Are you exhausted from watching the craziness in the market for GameStop stock and a few other companies? Are you upset by the decision of some brokerage firms, most notably Robinhood, to restrict trading in GameStop and a handful of other stocks? Are you fascinated by the story of David (small investors) versus Goliath (hedge funds) unfolding before our eyes? What on earth is going on in the market and can the craziness continue?

It is widely believed by analysts that the price of a share of stock is determined by fundamentals—specifically, the outlook for the company’s earnings, the perceived risk associated with holding those shares, and the level of interest rates. Prices will rise if there is an improvement in earnings prospects or risk is perceived to have diminished or interest rates have fallen. Because these fundamental forces are always changing, stock prices bounce around a lot.

Helping to ensure that prices stay in line with fundamentals are hedge funds and other professional investors. When the prevailing price of a share departs from that implied by fundamentals, hedge funds see a profit-making opportunity by buying when the current price is thought to be below that implied by fundamentals or selling when it is above. Selling of the stock is commonly done by shorting the stock—borrowing someone else’s shares and selling them. Large profits can be made when the hedge fund or other professional investor assesses things correctly and the price of the stock moves into alignment with fundamentals. In the case of short sales, the investor sells the borrowed shares at the higher price and buys them back at the lower price corresponding to their fundamental value, pocketing the difference. (This view of stock prices is commonly referred to as the efficient markets hypothesis—see Chapter 6 of my book, Financial Markets, Banking, and Monetary Policy, 2nd ed., Kendall-Hunt, 2020.)

However, bubbles occasionally occur in the stock market and in other markets in which prices rise well beyond levels that can be supported by fundamentals. Notable examples are the dot-com bubble in the stock market in the second half of the 1990s and the residential real estate bubble several years later. In both cases, prices moved well above fundamentals and stayed there for a while. In each case, the bubbles burst and prices collapsed. The tech-laden Nasdaq stock index fell 70 percent (and indexes of the broader market fell roughly 40 percent). In the real estate market, prices fell on average nearly 30 percent (and much greater declines were registered in some local markets).

Bubbles involve a dynamic in which investors come to believe that recent price increases in an asset will persist, at least for a while, and that they can get extraordinary returns by getting in on the action. There is also optimism by these investors that if prices turn down they can get out before others and avoid holding the bag. (Acquiring options—calls if you believe the price will go higher and puts if you believe the price will fall—is another way to take a position in stocks). In all bubbles, prices sooner or later return to levels corresponding to fundamentals—gravity ultimately prevails. In many cases, the plunge in prices overshoots, and prices drop to levels below those implied by fundamentals for a time. Once this happens, it becomes a good time to buy.

These days, many investors are annoyed by the ultra-low level of interest rates that are holding returns on many other investments down (see The Impact of Ultra-Low Interest Rates, January 28, 2021). This has prompted some investors to seek risky opportunities for big gains. What is different today than in past bubbles is widespread communications possibilities among investors on platforms such as Reddit’s WallStreetBets, Twitter, and other social media. As a consequence, a multitude of small investors can move at once to buy or sell on the advice of a self-proclaimed market guru. This herd activity has come to be a powerful force driving up share prices of targeted companies such as GameStop, AMC Entertainment, Nokia, and BlackBerry.

As prices of these companies have soared, hedge funds and other professional investors perceived a profit opportunity to sell these companies by shorting them, thinking that their share prices would soon come tumbling down. But small investors, enjoying huge instant returns, have kept on buying, more than offsetting the impact of short-sellers. In these circumstances, hedge funds have found themselves in a bind needing to buy shares in these companies to pay back the lenders of the borrowed shares. Their actions at times have added to the upward pressure on share prices. Hedge funds and other investors ended up buying these shorted shares at much higher prices than they sold them, inflicting huge losses. (Note that, on net, hedge fund short selling has a neutral impact on share prices—they put downward pressure on prices when they sell borrowed stock and upward pressure when they buy those shares back; the upward pressure from short-sellers, though, recently has added to the upward momentum coming from small herd investors and has strengthened the upward price dynamics). The actions by these various players have led to a mind-boggling 1,600 percent increase in GameStop shares since the start of this year. David once again slew Goliath.

