It bears repeating that this business cycle has been like no other. The COVID shock produced the steepest contraction in output but the shortest recession on record. Spending on nearly everything except food purchased from grocery stores dropped precipitously. In the face of the lockdown, production of nearly everything also dropped off sharply.

In a typical economic recession, demand for items across the board softens, with spending on postponable big-ticket items (commonly financed on credit) weakening the most. That demand pattern is reversed when the economy turns upward. Demand strengthens for goods and services across the board, with demand for big-ticket items strengthening the most. Production typically lags aggregate demand, but will eventually catch up. As a consequence, inventories build up early in a downturn but are drawn down as demand revives early in the upturn.

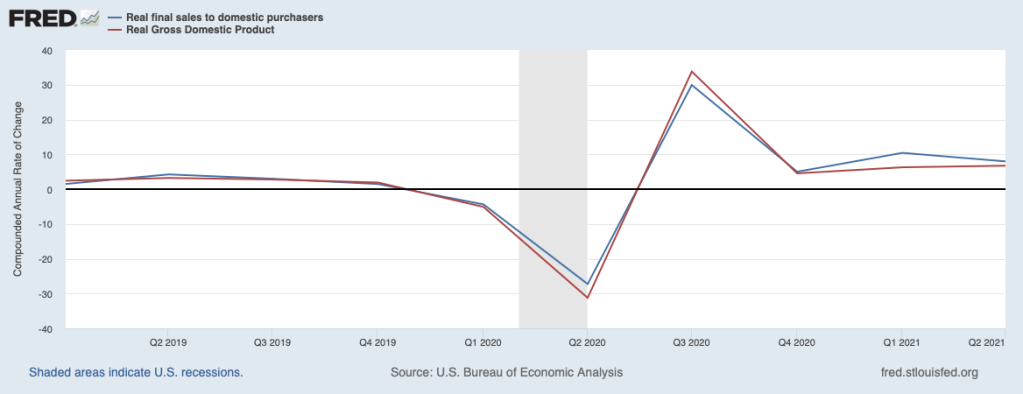

The chart below shows a proxy for growth in aggregate demand (Real Final Sales, the blue line) and production growth (Real GDP, the red line) since early 2019, a year before the onset of the pandemic. Both grew around the same rate over 2019 and both declined sharply over the first half of 2020. In response to the COVID shock, consumers and businesses cut spending on all but the bare necessities while producers slashed production across the board in response to the lockdown. Note that production plunged more than demand in the second quarter of last year when the brunt of the pandemic shock was felt on the economy. This contrasts with typical downturns in which demand falls more than production, a point we will come back to.

Both output and demand rebounded sharply in the second quarter of last year, with production outstripping demand. Since that time, production has expanded more slowly than demand. Not included in the chart are data for the third quarter of 2021 for which estimates indicate that output barely increased. It should be noted that the data for the proxy for aggregate demand (final sales) are understating actual underlying demand because buyers have not been able to purchase many of the goods that they want. Inventories of many consumer and producer goods have been depleted by demand outstripping supply over the pandemic period, leading to extremely lean inventories.

Supply has also been held back due to the difficulty in finding workers and the pervasive supply chain bottlenecks. Employers have been posting a record number of job vacancies over recent months, but the number of employed persons this September was 5 million below February 2020. Moreover, about 3 million people have dropped out of the labor force over this same period despite the greater number of jobs available.

Clearly, something is holding people back from taking the many available jobs. To some extent, it is a skills mismatch. Over 60 percent of small businesses in the most recent National Federation of Independent Business (NFIB) survey reported difficulties in finding qualified workers. Similar situations in the past have tended to work themselves out. In part, the working out has involved businesses responding by providing training and becoming more accommodative to employee preferences for work arrangements.

