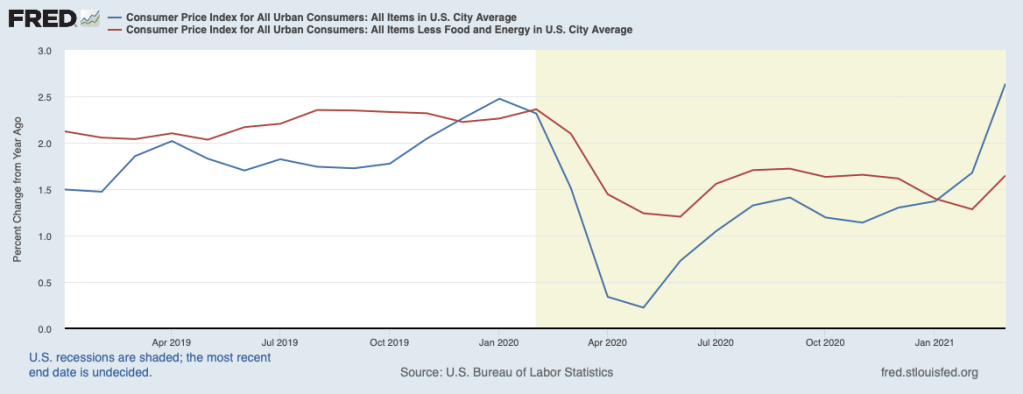

There is growing concern that inflation—the rate of increase in the prices of consumer goods and services—is on the way. Home prices are surging, consumer spending has snapped back, federal spending is on a tear, and the Fed has given no hint about slowing its provision of liquidity. Moreover, CPI (Consumer Price Index) inflation has jumped higher in recent months, as shown in the chart below by the blue line for the headline CPI. Much of the upturn in CPI inflation has come from the run-up in energy prices, notably the price of fuel at the pump. The upturn in core inflation—which excludes energy and food prices, the red line—has been much milder to date. However, at the producer level, there is clear upward pressure on finished goods prices and on processed and unprocessed materials used in manufacturing, which can be expected to pass through to consumer prices in the months ahead.

Do these price pressures mean that we need to be worried about runaway inflation? Economists view the inflation rate as being determined primarily by the amount of slack in the economy along with expectations of inflation by workers, businesses, and the public at large. We cannot measure either slack or inflation expectations directly, but various indicators suggest that inflation expectations have not drifted far from the Fed’s 2 percent target for inflation. One such indicator of long-term expectations of inflation is inflation compensation (primarily inflation expectations) for the five-year period starting five years ahead derived from the market for Treasury securities, the next chart. The chart shows that inflation compensation has been on the upswing in recent months, after dropping precipitously at the onset of the pandemic, but has not breached the 2018 level when inflation was tame. Overall, the recent behavior of inflation expectations should not be viewed as worrisome.

Turning to slack, one such measure is the unemployment rate which is still well above the level at the onset of the COVID shock (6.0 percent versus 3.5 percent). Moreover, the current unemployment rate understates slack in the labor market because many workers have been discouraged and have left the labor market, meaning that they have not been counted as unemployed. However, several goods-producing sectors have been facing supply-chain constraints and are having difficulty finding qualified workers. These sectors are experiencing excess demand and upward pressures on prices. In contrast, various segmentss of the service sector have been hit hardest by the pandemic—hotels, passenger airlines, and restaurants and bars— and are the ones with the most slack and least pressure on prices from this source.

Taken by themselves, inflation expectations and the degree of slack should not set off any alarms regarding the outlook for inflation. However, pent-up demands of households and businesses, augmented by massive fiscal and monetary stimulus, could change this situation quickly. It is quite possible that slack in the economy will be mostly absorbed by the end of this year, adding to upward pressure on inflation.

Moreover, there are inflation dynamics that are not fully understood. Coming out of the Great Recession of 2008-2009, actual inflation, though low, proved to be a good bit higher than standard models (based on a measure of slack and inflation expectations) were calling for, implying that our understanding of the inflation process was missing some pieces. Several years later, remaining slack in the economy appeared to be more than fully absorbed but actual inflation did not pick up as standard models were predicting. These episodes are useful reminders that our understanding of inflation is anything but complete.

