The Federal Open Market Committee raised its target for the federal funds rate ¼ percentage point on February 1 and suggested that a couple more similar-sized increases will be forthcoming. Fed policymakers further indicated that they will be assessing the lagged effects of previous rate increases and whether those effects are unfolding in line with expectations or whether a new path for the federal funds rate will be needed. Meanwhile, the FOMC emphasized its determination to bring inflation down to the 2 percent target in its February 1 policy statement – “The Committee is strongly committed to returning inflation to its 2 percent objective.” This resolve was also emphasized by Chair Powell in his post-meeting press conference and a week later before the Economic Club of Washington, D.C.

The primary purpose for the Fed repeatedly stressing its commitment to low inflation is to convince businesses and consumers that inflation will return to 2 percent so that businesses and households will make decisions based on that expectation. If expectations of inflation move above 2 percent, this will impart upward pressure on inflation, and the goal of 2 percent inflation will not be achievable on a sustainable basis. And the farther inflation expectations drift above 2 percent, the more difficult and painful will be the process of returning to 2 percent inflation.

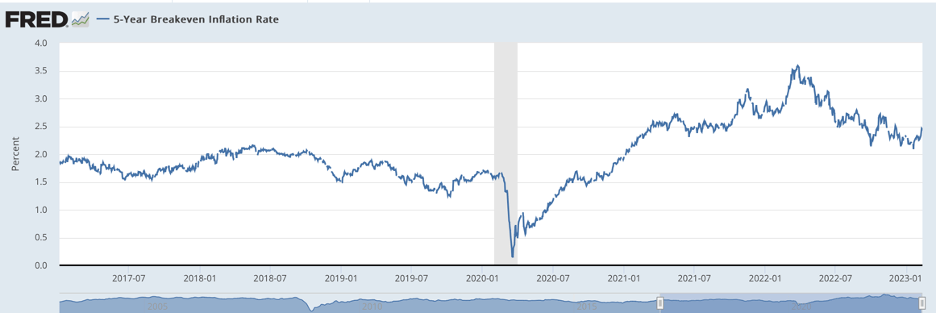

How successful has the Fed been in keeping inflation expectations tethered? Longer-term inflation expectations are generally deemed to be more important for the inflation process than shorter-term expectations. Analysts gauge inflation expectations from various surveys and the Treasury securities market. The chart below shows a Treasury securities market measure of compensation that investors require for inflation over the next five years, which is primarily expected inflation over the next five years and is frequently referred to as the break-even rate. Note that this measure remains above the pre-COVID period, even though it is off its peak. An important reason why the five-year break-even rate is higher than in the pre-COVID period is that investors continue to expect inflation over the coming year or two to remain high, holding up the five-year average.

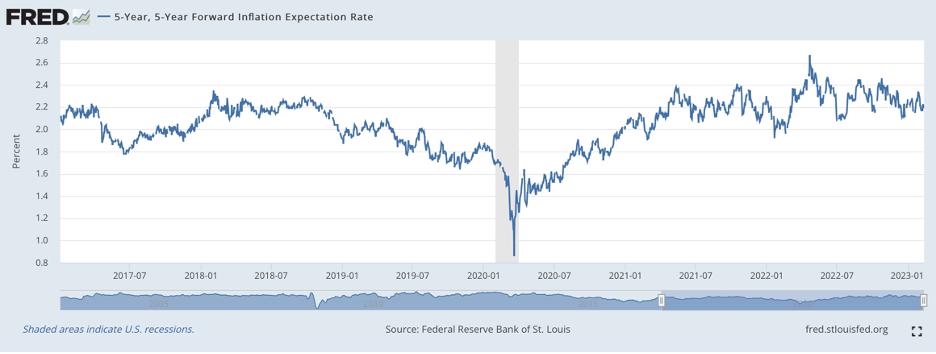

To get a handle on expectations beyond the next few years, the following chart shows expectations of inflation over the five-year period starting in five years. This measure of inflation expectations, too, has been running above the pre-COVID period but appears to have stabilized at a level only mildly above the earlier period.

Turning to survey measures, the following chart shows projections of PCE inflation over the next ten years based on a survey of professional forecasters, with the most recent reading being for February 2023. This measure moved distinctly above the pre-COVID period but has reversed much of that movement most recently.

While the above evidence on inflation expectations is somewhat mixed, on balance longer-term inflation expectations seem to be only a little higher currently than in the pre-COVID period when inflation was low and under control. This evidence of subdued longer-term inflation expectations contrasts with the period of the Great Inflation of the late 1970s and early 1980s when available survey data suggest that longer-term inflation expectations moved steadily higher and approached double digits. It seems safe to conclude that Fed statements underscoring a commitment to restoring price stability have been quite successful, implying that the forthcoming strains on the economy and labor market that will be required if price stability is to be restored will be less painful and disruptive.

Looking at the labor market, the blockbuster jobs report for January of 517,000 new jobs and a drop in the unemployment rate to a fifty-year low is a vivid reminder that the labor market remains very tight. The January report to a degree likely overstated the strength of the labor market, as holiday-related flows into and out of the labor market are huge and statistical methods for adjusting for these swings in flows are imperfect; nonetheless, even after allowing for these technical factors, the January labor report was strong. Beyond the January employment report, weekly data on initial claims for unemployment insurance through early February have yet to hint that a cooling off of conditions in the labor market has begun.

