Merriam-Webster

https://www.merriam-webster.com/dictionary/transitory.

Concern about inflation has been mounting over recent months and was punctuated by the 0.9 percent increase in the CPI for October (11 percent at an annual rate). Public opinion polls are indicating that concern about the inflation outlook has been steadily rising. Meanwhile, Fed policymakers have been saying that the surge in prices this year is “transitory,” reflecting temporary factors largely related to supply chain disruptions. However, the Fed’s conviction on this point has softened. Earlier this month, in their monetary policy statement, the Fed added the words “expected to be” to a sentence dealing with the inflation outlook to read, “Inflation is elevated, largely reflecting factors that are expected to be (emphasis added) transitory.” Previously, they characterized the inflation situation as follows: “Inflation is elevated, largely reflecting transitory factors.”

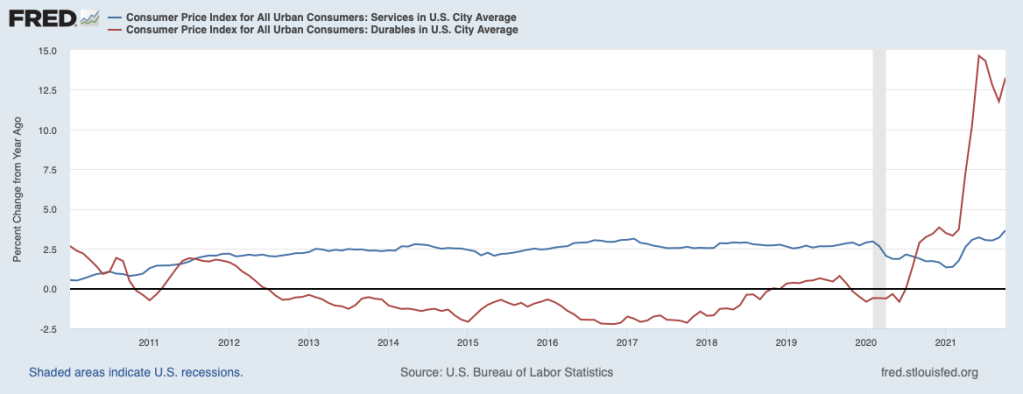

As noted in previous commentaries (See: October 25, 2021, Placing the Economic Expansion in Perspective; October 8, 2021, Supply Restraints Continue to Bedevil the Economic Expansion; and September 18, 2021, Has the Inflation Dragon Been Slayed?), supply chain disruptions have been boosting the prices of consumer goods while strains in the labor market have been putting upward pressure on the prices of services as well as goods. The upturn in goods and services inflation is illustrated in the chart below which shows the twelve-month rate of change of prices of consumer durable goods (the red line) and services (the blue line)—both components of the CPI. The chart shows that the prices of consumer durables tend to decline mildly over time while prices of services typically increase around 2.5 percent each year. This year, though, prices of durable goods have surged to roughly a 12.5 percent rate while the increase in the prices of services has climbed to a 3.5 percent rate. (Not shown is the change in prices of nondurable goods which have had a pattern similar to that of the prices of durables but a muted swing.)

While the chip shortage has been imparting upward pressure on the prices of some consumer goods—such as motor vehicles, appliances, and personal computers—other supply-chain bottlenecks are pushing up goods prices more broadly.

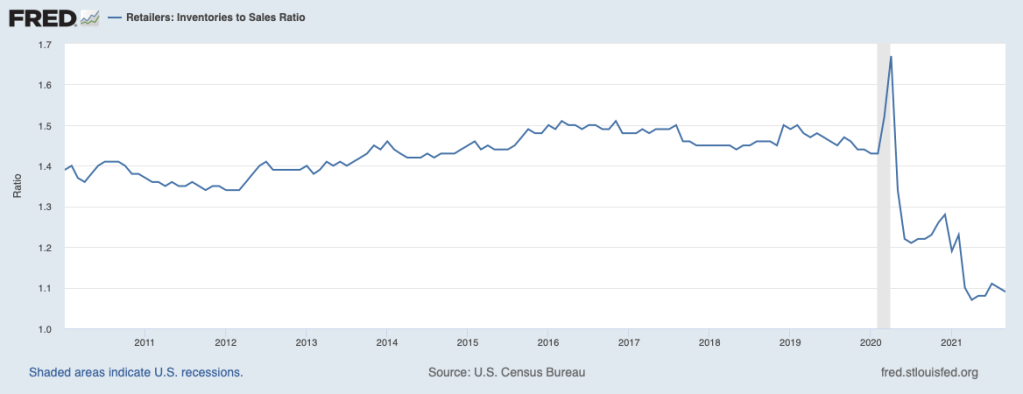

With demand remaining very strong and producers struggling to catch up, retail inventories of goods remain uncomfortably lean— the next chart.

