The recent news on the economy, especially on the labor market, is confirming that a head of steam is building. Fortunately, the upbeat news has extended to the sectors hit hardest by the pandemic (owing importantly to fear and governmental restrictions)—notably, hotels, restaurants and bars, entertainment, and airlines. As noted in previous commentaries, the economic fundamentals point to a vigorous pickup in household and, to a lesser extent, business demand in the months ahead, augmented by retailer efforts to replenish depleted inventories. (See, March 20, 2021, The Economy: There is Plenty of Fuel in the Tank; March 3, 2021, The Economy: The Pause is Ending; and February 13, 2021, The Economy: Spring is Just Around the Corner.) The upturn underway will benefit producers of both goods and services but, in some cases, add to strains on production.

To place things in perspective, output in the first quarter of this year was less than 1 percent below its pre-COVID peak and well on its way to surpassing that peak in the current quarter. In contrast, hours worked by employees in the first quarter were a full 4-1/2 percent below their pre-Covid peak. The resulting gap between output and hours worked is large and unsustainable. Further, many employers chose to boost production once demand rebounded late last spring by boosting hours of the workers they retained rather than adding new workers, a very typical response to a turnaround in the economy that was still considered to be tentative. Going forward, as the economy gains further traction, employers will rely more on adding workers to their payrolls to bring worker hours into better alignment with production and to enable an easing back of hours of existing workers. Most to benefit will be workers in the lagging service sector.

Not all sectors will experience smooth traveling as the recovery continues to unfold. First is the global chip shortage that has particularly limited production of motor vehicles (have you noticed fewer vehicles on the lot of your local new car dealer?). The setback was caused by the COVID shock, and it will take some months before chip production catches up. Meanwhile, the output of motor vehicles and other chip-intensive products will be lagging demand.

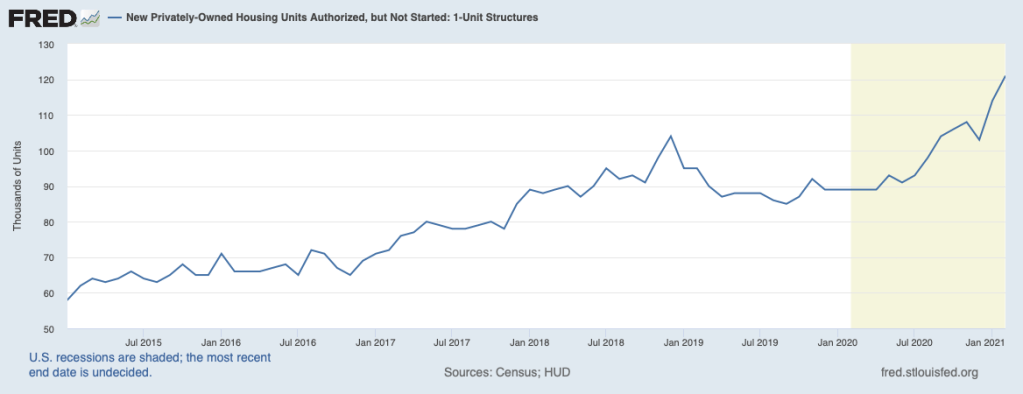

Second, the housing market has been restrained by supply constraints, also. One indication of growing strains in this sector are housing units authorized but not started, the chart below. This indicator has risen to the highest level in a decade and a half. Contributing to capacity constraints on new homes are tight supplies of lumber and other materials.

