Analysts seem divided on where the economic recovery from the COVID shock stands. Some see recent news to be pointing to a still-vigorous expansion—a “V”-shaped recovery. But others read the news, including new COVID outbreaks, to be suggesting that the expansion is stalling out or even receding—that is, a “W” is unfolding. Putting the various pieces together, a lot of progress has been made over recent months, but it has been uneven. Many sectors have made up lost ground and, going forward, are looking good. However, others have been lagging and will be slow in getting back on their feet or may not make it all the way. The ongoing struggles of these businesses and their employees have implications for credit losses at financial institutions.

Shown below are percent changes in the level of real GDP—national output—measured at a quarterly (not annual) rate in 2020.

| 2020 (e—estimate) | Percent Change in Output |

| Q1 | -1.3 |

| Q2 | -9.1 |

| Q3e | 7.3 |

The big decline occurred in the second (spring) quarter when output declined 9.1 percent (31.7 percent at an annual rate). The rebound in the third quarter, still an estimate, makes up the bulk of that decline. If growth in the fourth quarter slows to 3 percent (12.6 percent at an annual rate), output would end the year only 0.8 percent below a year earlier. This recovery would have to be characterized as a “V.”

The service sector—entertainment, air travel, hotels, and restaurants and bars—took the brunt of the COVID impact and has been facing the biggest challenge in coming back. With a few exceptions, the service sector is characterized by smaller businesses, and employees working in this sector tend to have earnings toward the lower end of the pay scale. Employment in these industries has recovered from its bottom this spring, but has far to go to return to pre-pandemic levels. Progress will depend on success in containing COVID and the ingenuity of business owners in being able to safely accommodate their customers. Meanwhile, many businesses will continue their battle to survive and a portion of their workforce will need to find work elsewhere. Also in the service sector, owners of office and retail buildings are facing a growing overhang of unoccupied space, as shopping online and telecommuting have proved to be more viable than was believed before the pandemic.

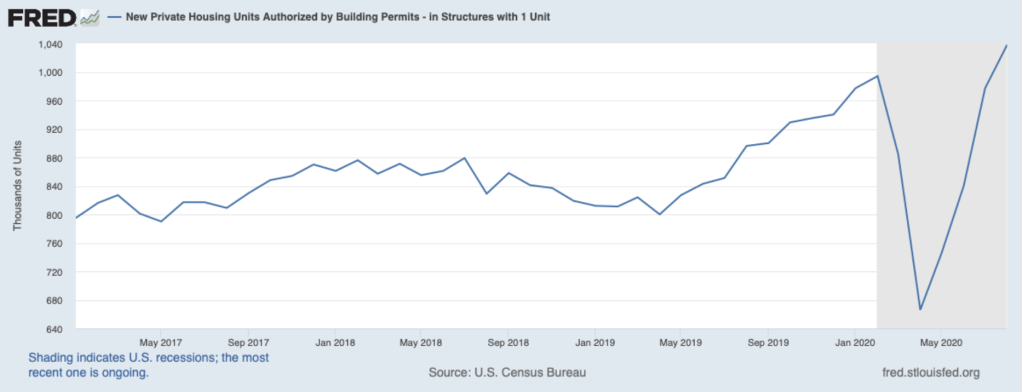

While slack will persist in the service sector, other sectors have been doing well. Historic low mortgage rates and greater telecommuting and remote learning have enlarged the demand for home space and sparked a boom in the housing sector, especially single-family homes. The chart below shows the recent surge in permits for single-family homes, which in August surpassed their February peak. Sales of building materials also have been robust over recent months, suggesting that additions and alterations to existing homes have been booming. Vibrancy in housing activity has been most evident in the upper end of the market where year-over-year existing-home sales are up 50 percent or more in many parts of the country. In contrast, existing home sales at the lower end are down from a year earlier. These divergent housing trends highlight the disparate impact of the COVID shock.

Elsewhere, demand for both durable and nondurable consumer goods, especially bigger-ticket durables, has snapped back and domestic production of consumer goods has nearly recovered all of its COVID-shock decline. Inventories of consumer goods have been drawn down and order books for restocking have been building rapidly. This activity bodes well for production going forward and for employment in those sectors. It also illustrates that many households feel confident enough to commit to deferrable big-ticket items involving future loan payments.

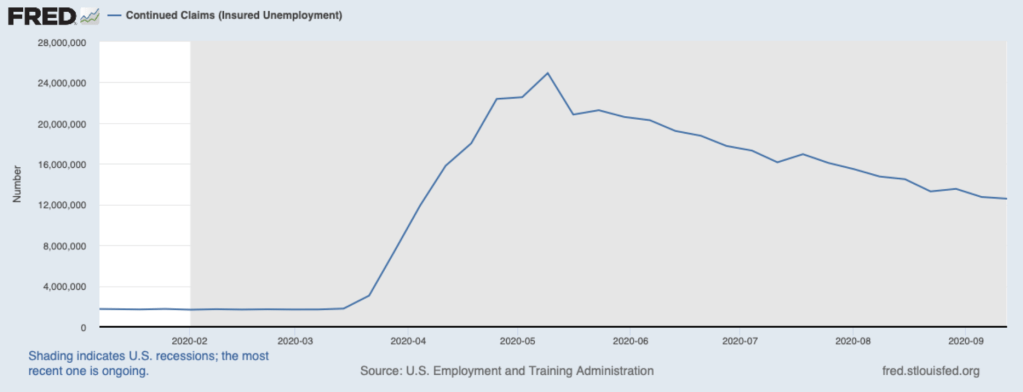

Overall, conditions in the labor market continue to improve, as shown below by the ongoing decline in people continuing to collect unemployment insurance payments. Despite, still-high new claims for unemployment insurance, more are dropping off the rolls and returning to work than going on the rolls. Elevated unemployment is concentrated in the service sector and many of those unemployed service-sector employees will need to look to other sectors of the economy to find work—or be extremely patient.

The prolonged slump in the service sector and certain other sectors of the economy has led to many borrowers falling behind in their debt-service payments. Government regulators have encouraged lenders to practice forbearance during this period, and, as a consequence, there is a lot of uncertainty about how many borrowers will remain behind in their payments and the corresponding credit losses. There is a risk that, once realized, credit losses could be substantial and some financial institutions will need to scale back their role of providing credit to the economy.

In sum, the economy has continued to show gains, but not all are sharing in the recovery. Nor are those lagging likely to experience a quick turnaround in their fortunes. Nonetheless, entrepreneurial ingenuity continues to respond to the COVID threat in many ways that are knocking down barriers to the recovery. For more on reasons why market economies are so adaptive to setbacks such as COVID, see Chapter 2 of my book, Capitalism Versus Socialism: What Does the Bible Have to Say?