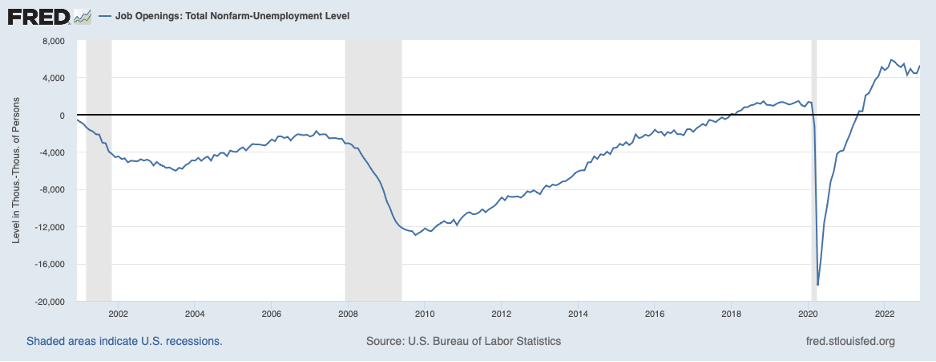

The extraordinary imbalance between labor demand and supply is illustrated in the chart below showing the large excess of unfilled job openings over the number of unemployed persons. During the low inflation period prior to 2020, job openings typically fell short of the number of unemployed persons. However, starting in 2021 job openings climbed well above the number of unemployed persons and the large imbalance has persisted through the end of 2022.

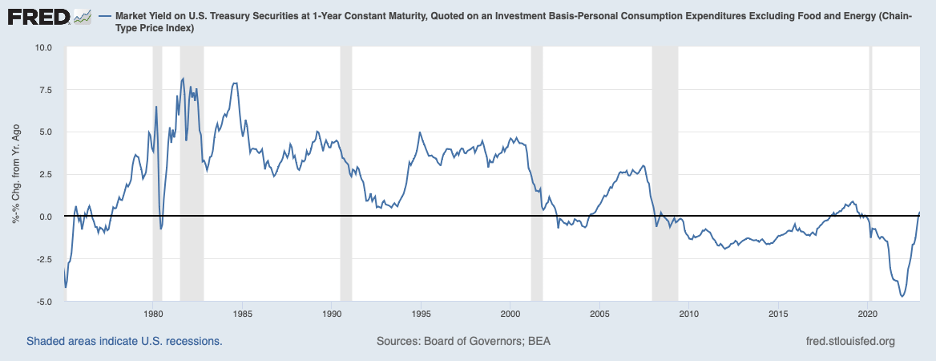

Thus, labor market data have yet to suggest that Fed policy has been restrictive. Indeed, the chart below presents a measure of the stance of Fed policy—the one-year Treasury bill rate less the twelve-month percent change in core PCE prices (available only through December 2022). This measure of the real short-term interest rate finally reached zero at year-end 2022, but even at zero, this rate is still below the neutral rate of 0.5 to 1 percent which is the rate at which monetary policy is neither stimulative nor restrictive. In other words, Fed policy continues to be stimulative, but much less so than a year ago. (The one-year Treasury rate in the chart reflects market expectations of two further ¼ percentage point increases in the federal funds rate over the first half of 2023, and thus even with the February 1 increase in the federal funds rate of ¼ percent, the real short-term interest rate has yet to move into neutral territory.)

Some Fed officials have been arguing for only ¼ percent rate hikes going forward or even a pause in further rate hikes to assess the impact of previous tightening actions (from a 0 percent federal funds rate a year ago to a 4.5 percent rate most recently). However, the chart above reminds us that Fed policy has remained stimulative over the past year of policy tightening. Thus, the lagged effects of policy are the lagged effects of diminishing stimulus.

Putting the pieces together, the Fed will need to keep raising the target for the federal funds rate. The federal funds rate must not only reach neutral but must move well into the restrictive territory to apply sufficient restraint to place inflation on a downward path to 2 percent. Achieving this disinflation will require slack in the labor market, which will require a considerable cooling in labor market conditions. All of this implies that the federal funds rate will need to be raised by more than another full percentage point. Moreover, short-term rates will need to remain high for as long as it takes to get inflation firmly on the path to 2 percent and to return longer-term inflation expectations to levels consistent with 2 percent inflation. Thus, finishing the job of restoring price stability will take continued vigilance on the part of the Fed. The vigilance to date has been paying off in holding down longer-term inflation expectations, which will reduce the sacrifice of employment and output needed to restore price stability.

The strong labor report for January, along with ongoing firm rhetoric from Fed officials, has been prompting market participants to nudge higher their expectations for the federal funds rate. Currently, market participants expect two additional ¼ percent increases in the federal funds rate by midyear—taking the federal funds rate up to 5 percent—and a moderate chance of another ¼ percent increase before they see this rate starting to come down toward the end of 2023. However, market participants will need to continue to boost their expectations for the path of the federal funds rate in order for them to be aligned with the path that will be needed to bring inflation down to 2 percent. This forthcoming upward revision to the path of the federal funds rate by market participants implies further downward pressures on the prices of bonds and stocks and upward pressure on the exchange value of the dollar.