thus, the current level of share prices in the S&P and the Nasdaq is based on expectations of good upcoming earnings reports against a backdrop of very low-interest rates used to discount those earnings. Thus, the market appears to be well supported by fundamentals and is not poised to enter bear territory.

For more on how market economies adapt to shocks, such as COVID, see Chapter 2 of my new book, Capitalism Versus Socialism: What Does the Bible Have to Say?

One thought on “What’s the Market Telling Us?”