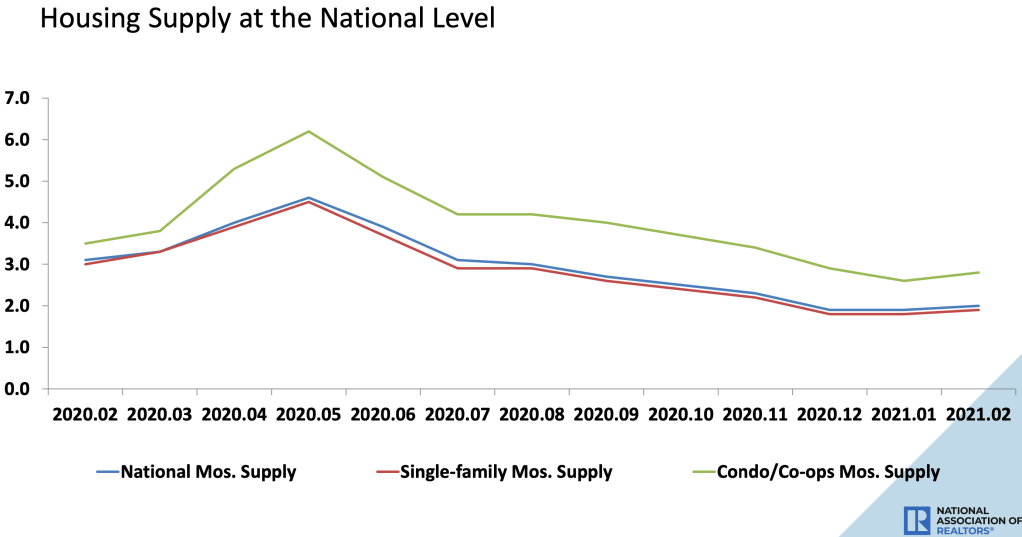

Supply constraints also are evident in the market for existing homes. This is illustrated in the following chart showing the average number of months that a home is on the market. New listings are being snatched up at a quick pace not seen for a while. This has been a key factor limiting sales of existing homes in recent months.

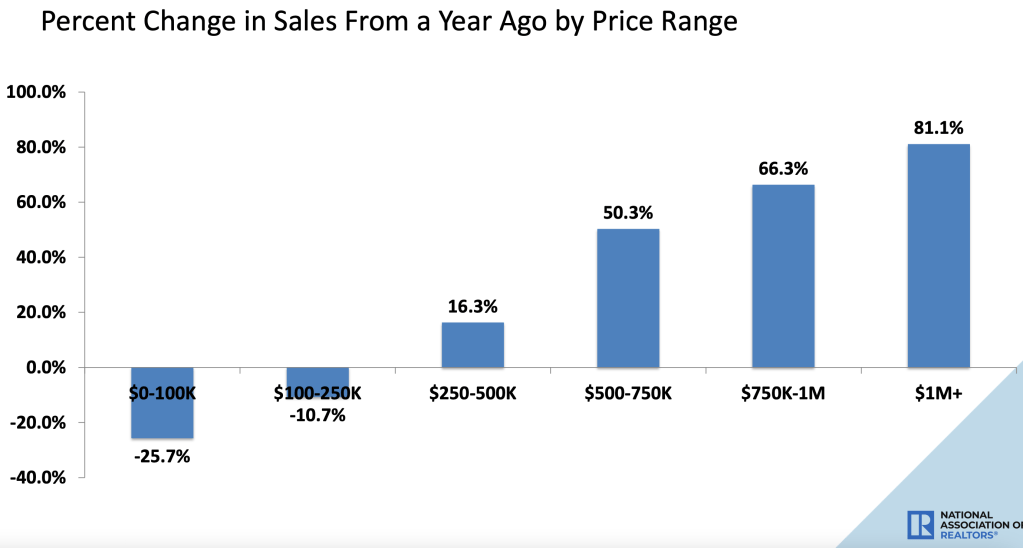

The housing market has been briskest at the upper end as shown below by year-over-year sales growth for six different price brackets. Sales have risen 80 percent over the past year in the top price bracket but have fallen 25 percent in the lowest bracket. This disparity reflects the better fortunes of those in the upper-income brackets during the pandemic compared to those in the lower-wage service sector.

Also showing selectivity in the housing sector has been mortgage credit. The availability of mortgage credit for a home purchase has been ample for those in the upper-income brackets who have been able to remain employed during the pandemic but less so for those who have struggled the most. Time will be needed for supplies of homes and mortgage credit to become aligned with demand and to become more evenly available among home buyers. Meanwhile, home prices can be expected to continue rising sharply. The next chart illustrates that an index of existing homes has reached double-digit gains and is on a distinct upward trajectory, echoing a pattern that characterized the housing bubble period that ended fifteen years ago.

So what could derail the rebound going forward? Clearly, another major outbreak of COVID could curb the pace of re-openings and slow the pace of recovery. This, however, seems less likely with each passing day as larger numbers are vaccinated and herd immunity spreads.

