Anemic job gains in January and stubbornly high new claims for unemployment insurance have led many to conclude that the economic recovery has stalled out and that more fiscal stimulus is needed to jump start the economy.

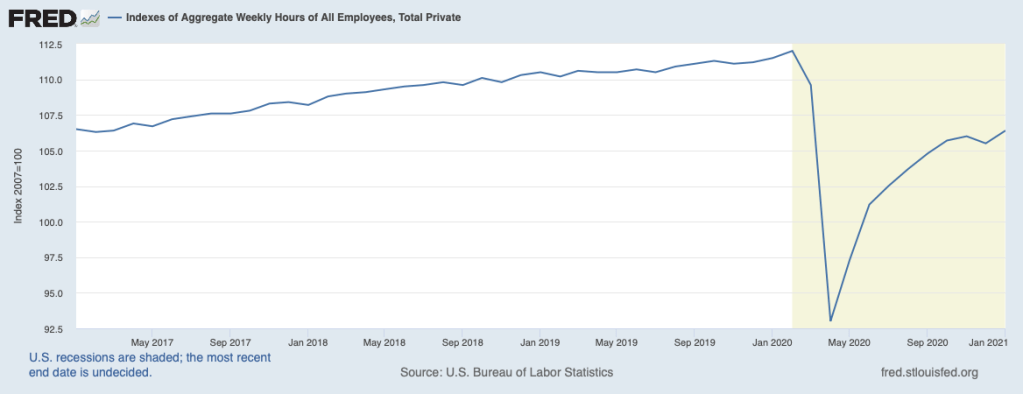

It should be noted that the employment report for January contained some encouraging signs, and the economic fundamentals point to a pickup, especially as the COVID-19 threat recedes. While the establishment survey of employers showed job gains of only 49 thousand in January (just 6 thousand at private-sector employers), the household survey (generally thought to be less reliable) showed gains of 201 thousand that same month. This suggests that the upturn in employment from the weakness in December may be a little more vigorous than headlines have portrayed. Furthermore, the January employment report showed that hiring by temporary employment services was unusually strong and that the average workweek jumped 0.3 hours to 35 hours—a sizable increase. It stood 0.7 hours above a year earlier, just before the lockdowns. What these features of the employment report are reflecting is that employers need more labor to meet rising production schedules. However, employers are proceeding cautiously by using temps and getting their current employees to work longer hours. This is a very common pattern for an economy that is gaining strength. Only once employers are sure that demand will persist, will they turn to adding more permanent workers. With the big increase in the average workweek in January, total hours worked last month increased 0.9 percent (more than 10 percent at an annual rate!). A sizable increase in total output in the first quarter of 2021 is implied.

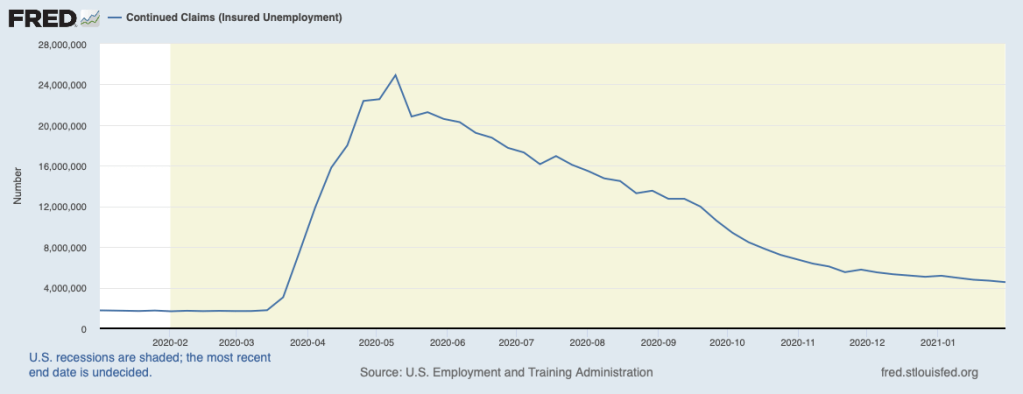

Early readings on the labor market in February suggest ongoing, but gradual, improvement. Continuing claims for unemployment insurance, shown in the next chart, have been edging lower. As a consequence, more people are coming off the unemployment rolls than going on.

Looking ahead, as noted in recent commentaries (see, Taking Stock of The Recovery, January 6, 2021 and The Demise of This Expansion is Greatly Exaggerated, December 12, 2020), the fundamentals favor a resumption of faster growth. For households overall, wealth positions are strong, and they have been saving an unusually large portion of their earnings. Accordingly, pent-up demands will be translated into more spending and with it the need to ramp up production and employment, including to rebuild very lean retail inventories.

