Although the statistical evidence has yet to provide widespread confirmation that the economy is accelerating, there is a growing list of indicators that point to an imminent boost to economic activity. To a degree, the upturn has been restrained by disruptions from supply chain difficulties and unusually severe winter weather in key portions of the country that will prove temporary.

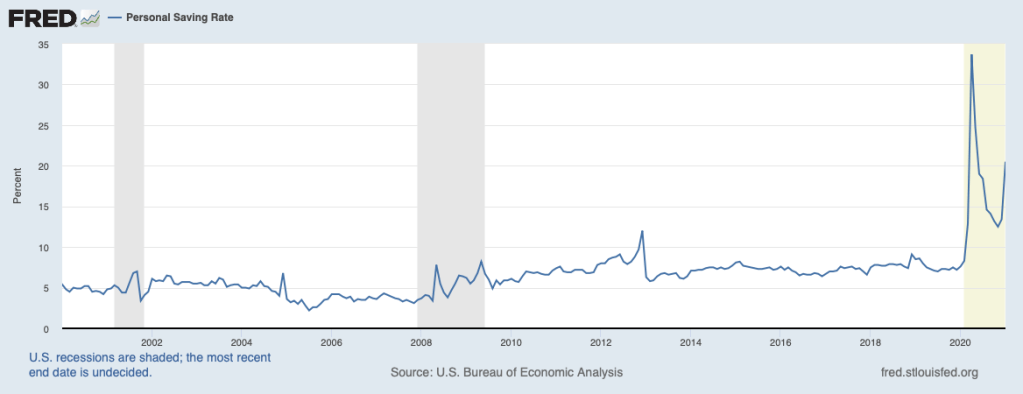

Consumer spending has begun the year smartly. At an average monthly rate, retail sales have risen slightly more than a 1 percent pace over January and February (about 13 percent at an annual rate). Moreover, the saving rate, shown below, has been extraordinarily high since the onset of the COVID pandemic, meaning that consumers have been keeping their powder dry.

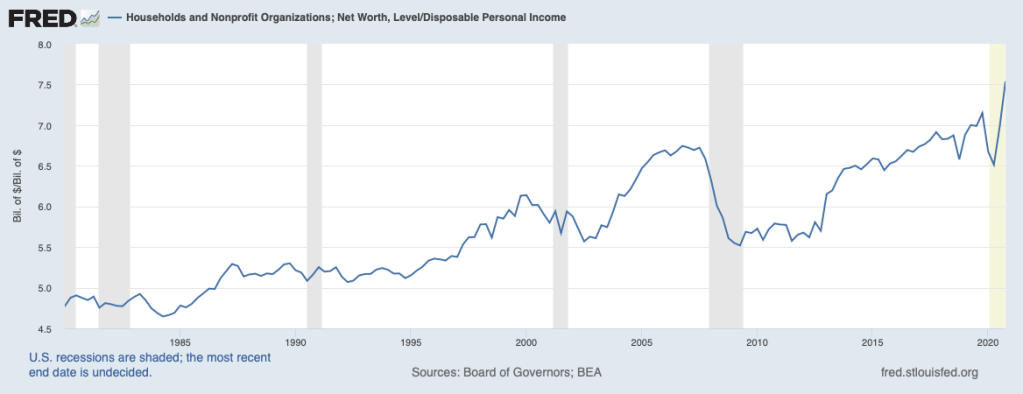

This has occurred against a backdrop of record-high household wealth and wealth-to-income ratio—the following chart—which typically induces more spending and less saving. The latest round of federal stimulus checks will add to already brisk consumer spending in the months ahead.

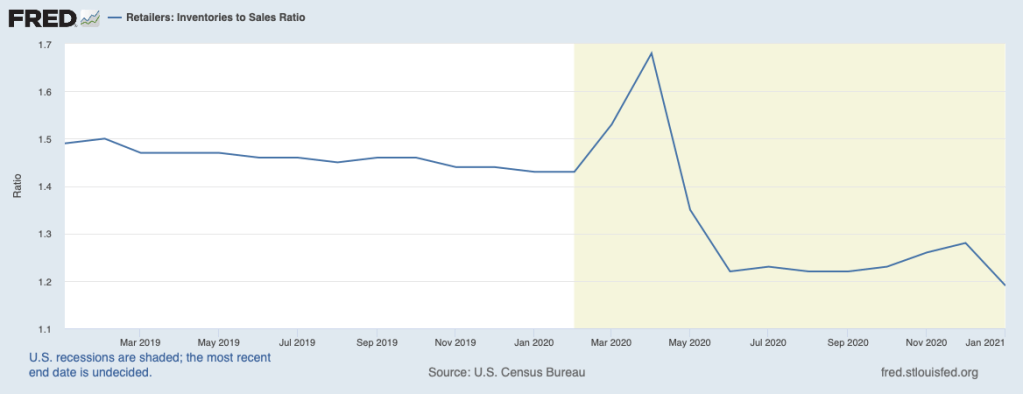

Faster consumer spending will place new strains on retailer inventories. The next chart illustrates how retail inventories (relative to sales) touched a low in January of this year. Retailers found themselves in the uncomfortable position of not being able to fully meet customer demands.

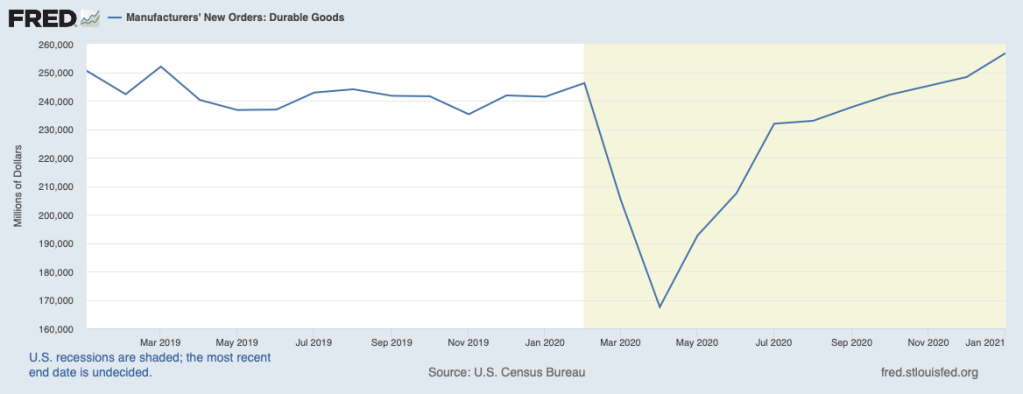

In response to lean inventories and expectations of improving sales, businesses have stepped up their orders, as shown in the next chart for consumer and producer durable goods. Growing order books will be translated into more production and more employment. The rising rate of COVID vaccinations, declining cases, lifting of COVID restrictions, and removal of supply-chain curbs will enable production to respond and grow faster. Expanding output in the sectors that have faced the most severe supply constraints in the past year—such as lumber and other building materials—should also relieve price pressures in those areas. A limiting factor on the pickup in output will be labor shortages in some segments of the labor market, exacerbated by generous unemployment benefits that are discouraging many workers from returning to the labor force.

Encouraging have been recent reports that indicate some of the service sectors hit hardest by the pandemic—restaurants and bars, hotels, and airlines—are seeing a turnaround. Even though growth is picking up in the service sector, and may soon exceed growth in the goods-producing industries, many parts of the service sector will continue to lag the rest of the economy.

In sum, the economy is poised to gain strength over the coming months, paced by consumers. The labor market, accordingly, will be looking better across the board.