The chart shows that inventories in relation to sales remain exceptionally low and have shown no progress toward rebuilding over recent months. Looking ahead, demands by retailers to replenish shelves will be adding to upward pressure on goods prices in the coming months.

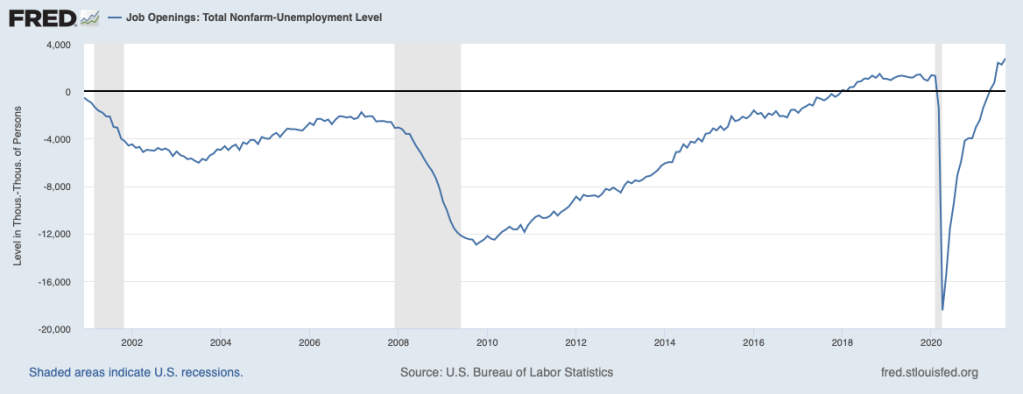

In addition to supply-chain bottlenecks, tautness in the labor market is raising costs to sellers and adding to inflation pressures. This tautness is illustrated by the chart below, showing the excess of job openings over the number of unemployed persons. The gap moved into record territory in September (most recent data).

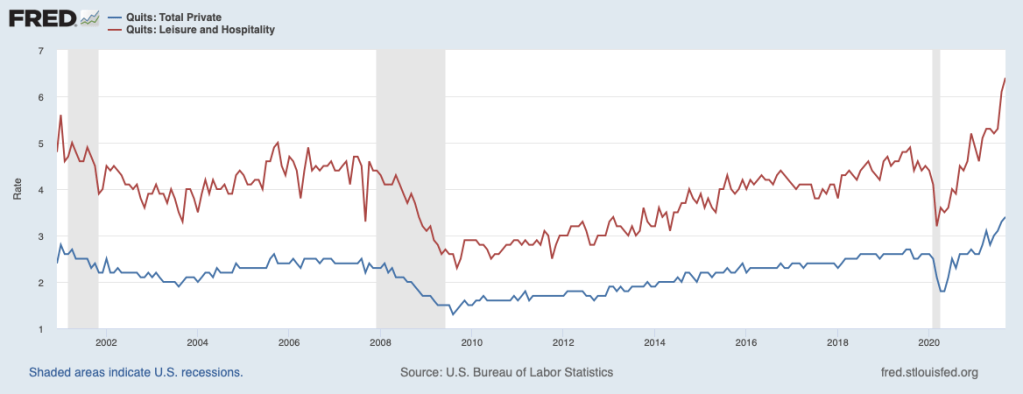

Also reflecting tautness in the labor market is the record number of quits, shown next. People quit jobs in droves when they are sure that they can find a better job quickly. The blue line is the quits rate faced by all private-sector employers, and the red line is the rate for employers in the leisure and hospitality sector. Both have risen sharply this year, with the quits rate in the leisure and hospitality sector outpacing other sectors.

