Not long ago, there was talk of a soft landing for the economy from the COVID shock—inflation picking up to the Fed’s 2 percent average target while vigorous growth in output and an improving labor market would result in full employment. However, then came the big surprises of sputtering employment gains and surging consumer prices (CPI) in April. Does this mean that all bets are off for reaching the soft-landing sweet spot?

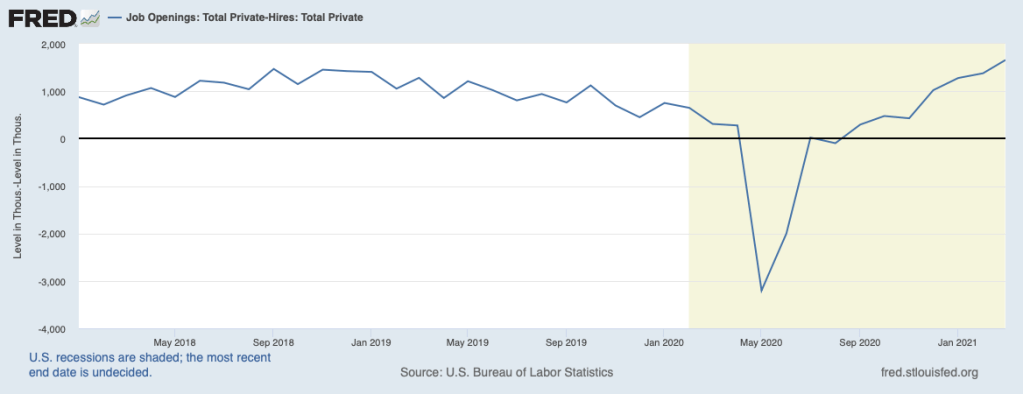

First, let’s look at the labor market. Increasingly, the problem is not the availability of jobs. In March (most recent data), job openings climbed to a new high. This should not come as much of a surprise because you have probably noticed that help wanted signs have sprung up everywhere. The National Federation of Independent Business (NFIB) reports that the share of small businesses facing difficulty in finding qualified workers rose still higher in April to an extraordinary 44 percent. Moreover, the chart below shows that the excess of job openings over hires continued on an upward trajectory, reaching an unprecedented level in the most recent report. Workers are not stepping forward to take the new jobs that have been created.

Contributing to labor shortages have been concerns by some workers about being exposed to COVID on the job. Also, many parents remain at home to care for children attending schools that have yet to reopen for full-time, in-class instruction. But both factors have been diminishing as the pandemic eases dramatically and as more children return to the classroom.

Playing a bigger role in the shortage have been generous supplemental unemployment insurance benefits that, along with standard benefits, exceed what individuals can receive by working. Indeed, the loudest complaints from employers have come from smaller businesses, especially in food services, employing workers in the lower rungs of the pay scale for which augmented unemployment benefits are most appealing.