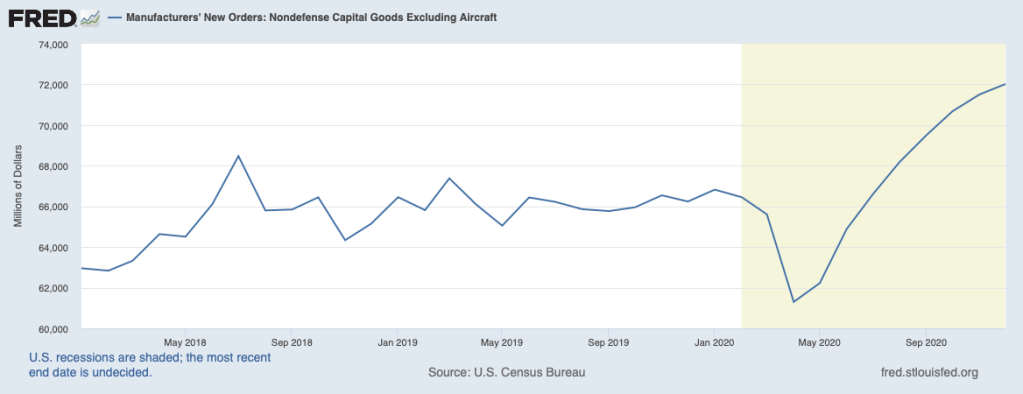

Moreover, businesses have stepped up their orders for capital goods over recent months, as shown next, to levels well above pre-pandemic levels. Rising order backlogs of capital goods also are prompting a strengthening of production. Around midyear, the economy should return to its pre-pandemic level.

To be sure, not all businesses and households will be sharing in the rebound. Various services—notably air travel, lodging, and restaurants and bars—will continue to lag. In some cases, business sales in these sectors will not return to pre-COVID levels because consumers and businesses have permanently altered their spending patterns over the past year in response to the pandemic. This means that workers and other resources in the lagging sectors will be needing to migrate to more vibrant sectors of the economy. Consequently, fiscal measures that induce workers and businesses to stay in place are just postponing the inevitable.

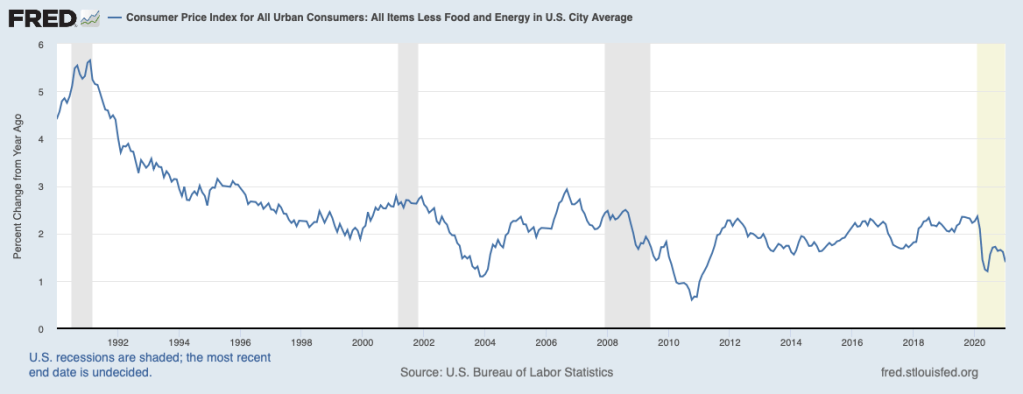

The preceding analysis suggests that there is sufficient impetus in place to achieve recovery of the economy and to put workers dislocated by the pandemic into jobs, be they their old jobs or new ones. A concern that has been mounting of late is whether inflation might be unleashed in the process, especially if the proposed nearly $2 trillion fiscal package is enacted. Recent news on prices has been fairly benign. While the headline CPI for January rose 0.3 percent, core prices (excluding volatile food and energy components) were flat for the second consecutive month. Moreover, the twelve-month change in prices slowed to 1.4 percent, as shown below, and is very low by the standards of recent decades. Among the components of the index, the pandemic has left distinct imprints. Airfares, hotel rates, and prices of men’s suits and women’s dresses are all down considerably from a year ago. In contrast, household paper products (toilet paper), cleaning supplies, major appliances (plagued by pandemic-caused production bottlenecks), and moving expenses (as many have been escaping large cities faced by COVID and high taxes) all registered outsized increases in prices.

Nonetheless, participants in financial markets have come to expect more inflation down the road. The chart below shows a rough gauge of expected inflation over five years beginning five years ahead. Expected inflation has more than recovered its early pandemic plunge and has climbed above the Fed’s 2 percent target. Growing prospects for a big fiscal stimulus package have contributed to this changing inflation outlook.

The Fed has reaffirmed its intention to continue buying Treasury and mortgage securities at nearly a $1-1/2 trillion annual pace indefinitely, thereby again indirectly absorbing a large share of new borrowing by the Treasury. The Fed has indicated over recent months that it is seeking a pickup in inflation to a pace moderately above 2 percent to compensate for persistent shortfalls from 2 percent over the past several years.

The Fed may be getting its wish to have inflation move above 2 percent before too long, especially with new fiscal stimulus. However, the Fed may also face a big challenge should the upturn in inflation gain momentum, which will become more likely if inflation expectations continue moving higher. Should inflation heat up, the question will be how vigorously the Fed will move to restrain it and whether that decision will interrupt the economic expansion.

For more on the regenerating forces at work in a market-based economy, see Chapter 2 of my book, Capitalism Versus Socialism: What Does the Bible Have to Say?