However, there are other reasons why the vacancies are not being filled. Among the reasons are generous government benefits that include larger child tax credits and greater eligibility for food stamps. Moreover, many have decided to stay at home to avoid exposure to COVID and to care for and school children. In addition, vaccine mandates are taking their toll and will continue to do so well into December when the federal mandate is fully binding.

Beyond difficulties in filling jobs, supply-chain disruptions have also been continuously holding down output. Many of those problems can be traced to just-in-time production methods that had been widely practiced around the globe in the production of goods. With just-in-time, manufacturers schedule delivery of materials and components to arrive just in time for scheduled production. In this manner, they can hold smaller inventories of inputs and cut down on the costs of managing inventory. However, when production dropped off more sharply than demand in response to the COVID shock – and when demand snapped back unexpectedly – producers found themselves short of key inputs and unable to meet production schedules. The problem has been most acute in the production of microchips. Ongoing transportation delays, notably involving cargo ships and trucks, have placed businesses further behind the curve.

These supply bottlenecks will work themselves out over time. At some point, these disruptions will become less of a problem restraining production, but the timeline will be extended by producers dropping just-in-time production methods. Having been burned by the pandemic experience, many businesses will attempt to protect themselves by boosting their orders for purposes of building precautionary buffers of inventories which will add to strains on their suppliers until supply-chain problems are resolved.

The extent of the supply-chain constraints on the production of goods, especially consumer goods, can be seen in the table below. The table presents total manufacturing output in all of 2020 and over August and September of this year.

| Year 2020 | Aug. – Sep. 2021 | |

| Total manufacturing | -2.5 | -1.1 |

| Consumer goods | -0.8 | -1.6 |

| Automotive | 5.1 | -10.7 |

| Home electronics | 16.1 | 0.6 |

| Appliances and furniture | 5.2 | -1.4 |

Manufacturing output over the past two months contracted by a little more than 1 percent, about half that for all of 2020. Production of consumer goods declined over August and September by double the decline over all of 2020. The weakening of production is most dramatic in the automotive sector, but also very pronounced in home electronics, appliances, and furniture.

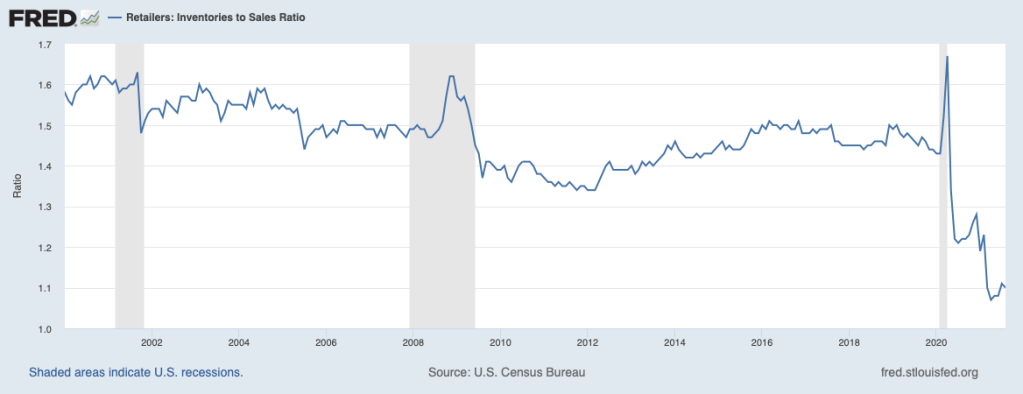

The impact of production disruptions is visible in retail inventories, shown in the chart below. The inventory-sales ratio being presented understates the paucity of inventories because sales in the denominator have been held down by the lack of available goods. The chart shows that inventories are way out of line with historical experience. Moreover, not only are retailers going to be rebuilding stocks to previous levels, but as noted they will be wanting to add a precautionary cushion which will prolong strains on producers of goods.