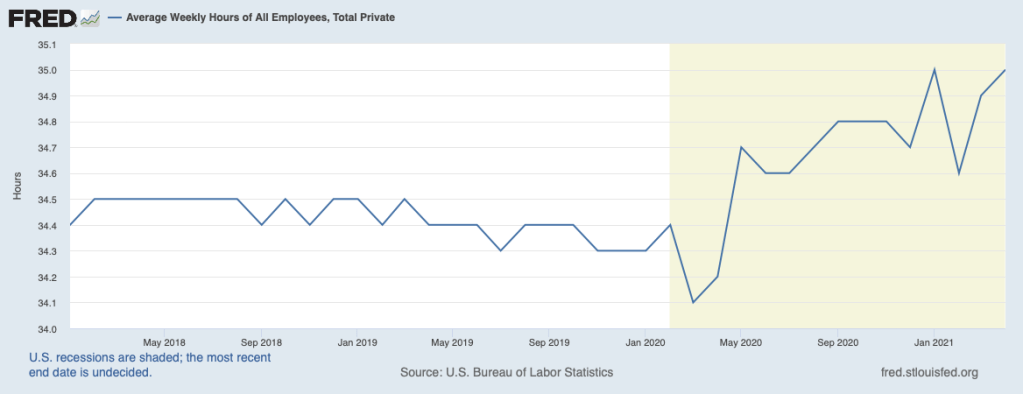

Employers have been coping with this situation by increasing the hours of their existing employees, including expanding hours for workers who had been placed on part-time employment. The chart below shows the average workweek through April. The average workweek dropped at the onset of the pandemic as production was curbed and the workweek leveled off later in 2020 as there were disruptions from a resurgence of COVID. However, the general trend has been distinctly upward (the drop in February owed to severe storms that shut down production in the south-central region). The recent readings on the average workweek are off the charts by recent historical standards.

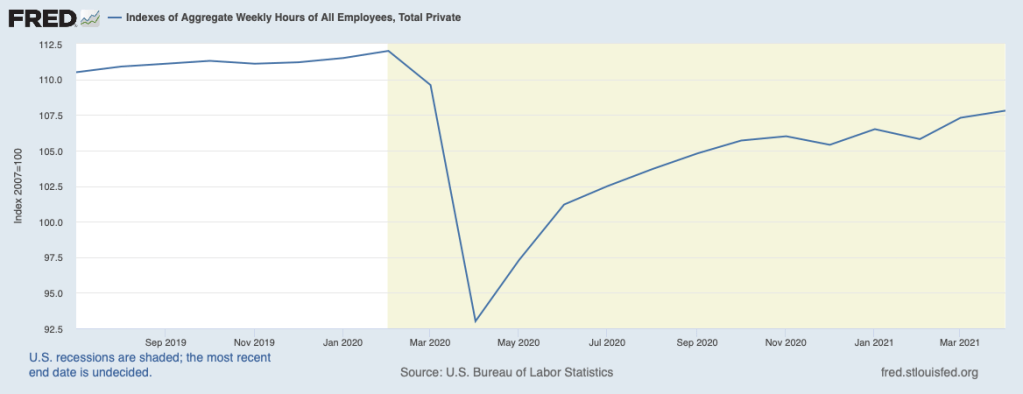

The increase in the average workweek has given a boost to total production hours, shown in the next chart. Even so, total production hours are roughly 4 percent below the peak in February 2020, at a time when total output has returned to its previous peak. The shortfall of hours implies that production hours will need to rise relative to output in the quarters ahead to realign the relationship between labor input and output.

Turning to the second recent surprise, inflation, consumer prices (CPI) rose 0.8 percent in April, despite flat energy prices. Increases were widespread, but they were especially large in commodities. The increase in prices of commodities (excluding food and energy) was a full 2.0 percent last month. Within this category, the price of used cars surged 10 percent as chip shortages curbed the production of new motor vehicles (and employment in that industry) and sent many buyers scrambling for used cars. Chip shortages also showed through in the prices of TVs (up 3 percent) and computers (up 5 percent), both of which typically decline over time. At the producer level, prices of consumer goods recorded sizable increases at both the final and intermediate stages of production, implying that more increases in the prices of goods at the consumer level are in the pipeline.

Large increases in service prices were also reported in April, especially for those services hardest hit by the pandemic. Airfares rose 10.2 percent, admission to sporting events jumped 10.1 percent, rates for lodging away from home (hotels) climbed 7.6 percent, and car and truck rental rates surged 16.2 percent.

Much of the outsized increases in the prices of consumer goods and services in April can be attributed to the return to a more normal economy and to temporary strains from the shortage of chips and other supply chain disruptions. Thus, these increases can be regarded as transitory and should not trigger inflation worries going forward. However, the pervasive increases elsewhere among goods and services suggest that inflation has indeed picked up on a more sustained basis and may be threatening to outpace the Fed’s target of 2 percent average inflation over time.