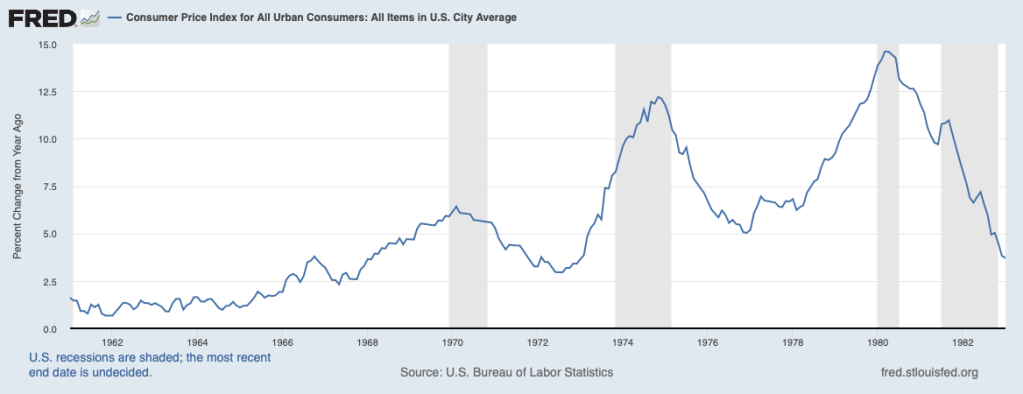

The last major bout of inflation began in the second half of the 1960s and then intensified over the 1970s. This is shown in the next chart. Like the current time, the second half of the 1960s was a period of very expansionary monetary and fiscal policies. In response, inflation moved from the 2 percent area, similar to now, to 5 percent. In the 1970s, inflation swung up and down, but moved to nearly 10 percent around the middle of the decade and finished the decade close to 15 percent. The spike in inflation around the middle of the decade was attributed to the relaxation of wage and price controls imposed by President Nixon that had been suppressing inflation and the OPEC cartel’s success in restricting oil supply and boosting energy prices. The run-up in the second half of the 1970s was attributed to overly stimulative monetary policy (leading to an absence of slack) and a ratcheting up of inflation expectations. Nonetheless, standard models of inflation seriously underpredicted the inflation that unfolded over that decade, implying that there was more going on in the inflation process.

The Fed last summer announced that its approach to achieving 2 percent inflation was being overhauled. Instead of being satisfied once inflation hit 2 percent, it would be seeking average inflation of 2 percent over time. This emphasis on average 2 percent inflation has come to be known as flexible average inflation targeting (FAIT). Of significance for now, because actual inflation has been running below 2 percent for several years (based on the Fed’s preferred measure of consumer prices—the Personal Consumption Expenditures index and not the Consumer Price Index), this goal of average inflation of 2 percent over time implies that the Fed will be seeking inflation moderately above 2 percent for some unspecified length of time to counterbalance the shortfall. (See August 31, 2020 post, “The Fed’s New Game Plan: Radical?”).

At this point, there seems to be little doubt that inflation will be moving up to and beyond 2 percent. At issue is whether inflation dynamics will be such that the Fed will be unable to keep inflation from continuing to march higher. In other words, is the Fed overconfident in its ability to restrain inflationary forces sufficiently to achieve their 2 percent average target. Or will policymakers unleash unwanted inflation that will disrupt the normal functioning of the economy. Such unwanted inflation is what happened in the 1970s, but that episode may be too far in the rearview mirror to raise caution flags. Still, the inflation of the 1970s is not something that we would like to see repeated. At that time, the nation faced the very unpleasant choice of letting rapid inflation continue and thereby allow the economy to continue to stagnate while our most vulnerable people were experiencing the erosion of purchasing power of their hard-earned savings or to tackle the inflation beast. In late 1979, the Fed under Paul A. Volcker chose the latter and launched a herculean effort to bring inflation down that had as a byproduct the worst recession in the postwar period to that time. While the cost of fighting inflation proved to be worth the benefits of the healthier economy that followed for a couple decades, that cost nonetheless was huge.

In sum, inflation is picking up and will move above 2 percent. The Fed is taking a big bet that it will be able to keep inflation from climbing still higher and will be able to hold inflation to a 2 percent average rate. Let’s hope that they win this bet.