With demand pressing against limited supply, not surprisingly, the prices of consumer goods have registered outsized increases, shown in the table below. Shown are price increases over the twelve months of 2020 and the twelve months ending in September 2021 (note that there is some monthly overlap). Prices for commodities excluding food and energy accelerated from a 1.6 percent increase to a 7.3 percent increase. Within this grouping, the pickup in inflation was evident across all categories shown, especially TVs. All these products have microchip components, and their producers will continue struggling with shortages of chips.

Percent Change in Consumer Prices

| Item | 2020 | 2021 |

| Commodities ex. food and energy | 1.6 | 7.3 |

| New vehicles | 1.9 | 8.7 |

| Appliances | 5.7 | 9.6 |

| TVs | -2.9 | 12.7 |

| Computers | 1.6 | 8.5 |

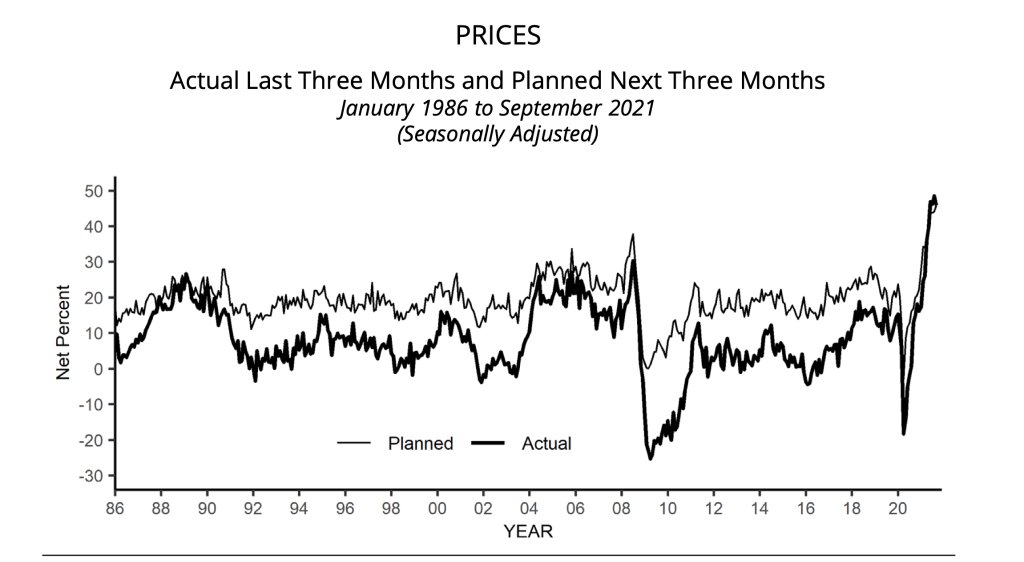

Looking ahead, these supply restraints will not be disappearing anytime soon. In the meantime, strong demand will continue to press against available supply, and goods prices will continue to post large increases. For example, the chart below shows that nearly half of all respondents to the most recent NFIB survey had recently raised selling prices, and about the same share intended to raise prices in the near future.

The chart above shows the largest number of sellers in thirty-five years. Similarly, large businesses are reporting in growing numbers that they intend to increase prices over the coming months. This is much like the actions taken by smaller businesses. It is also worth noting that many consumers are expecting price increases.

Accordingly, public opinion polls show that inflation continues to become more of a concern for American families. Consumer expectations of inflation over the longer term from the Michigan Survey of Consumers have been edging higher over recent months, as shown in the next chart, and likely will be headed further upward given the outlook.

Source: University of Michigan, Monthly Survey of Consumers.

Against this backdrop, inflation has some inertia that is getting built into the decisions of businesses and workers. This poses a dilemma for the Fed due to its target of 2 percent average inflation, which over time may be getting further out of reach. This inflation inertia implies that the Fed may not only need to scale back its asset purchases of $120 billion per month, but move forward in time its decision to begin raising its target for the federal funds rate from the effective lower bound of zero where it has been for more than a year and a half.