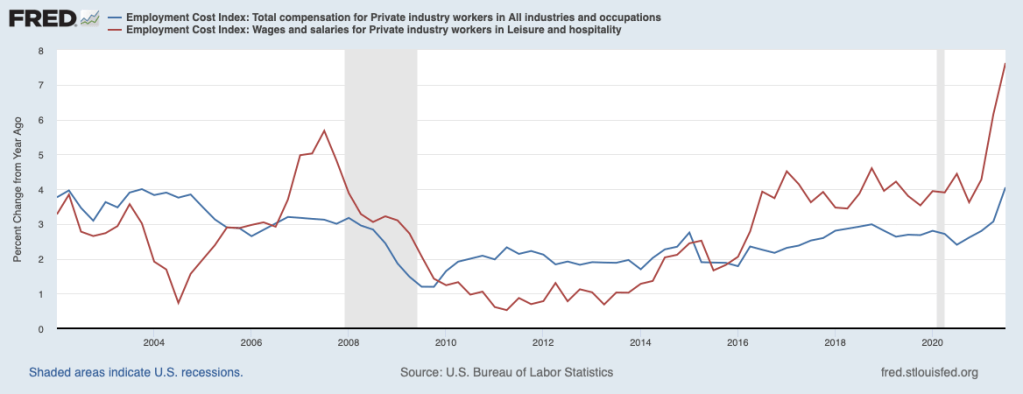

In response, employers have been trying to retain current employees and attract new employees by aggressively raising compensation, shown next. The blue line shows the twelve-month change in compensation (wages and salaries and benefits) for all workers in the private sector and the red line shows growth in compensation in the leisure and hospitality sector.

Compensation in the private sector overall has accelerated from around 3 percent per year prior to the pandemic to 4 percent more recently. In contrast, compensation in the leisure and hospitality sector has gone from around 4 percent prior to 7.5 percent more recently. Startling was the recent settlement at John Deere that includes an immediate restart bonus of $8,500 per worker and a 10 percent hike in compensation, which likely will be a pattern for other employers in the manufacturing sector. The broad pickup in compensation is placing considerable pressure on prices throughout the economy.

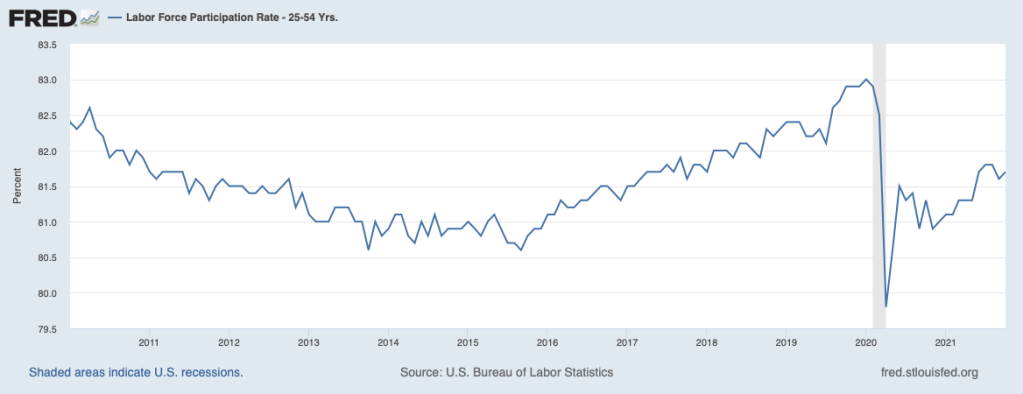

Adding to strains in the labor market has been a reluctance to return to the labor force on the part of workers who dropped out of the labor force when COVID hit. This reluctance is shown in the chart below depicting the labor force participation rate for prime-age workers. Participation rebounded shortly after the pandemic shock hit.

Since that time, it has only regained a portion of lost ground. Noteworthy, too, participation on the part of retirement-age workers also dropped off sharply at the onset of the pandemic but has shown very little indication of reversing that drop. The reluctance of workers to return to the labor force, despite the abundance of openings and competition for workers, will continue to place strains on the labor market and restrain aggregate supply. Indeed, the experience of the Great Recession of 2008 of a dozen years ago suggests that it will take a long while for participation on the part of prime-age workers to return to pre-COVID levels.