Note that small investors have concentrated on a few targeted stocks and have not been buying the broader market, as they could, for example, by purchasing S&P 500 exchange-traded funds (ETFs). Even as a group, these small investors would not have enough clout to move market prices very much in the broader market for S&P 500 company shares valued in excess of $40 trillion.

Looking ahead, the bubble in the price of these targeted companies will burst and many small investors will face big losses. Those investors who chose to sell shares and lock in gains while prices were still rising will end up being winners. The gains of those who sell before the peak will be paid for by the prospective losses of those who bought their shares during the run-up in share prices and rode them down once the bubble burst.

Meanwhile, turmoil in the bubble stocks is contributing to the recent sell-off in the market more generally. The chart below shows the prospective volatility of the S&P 500 based on options prices. As this index gets larger, market participants are expecting more volatility in share prices over the near term. Also, risk premiums affecting share prices will get larger, putting downward pressure on S&P 500 share prices. The chart shows that implied volatility has jumped higher in recent days reflecting growing concerns about bubble stocks as well as concerns about delays in the distribution of COVID vaccines. The chart also shows that prospective volatility is not terribly great by the standards of the past year.

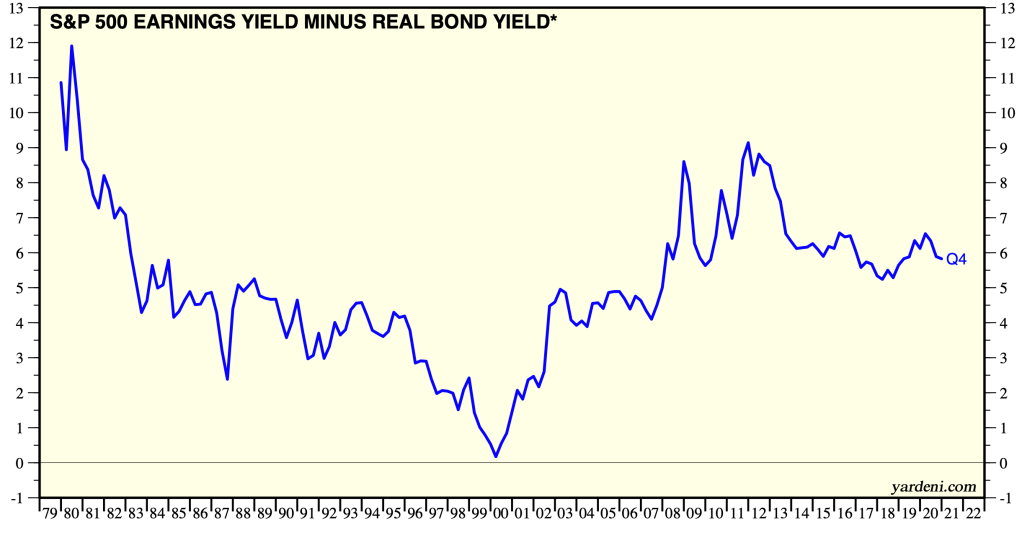

Looking at valuations in the broader market, it seems that the prices of S&P 500 shares are not out of line with fundamentals. Shown next is a measure of the risk premium (or so-called equity premium) on stocks in the S&P 500 through the end of last year. It illustrates that the risk premium dropped to virtually zero by the end of the 1990s (investors were not insisting on compensation for the extra risk of holding stocks over holding risk-free Treasury securities): In other words, a bubble had developed in the market more broadly, not just in tech stocks. As this bubble burst, the equity premium rose sharply and then climbed even higher during the financial crisis of 2008 and 2009. However, more recently, the equity premium has settled into a normal range, implying that S&P 500 prices are aligned with fundamentals (if this chart were to be extended into the first month of 2021, the risk premium would not have changed much from the end of 2020).

In sum, the herd mentality among small investors has been pushing the prices of a few targeted shares to extraordinary and unsustainable levels over recent weeks. The ongoing upward momentum has caused huge losses for some hedge funds that have tried to profit from overvalued share prices. But, in time, the bubble in these shares will burst—gravity will bring the prices of targeted shares back to earth—and many small investors will join the hedge funds in getting burned by this fling. Both David and Goliath will be bleeding.