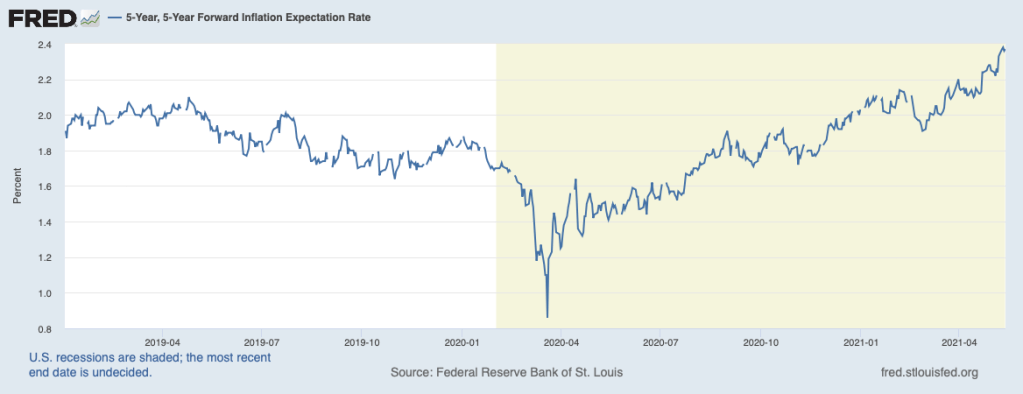

Indeed, market participants have become more worried about the outlook for inflation as shown by the increase in longer-term inflation compensation—expected inflation plus the premium for inflation risk—derived from the market for Treasury securities. Inflation compensation has moved up sharply over recent weeks, likely as both expected inflation and inflation risk has risen. This comes alongside a growing number of stories and commentaries expressing concern that the inflation genie has gotten out of the bottle. Rising inflation expectations by themselves will add upward pressure to inflation on a sustained basis (see April 19, 2021 commentary, Inflation is Coming, but How Much?).

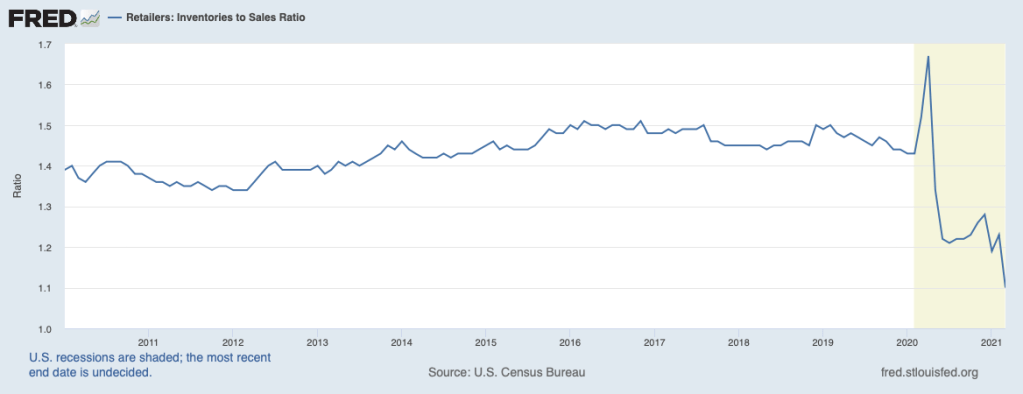

As noted in a recent commentary (see April 19, 2021 posting), inflationary forces are building that are being powered by strong consumer demand juxtaposed against restraints on supply in a number of sectors. Moreover, inventories have been drawn down to extraordinarily low levels, as shown in the next chart depicting inventories relative to sales in the retail sector. Efforts to replenish lean inventories are adding to demands being placed on producers.

It’s unlikely that producers can match the strong demand in the months ahead. The result is going to be ongoing pressures on prices, only some of which will be temporary. The risk at this point is that the Fed will be overshooting its near-term objective for inflation of moderately above 2 percent. It is seeking inflation moderately above 2 percent to balance against a steady shortfall from 2 percent over recent years in its effort to achieve average inflation of 2 percent over time. Whether in this situation the Fed will maintain its highly accommodative policy stance or begin to raise the federal funds rate and curtail asset purchases is an open question. In the first instance, the risks of even more inflation may be building, while in the second instance, the upward march in interest rates will come sooner and will spoil the party in financial markets. In any event, the prospects for engineering the desired soft landing seem to be fading.