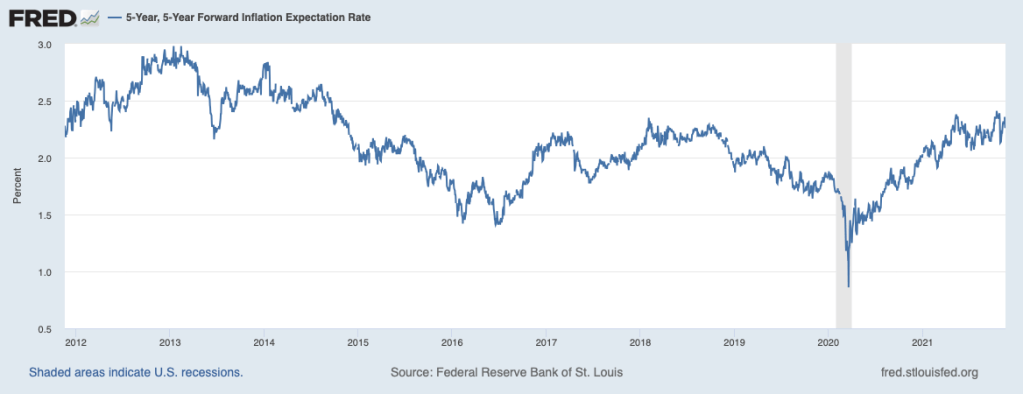

The above discussion implies that outsized price increases are likely to continue for as long as supply-chain disruptions persist, which could be another year. A critical issue is whether inflation has meanwhile gained enough momentum that it will continue after supply-chain strains have been relieved. Much depends on whether longer-term inflation expectations move above a range consistent with the Fed’s 2 percent inflation target. Shown next is an indicator of longer-term inflation expectations, based on Treasury security yields—so-called inflation compensation for the five-year period starting in five years. This indicator of inflation expectations has moved above pre-COVID levels. However, this measure has not moved outside the range of the past decade, when actual inflation tended to be below the Fed’s 2 percent target and has not moved much over recent weeks despite the bad news on the inflation front.

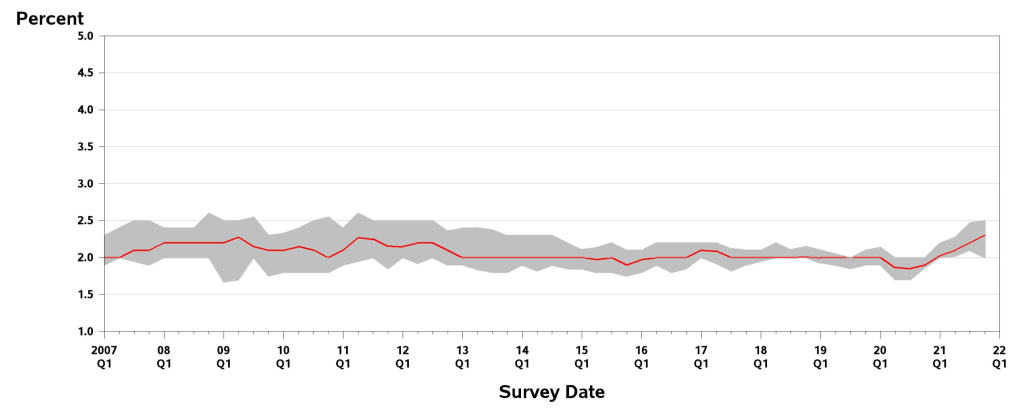

In contrast, the most recent survey of professional forecasters shows longer-term inflation expectations continuing to rise and move outside the range of the past decade and a half—the chart below.

This increase surely must be raising concern on the part of Fed policymakers, given the role of the survey respondents. This move seems to be bringing forward in time a policy dilemma: If inflation expectations are no longer consistent with their 2 percent target, they will need to begin raising the federal funds rate sooner than they were planning. Ahead of the liftoff of the policy interest rate, they will need to end their asset purchase program sooner than they contemplated. The Fed recently announced that they would end asset purchases in mid-2022. Putting it all together, the upturn in longer-term interest rates, including those on mortgages, will be larger than had been expected by the Fed and the market participants. Moreover, we are likely to experience some turbulence in financial markets along the way.