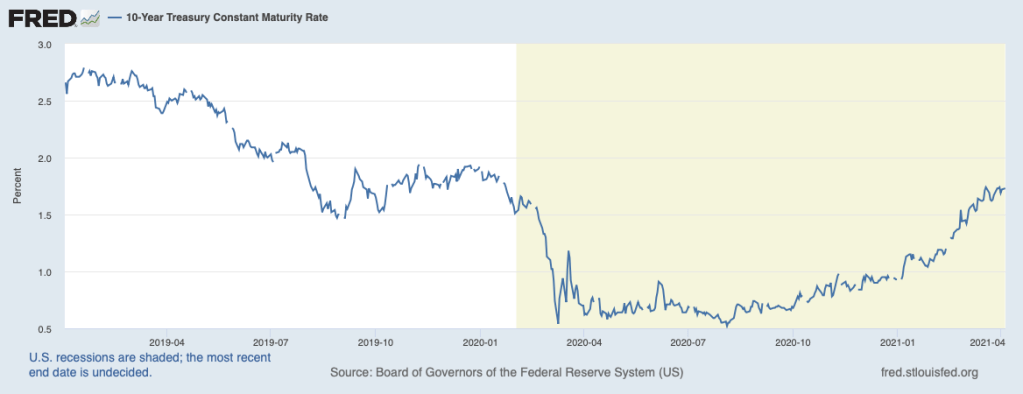

Some have raised concern that the recent rise in long-term interest rates, including the mortgage rate, could be a serious headwind facing the recovery. The chart below illustrates that the benchmark 10-year yield has risen about 1 percentage point since last fall, with much of that increase occurring over recent weeks. Behind this increase has been mounting evidence that the economic outlook has improved greatly. In this context, the rise in interest rates should be viewed as a reflection of economic strength and not an impediment to recovery.

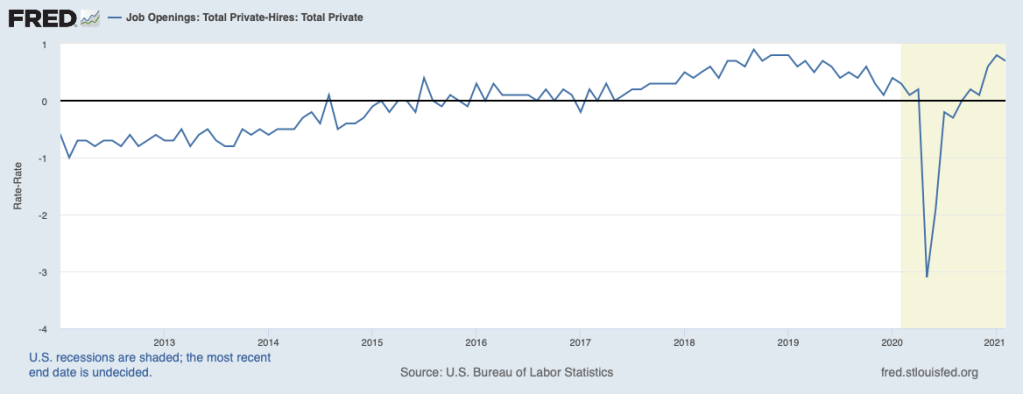

Beyond these, the direction of public policy could also be a factor limiting prospects for growth. In the months ahead, any additional measures to extend generous benefits for those collecting unemployment insurance will induce many workers to stay on the unemployment rolls and not take the jobs that are opening up as demand for workers continues to strengthen. The next chart illustrates the excess of job openings over job hires:

In recent months, job openings have exceeded new hires by a sizable margin, indicating that employers have unfilled positions that are holding back production and the satisfaction of rising demand. In some cases, the problem has been a skills mismatch between the job requirements of the open positions and workers available, but, in many cases, qualified workers have not been showing up to fill the vacancies.

Another possible obstacle to growth could be impending tax hikes. The proposed increase in the corporate tax rate will reduce returns on investments made by corporations and limit the rebound in business investment as well as employment opportunities for workers. Furthermore, higher marginal tax rates on personal income will act as a deterrent for risk-taking by entrepreneurs which in time will also act to limit growth.

In sum, the economy is building a head of steam that is being translated into big gains in jobs, especially for workers who have been hit hardest by the pandemic. But some sectors are experiencing some strains on supply chains—especially chip-intensive sectors—while the housing sector has been facing other supply restraints. It will take some time to work through these headwinds fully. Beyond these, it is important to keep in mind that some public policy measures currently being discussed could well be slowing the train.